Вам также может понравиться

- Regional Rural Banks of India: Evolution, Performance and ManagementОт EverandRegional Rural Banks of India: Evolution, Performance and ManagementОценок пока нет

- Credit Risk ManagementДокумент86 страницCredit Risk ManagementSagar Paul'g100% (1)

- Study On Retail Banking Transformations in India MBA FinaceДокумент17 страницStudy On Retail Banking Transformations in India MBA FinaceChetan ChanneОценок пока нет

- SBI Bank ProjectДокумент150 страницSBI Bank Projectee23258Оценок пока нет

- PDF Credit Analysis of Personal Loan HDFC Bank Specialisation ProjectДокумент89 страницPDF Credit Analysis of Personal Loan HDFC Bank Specialisation ProjectTejas BhavsarОценок пока нет

- Project Report: Post Garduate Diploma in Business Admnistration (PGDBM)Документ55 страницProject Report: Post Garduate Diploma in Business Admnistration (PGDBM)Aamir Khan100% (1)

- Project On HDFC BankДокумент72 страницыProject On HDFC Banksunit2658Оценок пока нет

- Home LoansДокумент40 страницHome LoansPrashant K. SinghОценок пока нет

- Project Report: "Study On Financial Services by Bank of Maharashtra ''Документ60 страницProject Report: "Study On Financial Services by Bank of Maharashtra ''Yash GandhewarОценок пока нет

- Surat Peoples Cooperative Bank LTDДокумент108 страницSurat Peoples Cooperative Bank LTDbrmehta06Оценок пока нет

- Bank of Maharashtra PDFДокумент76 страницBank of Maharashtra PDFPRATIK BhosaleОценок пока нет

- Rayudu DocumentДокумент55 страницRayudu DocumentPinky KusumaОценок пока нет

- Project Presentation On "Reverse Mortgage in India": Presenter: Shaikh Azharoddin Shakeel. Roll No.03 Mms-IiДокумент17 страницProject Presentation On "Reverse Mortgage in India": Presenter: Shaikh Azharoddin Shakeel. Roll No.03 Mms-IiAzharОценок пока нет

- Home Loans On Icici BankДокумент11 страницHome Loans On Icici BankSridharan RaviОценок пока нет

- Housing Finance A Comparative Study of SBI and HDFC BankДокумент3 страницыHousing Finance A Comparative Study of SBI and HDFC BankEditor IJTSRDОценок пока нет

- Corporate BankingДокумент63 страницыCorporate BankingRicha SinhaОценок пока нет

- Comparative Study of HDFC and SbiДокумент53 страницыComparative Study of HDFC and SbiABHISHEK RAWATОценок пока нет

- Project On Loans and AdvancesДокумент3 страницыProject On Loans and Advancesbilgrak67% (6)

- Retail Banking of Allahabad BankДокумент50 страницRetail Banking of Allahabad Bankaru161112Оценок пока нет

- Introduction and Functions of Nationalized BankДокумент10 страницIntroduction and Functions of Nationalized BankPrashant MunnolliОценок пока нет

- A Study On E-Banking Services of Axis Bank LTD: Submitted ToДокумент12 страницA Study On E-Banking Services of Axis Bank LTD: Submitted ToNavyug NavОценок пока нет

- A STUDY of NPA ProjectДокумент74 страницыA STUDY of NPA ProjectAman RajakОценок пока нет

- THEJASWINI ProjectДокумент112 страницTHEJASWINI Projectswamy yashuОценок пока нет

- Icici Bank FileДокумент7 страницIcici Bank Fileharman singhОценок пока нет

- MuthootДокумент45 страницMuthootZachy Jimmy VellukunnelОценок пока нет

- Sanjana Financial Statement ProjectДокумент49 страницSanjana Financial Statement ProjectPooja SahaniОценок пока нет

- Shriram Finanace NewДокумент43 страницыShriram Finanace NewRavi GuptaОценок пока нет

