Вам также может понравиться

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- SANS PowerShell Cheat SheetДокумент9 страницSANS PowerShell Cheat SheetRaistlin MajereОценок пока нет

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- Azure AD Security - 061421Документ44 страницыAzure AD Security - 061421Raistlin Majere100% (1)

- Sophos Threat Report 2022Документ27 страницSophos Threat Report 2022Raistlin MajereОценок пока нет

- The Human Side of Beyond Budgeting Paris 21june2016 FinalДокумент43 страницыThe Human Side of Beyond Budgeting Paris 21june2016 FinalRaistlin MajereОценок пока нет

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Best Memorial (Respondent) - GIMC 2019Документ36 страницBest Memorial (Respondent) - GIMC 2019raj bhoirОценок пока нет

- EBO Report Final PDFДокумент7 страницEBO Report Final PDFHamza AsifОценок пока нет

- Mincer (1958) - Investment in Human Capital and Personal Income DistributionДокумент23 страницыMincer (1958) - Investment in Human Capital and Personal Income DistributionOscar Andree Flores LeonОценок пока нет

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- E14 E19 AnswerДокумент3 страницыE14 E19 Answerjustine reine cornicoОценок пока нет

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Axis Direct PDFДокумент2 страницыAxis Direct PDFMahesh KorrapatiОценок пока нет

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- GHOSTWRITER AUTHOR NDA AGREEMENT - PDF Changes - ShortДокумент1 страницаGHOSTWRITER AUTHOR NDA AGREEMENT - PDF Changes - ShortEmmanuel535100% (3)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Final List of Registered Firms 2021-2023 - Uploaded 25.11.2021 - 1Документ12 страницFinal List of Registered Firms 2021-2023 - Uploaded 25.11.2021 - 1wasikepwОценок пока нет

- 9 Main Causes of Regional Imbalances in IndiaДокумент4 страницы9 Main Causes of Regional Imbalances in IndiaGargi SinhaОценок пока нет

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

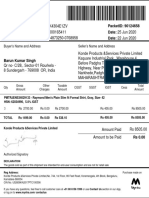

- Myntra Invoice of ShirtДокумент1 страницаMyntra Invoice of ShirtBarun Singh0% (2)

- ESci 14 - Mid TermAДокумент1 страницаESci 14 - Mid TermAje solarteОценок пока нет

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- Splashwall Bathrooms 2021 LowResДокумент19 страницSplashwall Bathrooms 2021 LowResday69walkerОценок пока нет

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (345)

- The Economic Life of Project Is An Asset From The Angle of Maximization of The Project ValueДокумент12 страницThe Economic Life of Project Is An Asset From The Angle of Maximization of The Project ValueUjjwal KheriaОценок пока нет

- Statistics The Second.Документ8 страницStatistics The Second.Oliyad KondalaОценок пока нет

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- SIM WS2022-23 Lec8Документ16 страницSIM WS2022-23 Lec8CarolinaОценок пока нет

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- Simple Gifts For Women in PhilippinesДокумент4 страницыSimple Gifts For Women in PhilippinesLumi candlesОценок пока нет

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- ds11 SpecsheetДокумент4 страницыds11 Specsheet13421301508Оценок пока нет

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- Moa Contract To SellДокумент2 страницыMoa Contract To Selllyndon melvi sumiogОценок пока нет

- Micro 1 1st Test 2021Документ5 страницMicro 1 1st Test 2021Lemi GonfaОценок пока нет

- Sequences A LevelДокумент8 страницSequences A LevelSemaОценок пока нет

- Logo ContractДокумент2 страницыLogo ContractRhonmar CastroОценок пока нет

- An Overview of The Financial Performance of Indian Tyre Industry - Comparison Among Leading Tyre CompaniesДокумент3 страницыAn Overview of The Financial Performance of Indian Tyre Industry - Comparison Among Leading Tyre CompaniesLucky khandelwalОценок пока нет

- Doubtful Accounts Expense Using Allowance Method: SolutionДокумент2 страницыDoubtful Accounts Expense Using Allowance Method: Solutionmade elleОценок пока нет

- Steel ForecastingДокумент33 страницыSteel ForecastingParth TraderОценок пока нет

- A COMPARATIVE STUDY OF OLA AND UBER CUSTOMERS IN DELHI After COVID-19Документ9 страницA COMPARATIVE STUDY OF OLA AND UBER CUSTOMERS IN DELHI After COVID-19trivikram SahuОценок пока нет

- Finacle User Guide IdbiДокумент337 страницFinacle User Guide Idbianjali anjuОценок пока нет

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- A Study On Quality Issues of Construction Industry in MalaysiaДокумент6 страницA Study On Quality Issues of Construction Industry in MalaysiaAlif AffzaОценок пока нет

- Trends Quiz 1-2Документ3 страницыTrends Quiz 1-2Editha RobillosОценок пока нет

- Official Receipt: Baguio de Academia CollegeДокумент11 страницOfficial Receipt: Baguio de Academia CollegeLorgie Khim IslaОценок пока нет

- 3rd Revision Economics EM 12th 2023Документ2 страницы3rd Revision Economics EM 12th 2023Rani muthuselvamОценок пока нет

- Molly Maid ChecklistДокумент1 страницаMolly Maid ChecklistYessОценок пока нет