Вам также может понравиться

- User Manual - UM EN ILC 1XX (7805 - en - 06) PDFДокумент86 страницUser Manual - UM EN ILC 1XX (7805 - en - 06) PDFingezoneОценок пока нет

- The5 - 264831 (Group C)Документ2 страницыThe5 - 264831 (Group C)Rubiatul AdawiyahОценок пока нет

- LG Technical Manual PDFДокумент31 страницаLG Technical Manual PDFfarhadzakerОценок пока нет

- Zoomlion Service Satisfaction Questionnaire (2015)Документ4 страницыZoomlion Service Satisfaction Questionnaire (2015)मुकेश कुमार झाОценок пока нет

- PLC Synchrocloser EPECДокумент8 страницPLC Synchrocloser EPECDaniel FloresОценок пока нет

- LG 21FU1RLX Service ManualДокумент22 страницыLG 21FU1RLX Service Manualuzenho100% (1)

- Mind Reading and Mind Control Technologies Are Coming 10th ED February 14, 2021Документ6 страницMind Reading and Mind Control Technologies Are Coming 10th ED February 14, 2021JusticeTIОценок пока нет

- En LG-C333 SVC Eng 120824 PDFДокумент181 страницаEn LG-C333 SVC Eng 120824 PDFSergio MesquitaОценок пока нет

- Manhinh KX PDFДокумент49 страницManhinh KX PDFĐoàn Văn MinhОценок пока нет

- Ak731 606 00 0 2PLC1Документ138 страницAk731 606 00 0 2PLC1Francisco MunguíaОценок пока нет

- Sheave Replacement ProcedureДокумент3 страницыSheave Replacement Procedureमुकेश कुमार झाОценок пока нет

- Ua22c4000p PDFДокумент81 страницаUa22c4000p PDFI Ketut Maryata Tanaya100% (1)

- E P e C Machine ControllerДокумент92 страницыE P e C Machine Controllerkishan1234Оценок пока нет

- Daikin Troubleshooting GuideДокумент2 страницыDaikin Troubleshooting Guidenvn87Оценок пока нет

- Option Overview: Making Modern Living PossibleДокумент12 страницOption Overview: Making Modern Living PossibleMecatroscarОценок пока нет

- FR-D700 - Presentation 1207Документ23 страницыFR-D700 - Presentation 1207Jilani HayderОценок пока нет

- Embedded Control System For Agricultural Machinery Implemented in Forage HarvestingДокумент78 страницEmbedded Control System For Agricultural Machinery Implemented in Forage HarvestingHotib PerwiraОценок пока нет

- Awelco Welder 5679 80a SCH PDFДокумент1 страницаAwelco Welder 5679 80a SCH PDFGoguredОценок пока нет

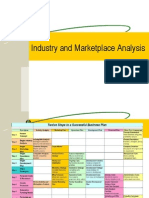

- Industry & Market Place AnalysisДокумент20 страницIndustry & Market Place AnalysisEfriantary NurdianaОценок пока нет

- Competitor ChartДокумент6 страницCompetitor ChartMike FelberОценок пока нет

- BKAA3023 Take Home Exercise 6: Rubiatul Adawiyah Binti Mohd Ashari (264831) Group CДокумент2 страницыBKAA3023 Take Home Exercise 6: Rubiatul Adawiyah Binti Mohd Ashari (264831) Group CRubiatul AdawiyahОценок пока нет

- IGBT - ApplicationManual - E GOOOOOD TO UNDERSTANDING PDFДокумент16 страницIGBT - ApplicationManual - E GOOOOOD TO UNDERSTANDING PDFDoDuyBacОценок пока нет

- Extreme Performance Engine Control: M-12650-C80 M-12650-C81Документ197 страницExtreme Performance Engine Control: M-12650-C80 M-12650-C81Riadalg RiadОценок пока нет

- Competition Commission Vehicle Repair GuidelinesДокумент23 страницыCompetition Commission Vehicle Repair GuidelinesBusinessTech75% (4)