- Customer Satisfaction Towards HDFC BANKS AND SBI PDFДокумент90 страницCustomer Satisfaction Towards HDFC BANKS AND SBI PDFKrishma RatheeОценок пока нет

- Consumer Finance..yatith Poojari (Yp)Документ67 страницConsumer Finance..yatith Poojari (Yp)Yatith PoojariОценок пока нет

- M Com Project Topics For Banking SpecializationДокумент2 страницыM Com Project Topics For Banking SpecializationGudala SrikanthОценок пока нет

- Uday BlackbookДокумент61 страницаUday BlackbookRavi VishwakarmaОценок пока нет

- Financial Services Offered by BankДокумент52 страницыFinancial Services Offered by BankIshan Vyas100% (2)

- Project Report ON "Analysis of Financial Statement" OF: Icici BankДокумент53 страницыProject Report ON "Analysis of Financial Statement" OF: Icici BankManish Nagpal100% (1)

- Retail Banking Front Office Management Activity For HDFC Bank by Nisha Wadekar This Project Is Very Useful To StudentДокумент51 страницаRetail Banking Front Office Management Activity For HDFC Bank by Nisha Wadekar This Project Is Very Useful To Studentganeshkhale7052Оценок пока нет

- PMC Bank ProjectДокумент23 страницыPMC Bank ProjectRahul JAGTAP60% (5)

- Innovation in Banking SectorДокумент21 страницаInnovation in Banking Sectoruma2k10Оценок пока нет

- Kotak Mahindra Bank What Makes Kotak Different From Others - A Comparative Story KotakДокумент68 страницKotak Mahindra Bank What Makes Kotak Different From Others - A Comparative Story KotakshiprapathaniaОценок пока нет

- Malaysia: Finance Debt Collateralized Lien Bankruptcy LiquidationДокумент2 страницыMalaysia: Finance Debt Collateralized Lien Bankruptcy LiquidationAkhil UchilОценок пока нет

- Sidbi 39Документ43 страницыSidbi 39HARSHAL PATADEОценок пока нет

- Comparative Analysis On Non Performing Assets of Private and Public Sector BanksДокумент108 страницComparative Analysis On Non Performing Assets of Private and Public Sector BanksAmit SinghОценок пока нет

- Review of LiteratureДокумент2 страницыReview of Literaturepoojasambrekar89% (9)

- QestionnaireДокумент4 страницыQestionnairePreet AmanОценок пока нет

- Synopsis On Home LoanДокумент9 страницSynopsis On Home Loanyash jejaniОценок пока нет

- A Project Report On: A Study On Consumer Satisfaction of Payzapp Wallet With Refrence To City BhindДокумент51 страницаA Project Report On: A Study On Consumer Satisfaction of Payzapp Wallet With Refrence To City Bhindnikhil jОценок пока нет

- Universal Banking Project 2Документ128 страницUniversal Banking Project 2Vishagrah Tyagi33% (6)

- Non-Performing AssestДокумент56 страницNon-Performing AssestKhalid HussainОценок пока нет

- Summer Internship Report On Credit Department of Punjab National BankДокумент20 страницSummer Internship Report On Credit Department of Punjab National Banktanushree saxenaОценок пока нет

- SBI Home Loan TMV BlackbookДокумент106 страницSBI Home Loan TMV Blackbookvishal birajdarОценок пока нет

- Personal Load in SbiДокумент42 страницыPersonal Load in SbiNitinAgnihotriОценок пока нет

- Consumer Satisfaction On Nashik Merchamt BankДокумент40 страницConsumer Satisfaction On Nashik Merchamt BankKunal Hire-Patil100% (2)

- Union Bank of IndiaДокумент33 страницыUnion Bank of Indiaraghavan swaminathanОценок пока нет

- Pooja Patel 70Документ93 страницыPooja Patel 70Mohd Saad HamidaniОценок пока нет

