Вам также может понравиться

- Autonomy PitchbookДокумент23 страницыAutonomy PitchbookZerohedge100% (29)

- Square's Pitch DeckДокумент20 страницSquare's Pitch Deckapi-204718852100% (12)

- Square Pitch DeckДокумент20 страницSquare Pitch DeckAwesome Pitch Company67% (3)

- GenpactДокумент57 страницGenpactAlan JacobОценок пока нет

- DMX Technologies: OverweightДокумент4 страницыDMX Technologies: Overweightstoreroom_02Оценок пока нет

- Infosys: Performance HighlightsДокумент15 страницInfosys: Performance HighlightsAtul ShahiОценок пока нет

- Larsen & ToubroДокумент15 страницLarsen & ToubroAngel BrokingОценок пока нет

- Autonomy Presentation 1 505952Документ14 страницAutonomy Presentation 1 505952Roberto BaldwinОценок пока нет

- Wipro Result UpdatedДокумент16 страницWipro Result UpdatedAngel BrokingОценок пока нет

- Wipro 4Q FY 2013Документ15 страницWipro 4Q FY 2013Angel BrokingОценок пока нет

- HCLTech 3Q FY13Документ16 страницHCLTech 3Q FY13Angel BrokingОценок пока нет

- HCL Technologies: Performance HighlightsДокумент15 страницHCL Technologies: Performance HighlightsAngel BrokingОценок пока нет

- Infosys Result UpdatedДокумент14 страницInfosys Result UpdatedAngel BrokingОценок пока нет

- A Study On The Effects of Program Trading On KOSPI and KOSPI200 Futures Market in KoreaДокумент12 страницA Study On The Effects of Program Trading On KOSPI and KOSPI200 Futures Market in KoreaRahul PinnamaneniОценок пока нет

- Infosys: Performance HighlightsДокумент15 страницInfosys: Performance HighlightsAngel BrokingОценок пока нет

- ITG TCA - Koscom Seminar March 2013Документ32 страницыITG TCA - Koscom Seminar March 2013smallakeОценок пока нет

- Infosys: Performance HighlightsДокумент15 страницInfosys: Performance HighlightsAngel BrokingОценок пока нет

- BM&F Bovespa 2Q08 Earnings Conference Call August 15thДокумент31 страницаBM&F Bovespa 2Q08 Earnings Conference Call August 15thBVMF_RIОценок пока нет

- Mphasis: Performance HighlightsДокумент13 страницMphasis: Performance HighlightsAngel BrokingОценок пока нет

- Global Sourcing - A Strategic Business ActivityДокумент65 страницGlobal Sourcing - A Strategic Business ActivityamohuidromОценок пока нет

- Clearsight Monitor - Professional Services Industry UpdateДокумент9 страницClearsight Monitor - Professional Services Industry UpdateClearsight AdvisorsОценок пока нет

- Mphasis 1Q FY2013 01.03.13Документ13 страницMphasis 1Q FY2013 01.03.13Angel BrokingОценок пока нет

- Mahindra Satyam, 4th February, 2013Документ12 страницMahindra Satyam, 4th February, 2013Angel BrokingОценок пока нет

- Wipro Result UpdatedДокумент14 страницWipro Result UpdatedAngel BrokingОценок пока нет

- Full Sal Surv 09Документ12 страницFull Sal Surv 09Elie Edmond IranyОценок пока нет

- HCL Technologies: Performance HighlightsДокумент15 страницHCL Technologies: Performance HighlightsAngel BrokingОценок пока нет

- Asian Paints: Hues of GrowthДокумент9 страницAsian Paints: Hues of GrowthAnonymous y3hYf50mTОценок пока нет

- Mind TreeДокумент16 страницMind TreeAngel BrokingОценок пока нет

- 3i Infotech: Performance HighlightsДокумент9 страниц3i Infotech: Performance HighlightsVОценок пока нет

- Infosys 4Q FY 2013, 12.04.13Документ15 страницInfosys 4Q FY 2013, 12.04.13Angel BrokingОценок пока нет

- Street Rating MicrosoftДокумент5 страницStreet Rating MicrosoftEric LeОценок пока нет

- Satyam 4Q FY 2013Документ12 страницSatyam 4Q FY 2013Angel BrokingОценок пока нет

- Microsoft Financial AnalysisДокумент30 страницMicrosoft Financial AnalysisVijayKumar Nishad50% (2)

- Development Credit Bank Limited: February, 2008Документ35 страницDevelopment Credit Bank Limited: February, 2008Ashutosh TiwariОценок пока нет

- ITC Result UpdatedДокумент15 страницITC Result UpdatedAngel BrokingОценок пока нет

- BaiduДокумент29 страницBaiduidradjatОценок пока нет

- Majesco: Muted Show, Thesis UnchangedДокумент11 страницMajesco: Muted Show, Thesis UnchangedAnonymous y3hYf50mTОценок пока нет

- Tech Mahindra: Performance HighlightsДокумент11 страницTech Mahindra: Performance HighlightsAngel BrokingОценок пока нет