- LG LWHD1006R Training ManualДокумент44 страницыLG LWHD1006R Training ManualGuillermo HernandezОценок пока нет

- 7 Service Manual - LG - Le50Документ83 страницы7 Service Manual - LG - Le50Soporte Tecnico Buenos AiresОценок пока нет

- 6 Axle DrawbarДокумент2 страницы6 Axle DrawbarСергейОценок пока нет

- Service Manual: Model SeriesДокумент48 страницService Manual: Model SeriesEnrique HerreraОценок пока нет

- GOT2000 Technical Presentation 2015Документ41 страницаGOT2000 Technical Presentation 2015Tarek KhafagaОценок пока нет

- 8997 0218 00 DrawingsДокумент127 страниц8997 0218 00 DrawingsAngel Sanchez VilcaОценок пока нет

- Home Product Competitor Comparison 7-24-2013Документ3 страницыHome Product Competitor Comparison 7-24-2013Mitchell BemrichОценок пока нет

- Diagnostic: Educational-GoalsДокумент17 страницDiagnostic: Educational-GoalsPedro TiagoОценок пока нет

- Sales Training - Ingenio Max 200-500 KvaДокумент59 страницSales Training - Ingenio Max 200-500 KvaSayemAbusadatОценок пока нет

- Ifrs Usgaap NotesДокумент38 страницIfrs Usgaap Notesaum_thai100% (1)

- Healthy Balance of Payment in SingaporeДокумент2 страницыHealthy Balance of Payment in SingaporeMichael Loh100% (1)

- Aocp PDFДокумент38 страницAocp PDFSANJAYKUMAR chaudharyОценок пока нет

- C18 Generator Set Electrical System With Emcpii, Emcpii+ and Emcp 3Документ2 страницыC18 Generator Set Electrical System With Emcpii, Emcpii+ and Emcp 3Adetunji TaiwoОценок пока нет

- SM ch11Документ15 страницSM ch11derfzzОценок пока нет

- Aeb SM CH11 1 PDFДокумент16 страницAeb SM CH11 1 PDFAdi SusiloОценок пока нет

- Aeb SM CH11 1Документ15 страницAeb SM CH11 1Crytal AbubakarОценок пока нет

- Solution Manual For Auditing and Assurance Services 17th Edition Alvin A Arens Randal J Elder Mark S Beasley Chris e HoganДокумент31 страницаSolution Manual For Auditing and Assurance Services 17th Edition Alvin A Arens Randal J Elder Mark S Beasley Chris e HoganMeredithFleminggztay100% (79)

- Arens Auditing16e SM 10Документ30 страницArens Auditing16e SM 10김현중100% (1)

- Solution Manual For Auditing and Assurance Services 17th by ArensДокумент32 страницыSolution Manual For Auditing and Assurance Services 17th by ArensMeredithFleminggztay99% (81)

- Assessing and Responding To Fraud Risks: Concept Checks P. 281Документ30 страницAssessing and Responding To Fraud Risks: Concept Checks P. 281Eileen HUANGОценок пока нет

- Solution Manual Auditing and Assurance Services 13e by Arens Chapter 11Документ16 страницSolution Manual Auditing and Assurance Services 13e by Arens Chapter 11MahediОценок пока нет

- Assessing and Responding To Fraud RisksДокумент7 страницAssessing and Responding To Fraud RisksRisal EfendiОценок пока нет

- Chapter 3 - Auditors' ResponsibilityДокумент51 страницаChapter 3 - Auditors' ResponsibilityddddddaaaaeeeeОценок пока нет

- PP FF Auditoria Clase 4Документ173 страницыPP FF Auditoria Clase 4Tony amador gonzalezОценок пока нет

- Definition of Fraud 1-3Документ3 страницыDefinition of Fraud 1-3Nada An-NaurahОценок пока нет