- Comparative Analysis of Home Loans - MДокумент86 страницComparative Analysis of Home Loans - Mdasdebashish82100% (6)

- Sip Project of UbiДокумент75 страницSip Project of UbiArgha MondalОценок пока нет

- Finance (ANALYSIS OF HDFC CAR LOAN'S FINANCE)Документ40 страницFinance (ANALYSIS OF HDFC CAR LOAN'S FINANCE)AneesAnsariОценок пока нет

- Retail Banking An Introduction Research Methodology: Title of Project Statement of The Problem Objective of The StudyДокумент9 страницRetail Banking An Introduction Research Methodology: Title of Project Statement of The Problem Objective of The StudySandeep KumarОценок пока нет

- Study On Retail BankingДокумент47 страницStudy On Retail Bankingzaru1121Оценок пока нет

- Chapter - 1: 1.1 General Introduction About The SectorДокумент23 страницыChapter - 1: 1.1 General Introduction About The SectorAnkur ChopraОценок пока нет

- IndexДокумент15 страницIndexJagdish BambhaniyaОценок пока нет

- A Project Report On Comparison Between HDFC Bank Amp ICICI BankДокумент45 страницA Project Report On Comparison Between HDFC Bank Amp ICICI Bankillusionofsoul_51347Оценок пока нет

- Portfolio Analyis RetailДокумент21 страницаPortfolio Analyis RetailSandeep PatelОценок пока нет

- SM-II Report - Section-C - Group-10 PDFДокумент20 страницSM-II Report - Section-C - Group-10 PDFroguembaОценок пока нет

- Portfolio Analysis - Personal Care - Group 2 - Section C PDFДокумент25 страницPortfolio Analysis - Personal Care - Group 2 - Section C PDFroguemba100% (1)

- Group 10 Section A WalMart Perspective From Porter PDFДокумент3 страницыGroup 10 Section A WalMart Perspective From Porter PDFroguembaОценок пока нет

- SM Report - Section C - Group 1 PDFДокумент18 страницSM Report - Section C - Group 1 PDFroguembaОценок пока нет

- SM Group5 SectionC BHEL PDFДокумент23 страницыSM Group5 SectionC BHEL PDFroguemba100% (1)

- Portfolio Analysis Airline Industry - Group 4 - Section C - SM2 Project PDFДокумент27 страницPortfolio Analysis Airline Industry - Group 4 - Section C - SM2 Project PDFroguembaОценок пока нет

- Portfolio Analysis Commercial VehiclesДокумент25 страницPortfolio Analysis Commercial Vehiclesroguemba100% (1)

- Hotel Industry - Portfolia AnalysisДокумент26 страницHotel Industry - Portfolia Analysisroguemba87% (15)

- Indian Biotechnology Industry - Portfolio AnalysisДокумент15 страницIndian Biotechnology Industry - Portfolio AnalysisroguembaОценок пока нет

- BOP Intervention M-PesaДокумент21 страницаBOP Intervention M-PesaroguembaОценок пока нет

- S.N o Name of Stock Quantit y Purchas e Price Last Traded Price Sale S Pric e Gain Realized/UnrealizedДокумент8 страницS.N o Name of Stock Quantit y Purchas e Price Last Traded Price Sale S Pric e Gain Realized/UnrealizedShreya ChitrakarОценок пока нет

- Bank Reconciliation Statement 70Документ6 страницBank Reconciliation Statement 70xyzОценок пока нет

- RBI Branch and ATM Expansion LiberalizedДокумент9 страницRBI Branch and ATM Expansion LiberalizedbistamasterОценок пока нет

- Corporate FinanceДокумент18 страницCorporate FinanceNishakdasОценок пока нет

- DATA ANALYSIS AND INTERPRETATION of Rain Bow PipesДокумент10 страницDATA ANALYSIS AND INTERPRETATION of Rain Bow Pipesarmeena falakОценок пока нет