- Responsive Document - CREW: Department of Education: Regarding For-Profit Education: 8/16/2011 - OUS 11-00026 - 2Документ750 страницResponsive Document - CREW: Department of Education: Regarding For-Profit Education: 8/16/2011 - OUS 11-00026 - 2CREWОценок пока нет

- Mphasis Result UpdatedДокумент12 страницMphasis Result UpdatedAngel BrokingОценок пока нет

- Infosys: A Bumpy Road, To Success!Документ12 страницInfosys: A Bumpy Road, To Success!Dinesh ChoudharyОценок пока нет

- Times Presentation Feb 28, 2011Документ30 страницTimes Presentation Feb 28, 2011Soumitro GangulyОценок пока нет

- HCL Technologies Q3FY11 Result UpdateДокумент4 страницыHCL Technologies Q3FY11 Result Updaterajarun85Оценок пока нет

- Financial PlanДокумент10 страницFinancial Planapi-25978665Оценок пока нет

- Square Pitch DeckДокумент20 страницSquare Pitch DeckSteve PolandОценок пока нет

- Matrix 2Документ2 страницыMatrix 2Devendra SharmaОценок пока нет

- Tech Mahindra: Performance HighlightsДокумент11 страницTech Mahindra: Performance HighlightsAngel BrokingОценок пока нет

- Persistent Systems LTD.: IT Services - Q3 FY12 Result Update 27 January 2012Документ4 страницыPersistent Systems LTD.: IT Services - Q3 FY12 Result Update 27 January 2012shahavОценок пока нет

- Bartronics Anand RathiДокумент2 страницыBartronics Anand RathisanjeevmohankapoorОценок пока нет

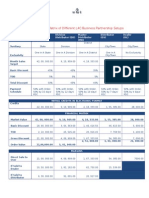

- Commercial Matrix of Different L4C Business Partnership SetupsДокумент2 страницыCommercial Matrix of Different L4C Business Partnership SetupsDevendra SharmaОценок пока нет

- CSE Annual Report 2010Документ76 страницCSE Annual Report 2010Dhananjaya HathurusingheОценок пока нет

- Conference Call TranscriptДокумент20 страницConference Call TranscriptHimanshu BhambhaniОценок пока нет

- Bold Thinking: Robert H. Hacker Cincinnati, Oh OCTOBER 24-25, 2009Документ42 страницыBold Thinking: Robert H. Hacker Cincinnati, Oh OCTOBER 24-25, 2009api-25978665Оценок пока нет

- Wipro LTD: Disappointing Writ All OverДокумент6 страницWipro LTD: Disappointing Writ All OverswetasagarОценок пока нет

- The Revenue Acceleration Rules: Supercharge Sales and Marketing Through Artificial Intelligence, Predictive Technologies and Account-Based StrategiesОт EverandThe Revenue Acceleration Rules: Supercharge Sales and Marketing Through Artificial Intelligence, Predictive Technologies and Account-Based StrategiesОценок пока нет

- Economic Indicators for Southeastern Asia and the Pacific: Input–Output TablesОт EverandEconomic Indicators for Southeastern Asia and the Pacific: Input–Output TablesОценок пока нет

- Robotic Process Automation (RPA) in the Financial Sector: Technology - Implementation - Success For Decision Makers and UsersОт EverandRobotic Process Automation (RPA) in the Financial Sector: Technology - Implementation - Success For Decision Makers and UsersОценок пока нет

- Aid for Trade in Asia and the Pacific: Promoting Economic Diversification and EmpowermentОт EverandAid for Trade in Asia and the Pacific: Promoting Economic Diversification and EmpowermentОценок пока нет

- Benefits Realisation Management: The Benefit Manager's Desktop Step-by-Step GuideОт EverandBenefits Realisation Management: The Benefit Manager's Desktop Step-by-Step GuideОценок пока нет

- Financial Ratio Tree (Deb Sahoo)Документ1 страницаFinancial Ratio Tree (Deb Sahoo)Deb SahooОценок пока нет

- Option Trading Workbook (Deb Sahoo)Документ25 страницOption Trading Workbook (Deb Sahoo)Deb SahooОценок пока нет

- 2010 - 2012 VC LandscapeДокумент2 страницы2010 - 2012 VC LandscapeDeb SahooОценок пока нет

- EVA Tree Analysis of Financial Statement (Deb Sahoo)Документ3 страницыEVA Tree Analysis of Financial Statement (Deb Sahoo)Deb SahooОценок пока нет

- Perpetual License vs. SaaS Revenue ModelДокумент1 страницаPerpetual License vs. SaaS Revenue ModelDeb SahooОценок пока нет

- Merger of Microsoft and Adobe (Deb Sahoo)Документ43 страницыMerger of Microsoft and Adobe (Deb Sahoo)Deb SahooОценок пока нет

- Merger of Qualcomm and Atheros (Deb Sahoo)Документ44 страницыMerger of Qualcomm and Atheros (Deb Sahoo)Deb SahooОценок пока нет