- Ch11 SolutionsДокумент5 страницCh11 Solutionsjackroy1406Оценок пока нет

- Chapter 3 - Assignment - Marcellana, Ariel P. - Bsa-31Документ5 страницChapter 3 - Assignment - Marcellana, Ariel P. - Bsa-31Marcellana ArianeОценок пока нет

- Chapter 2 Note Audit From The Book. Learning Object 1 Define The Various Types of Fraud That Affect OrganizationДокумент12 страницChapter 2 Note Audit From The Book. Learning Object 1 Define The Various Types of Fraud That Affect OrganizationkimkimОценок пока нет

- CH 14Документ5 страницCH 14Kurt Del RosarioОценок пока нет

- Auditig Chapter 6Документ16 страницAuditig Chapter 6A A AYU SINTA JAYANTIОценок пока нет

- CHAPTER 3 - AudTheoДокумент6 страницCHAPTER 3 - AudTheoVicente, Liza Mae C.Оценок пока нет

- Fraud Detection and PreventionДокумент5 страницFraud Detection and PreventionIrsani KurniatiОценок пока нет

- PrE1 Auditor's ResponsibityДокумент17 страницPrE1 Auditor's ResponsibityAbegail Kaye BiadoОценок пока нет

- Updated Report AUDITINGДокумент9 страницUpdated Report AUDITINGJanelleОценок пока нет

- Chap 14 Corp Gov Biasura Jhazreel 2 BДокумент6 страницChap 14 Corp Gov Biasura Jhazreel 2 BJhazreel BiasuraОценок пока нет

- Auditor's Responsibility (Fraud and Error)Документ5 страницAuditor's Responsibility (Fraud and Error)Maria Beatriz MundaОценок пока нет

- Aeb SM CH23 2Документ17 страницAeb SM CH23 2jg2128100% (1)

- Aeb SM CH26 1Документ14 страницAeb SM CH26 1jg2128Оценок пока нет

- Aeb SM CH24 1Документ30 страницAeb SM CH24 1jg2128100% (1)

- Aeb SM CH25 1Документ16 страницAeb SM CH25 1jg2128100% (1)

- Aeb SM CH20 1Документ22 страницыAeb SM CH20 1jg2128Оценок пока нет

- Aeb SM CH22 1Документ19 страницAeb SM CH22 1jg2128Оценок пока нет

- Aeb SM CH15 1Документ25 страницAeb SM CH15 1jg2128Оценок пока нет

- Aeb SM CH19 1Документ22 страницыAeb SM CH19 1jg2128100% (1)

- Aeb SM CH21 1Документ26 страницAeb SM CH21 1jg2128100% (2)

- Aeb SM CH17 1Документ28 страницAeb SM CH17 1jg2128Оценок пока нет

- Aeb SM CH18 1Документ37 страницAeb SM CH18 1jg2128100% (3)

- AEB SM aFM 2Документ5 страницAEB SM aFM 2jg2128Оценок пока нет

- Aeb SM CH13 2Документ22 страницыAeb SM CH13 2jg2128100% (1)

- Aeb SM CH14 1Документ38 страницAeb SM CH14 1jg2128100% (1)

- Aeb SM CH06 1Документ19 страницAeb SM CH06 1jg2128Оценок пока нет

- Aeb SM CH10 1Документ27 страницAeb SM CH10 1jg2128Оценок пока нет

- AEB SM Ch09 1Документ28 страницAEB SM Ch09 1jg2128Оценок пока нет

- Aeb SM CH07 1Документ24 страницыAeb SM CH07 1jg2128Оценок пока нет

- Aeb SM CH08 1Документ41 страницаAeb SM CH08 1jg2128Оценок пока нет

- Aeb SM CH05 1Документ14 страницAeb SM CH05 1jg2128Оценок пока нет

- Aeb SM CH03 1Документ25 страницAeb SM CH03 1jg2128Оценок пока нет

- Working Capital FinancingДокумент80 страницWorking Capital FinancingArjun John100% (1)