- Does Stock Split Influence To Liquidity and Stock ReturnДокумент9 страницDoes Stock Split Influence To Liquidity and Stock ReturnBhavdeepsinh JadejaОценок пока нет

- To The Chief Executive Officer Bank of America N.A. (India Branches)Документ53 страницыTo The Chief Executive Officer Bank of America N.A. (India Branches)aditya tripathiОценок пока нет

- Afar 08Документ14 страницAfar 08RENZEL MAGBITANGОценок пока нет

- ValuationДокумент3 страницыValuationBryan IbarrientosОценок пока нет

- Stock Market and Trading Mechanism: Chapter - 2Документ77 страницStock Market and Trading Mechanism: Chapter - 2Nidhi JajodiaОценок пока нет

- CFP Investment Planning Study Notes SampleДокумент28 страницCFP Investment Planning Study Notes SampleMeenakshi67% (3)

- Money and Banking Week 3Документ16 страницMoney and Banking Week 3Pradipta NarendraОценок пока нет

- Financial Planning ProcessДокумент2 страницыFinancial Planning ProcessJeleen Zurbano PontillasОценок пока нет

- HLB Receipt 289062Документ3 страницыHLB Receipt 289062devanboy 2007Оценок пока нет

- Financial Model For 1 Year MBA - Is It Worth Going For 1 Year MBAДокумент7 страницFinancial Model For 1 Year MBA - Is It Worth Going For 1 Year MBAAnurag SingalОценок пока нет

- CHEQUEmaster ClassДокумент10 страницCHEQUEmaster ClassMohanarajОценок пока нет

- Subunit 3.6 Efficiency Ratio AnalysisДокумент30 страницSubunit 3.6 Efficiency Ratio AnalysisSteam MainОценок пока нет

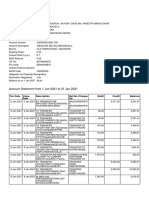

- Sbi Account Jan 2021Документ2 страницыSbi Account Jan 2021Manoj GaurОценок пока нет

- Analysis of Credit Risk, Liquidity and Profitability of The Trade Bank of Iraq For The Period (2012-2021)Документ25 страницAnalysis of Credit Risk, Liquidity and Profitability of The Trade Bank of Iraq For The Period (2012-2021)Ali Abdulhassan AbbasОценок пока нет

- Chapte 1Документ27 страницChapte 1Mary Ann Alegria MorenoОценок пока нет

- Ladrillo Investor PresentationДокумент16 страницLadrillo Investor PresentationMOVIES SHOPОценок пока нет

- Typesof ClearingДокумент3 страницыTypesof ClearingteliumarОценок пока нет

- Crypto Trading Secrets How To Earn Big in The Cryptocurrency MarketДокумент25 страницCrypto Trading Secrets How To Earn Big in The Cryptocurrency MarketSiddharth KaulОценок пока нет

- Schedule of Services and Tariffs: HSBC Jade, HSBC Premier, HSBC Advance and Personal BankingДокумент18 страницSchedule of Services and Tariffs: HSBC Jade, HSBC Premier, HSBC Advance and Personal BankingShadab HussainОценок пока нет

- ELSSДокумент15 страницELSSSecure Plus100% (1)

- Za Test 8 KumarДокумент30 страницZa Test 8 KumarMia Omerika100% (1)

- Chase B Statement-MarДокумент4 страницыChase B Statement-MarЮлия ПОценок пока нет

- Lanka Floortiles PLC - (Tile) - q4 Fy 15 - BuyДокумент9 страницLanka Floortiles PLC - (Tile) - q4 Fy 15 - BuySudheera IndrajithОценок пока нет

- Financial Performance of Kerala Gramin Bank Special Reference To Southern AreaДокумент81 страницаFinancial Performance of Kerala Gramin Bank Special Reference To Southern AreaPriyanka Ramath100% (1)

- The Letter of Credit ProcessДокумент1 страницаThe Letter of Credit ProcessGirish RanganathanОценок пока нет