- 2.1 Song of The Open RoadДокумент10 страниц2.1 Song of The Open RoadHariom yadavОценок пока нет

- Ecology Block Wall CollapseДокумент14 страницEcology Block Wall CollapseMahbub KhanОценок пока нет

- Philippine Phoenix Surety vs. WoodworksДокумент1 страницаPhilippine Phoenix Surety vs. WoodworksSimon James SemillaОценок пока нет

- SWOT Analysis and Competion of Mangola Soft DrinkДокумент2 страницыSWOT Analysis and Competion of Mangola Soft DrinkMd. Saiful HoqueОценок пока нет

- Government Arsenal Safety and Security OfficeДокумент5 страницGovernment Arsenal Safety and Security OfficeMark Alfred MungcalОценок пока нет

- My Portfolio: Marie Antonette S. NicdaoДокумент10 страницMy Portfolio: Marie Antonette S. NicdaoLexelyn Pagara RivaОценок пока нет

- Carl Rogers Written ReportsДокумент3 страницыCarl Rogers Written Reportskyla elpedangОценок пока нет

- The Absent Presence of Progressive Rock in The British Music Press 1968 1974 PDFДокумент33 страницыThe Absent Presence of Progressive Rock in The British Music Press 1968 1974 PDFwago_itОценок пока нет

- Viking Solid Cone Spray NozzleДокумент13 страницViking Solid Cone Spray NozzlebalaОценок пока нет

- People vs. Tampus DigestДокумент2 страницыPeople vs. Tampus Digestcmv mendozaОценок пока нет

- Concept Note TemplateДокумент2 страницыConcept Note TemplateDHYANA_1376% (17)

- Module 2. Lesson 2. OverexploitationДокумент11 страницModule 2. Lesson 2. OverexploitationJephthah Faith Adorable-PalicОценок пока нет

- Zero Hedge - On A Long Enough Timeline The Survival Rate For Everyone Drops To Zero PDFДокумент5 страницZero Hedge - On A Long Enough Timeline The Survival Rate For Everyone Drops To Zero PDFcaldaseletronica280Оценок пока нет

- First Online Counselling CutoffДокумент2 страницыFirst Online Counselling CutoffJaskaranОценок пока нет

- Tok SB Ibdip Ch1Документ16 страницTok SB Ibdip Ch1Luis Andrés Arce SalazarОценок пока нет

- Detailed Lesson PlanДокумент6 страницDetailed Lesson PlanMa. ChrizelОценок пока нет

- BB Winning Turbulence Lessons Gaining Groud TimesДокумент4 страницыBB Winning Turbulence Lessons Gaining Groud TimesGustavo MicheliniОценок пока нет

- What Is OB Chapter1Документ25 страницWhat Is OB Chapter1sun_shenoy100% (1)

- Advanced Stock Trading Course + Strategies Course CatalogДокумент5 страницAdvanced Stock Trading Course + Strategies Course Catalogmytemp_01Оценок пока нет

- British Airways Vs CAДокумент17 страницBritish Airways Vs CAGia DimayugaОценок пока нет

- AKL - Pert 2-2Документ2 страницыAKL - Pert 2-2Astri Ririn ErnawatiОценок пока нет

- HP Compaq Presario c700 - Compal La-4031 Jbl81 - Rev 1.0 - ZouaveДокумент42 страницыHP Compaq Presario c700 - Compal La-4031 Jbl81 - Rev 1.0 - ZouaveYonny MunozОценок пока нет

- Periodical Test - English 5 - Q1Документ7 страницPeriodical Test - English 5 - Q1Raymond O. BergadoОценок пока нет

- EZ 220 Songbook Web PDFДокумент152 страницыEZ 220 Songbook Web PDFOscar SpiritОценок пока нет

- Torts ProjectДокумент20 страницTorts ProjectpriyaОценок пока нет

- NRes1 Work Activity 1 - LEGARTEДокумент4 страницыNRes1 Work Activity 1 - LEGARTEJuliana LegarteОценок пока нет

- Profile Story On Survivor Contestant Trish DunnДокумент6 страницProfile Story On Survivor Contestant Trish DunnMeganGraceLandauОценок пока нет

- Swami VivekanandaДокумент20 страницSwami VivekanandaRitusharma75Оценок пока нет

- Buyer - Source To Contracts - English - 25 Apr - v4Документ361 страницаBuyer - Source To Contracts - English - 25 Apr - v4ardiannikko0Оценок пока нет

- (ISC)2 CISSP Certified Information Systems Security Professional Official Study GuideОт Everand(ISC)2 CISSP Certified Information Systems Security Professional Official Study GuideРейтинг: 2.5 из 5 звезд2.5/5 (2)

- A Pocket Guide to Risk Mathematics: Key Concepts Every Auditor Should KnowОт EverandA Pocket Guide to Risk Mathematics: Key Concepts Every Auditor Should KnowОценок пока нет

- Guide: SOC 2 Reporting on an Examination of Controls at a Service Organization Relevant to Security, Availability, Processing Integrity, Confidentiality, or PrivacyОт EverandGuide: SOC 2 Reporting on an Examination of Controls at a Service Organization Relevant to Security, Availability, Processing Integrity, Confidentiality, or PrivacyОценок пока нет

- Business Process Mapping: Improving Customer SatisfactionОт EverandBusiness Process Mapping: Improving Customer SatisfactionРейтинг: 5 из 5 звезд5/5 (1)

- Bribery and Corruption Casebook: The View from Under the TableОт EverandBribery and Corruption Casebook: The View from Under the TableОценок пока нет

- Frequently Asked Questions in International Standards on AuditingОт EverandFrequently Asked Questions in International Standards on AuditingРейтинг: 1 из 5 звезд1/5 (1)

- GDPR-standard data protection staff training: What employees & associates need to know by Dr Paweł MielniczekОт EverandGDPR-standard data protection staff training: What employees & associates need to know by Dr Paweł MielniczekОценок пока нет

- A Step By Step Guide: How to Perform Risk Based Internal Auditing for Internal Audit BeginnersОт EverandA Step By Step Guide: How to Perform Risk Based Internal Auditing for Internal Audit BeginnersРейтинг: 4.5 из 5 звезд4.5/5 (11)

- Financial Statement Fraud Casebook: Baking the Ledgers and Cooking the BooksОт EverandFinancial Statement Fraud Casebook: Baking the Ledgers and Cooking the BooksРейтинг: 4 из 5 звезд4/5 (1)

- Scrum Certification: All In One, The Ultimate Guide To Prepare For Scrum Exams And Get Certified. Real Practice Test With Detailed Screenshots, Answers And ExplanationsОт EverandScrum Certification: All In One, The Ultimate Guide To Prepare For Scrum Exams And Get Certified. Real Practice Test With Detailed Screenshots, Answers And ExplanationsОценок пока нет

- The Layman's Guide GDPR Compliance for Small Medium BusinessОт EverandThe Layman's Guide GDPR Compliance for Small Medium BusinessРейтинг: 5 из 5 звезд5/5 (1)

- Executive Roadmap to Fraud Prevention and Internal Control: Creating a Culture of ComplianceОт EverandExecutive Roadmap to Fraud Prevention and Internal Control: Creating a Culture of ComplianceРейтинг: 4 из 5 звезд4/5 (1)

- GDPR for DevOp(Sec) - The laws, Controls and solutionsОт EverandGDPR for DevOp(Sec) - The laws, Controls and solutionsРейтинг: 5 из 5 звезд5/5 (1)

- Audit and Assurance Essentials: For Professional Accountancy ExamsОт EverandAudit and Assurance Essentials: For Professional Accountancy ExamsОценок пока нет

- Mastering Internal Audit Fundamentals A Step-by-Step ApproachОт EverandMastering Internal Audit Fundamentals A Step-by-Step ApproachРейтинг: 4 из 5 звезд4/5 (1)