Вам также может понравиться

- SWOT N PORTER 5 Forces - Indian PahrmaДокумент21 страницаSWOT N PORTER 5 Forces - Indian Pahrmabhupendraa97% (35)

- Company:Flipkart: Presentation:Compensation ManagementДокумент22 страницыCompany:Flipkart: Presentation:Compensation ManagementNileNdratiger NiLu0% (1)

- Retail Market Stratetegy Final 5th July PDFДокумент40 страницRetail Market Stratetegy Final 5th July PDFmayur6790Оценок пока нет

- RetailДокумент25 страницRetailjayesh78149062100% (2)

- Zane Cycles Case, Video QuestionsДокумент2 страницыZane Cycles Case, Video QuestionsVageesh KumarОценок пока нет

- Retail MarketingДокумент87 страницRetail MarketingsayiviswadevanОценок пока нет

- B2B Module Outline 2010-11 Recovered)Документ10 страницB2B Module Outline 2010-11 Recovered)Sandip KhairnarОценок пока нет

- Balanced Scorecard and Strategy DesignДокумент5 страницBalanced Scorecard and Strategy DesignMark KellyОценок пока нет

- SWOT-Reliance Digital: StrengthsДокумент2 страницыSWOT-Reliance Digital: StrengthsAldrinОценок пока нет

- Whirlpool's E-Business Initiatives Cut Costs and Improved EfficiencyДокумент5 страницWhirlpool's E-Business Initiatives Cut Costs and Improved EfficiencyAnonymous kayEII5NОценок пока нет

- Aswin 80303180002Документ12 страницAswin 80303180002Shambhawi Sinha100% (1)

- B2B Module Assignment Case 2010-11Документ4 страницыB2B Module Assignment Case 2010-11Faram Medhora0% (1)

- Merchandise PlanningДокумент31 страницаMerchandise PlanningAvinaash Pollepalli100% (1)

- Focus On High-Quality Products and Digital ServicesДокумент4 страницыFocus On High-Quality Products and Digital ServicesYugeshJadiyaОценок пока нет

- Service Marketing Lecture of Chapter 1 (4th Edition)Документ24 страницыService Marketing Lecture of Chapter 1 (4th Edition)Biplob SarkarОценок пока нет

- STR348 - Week 2 - Introduction To Operations ManagementДокумент31 страницаSTR348 - Week 2 - Introduction To Operations ManagementMeglena Velevska50% (2)

- 1.basics of Retailing - 1Документ27 страниц1.basics of Retailing - 1anshushah_144850168Оценок пока нет

- Quality Related Aspects of A SupermarketДокумент52 страницыQuality Related Aspects of A SupermarketSandeep100% (4)

- Altria GroupДокумент3 страницыAltria Groupmonika sharmaОценок пока нет

- Category ManagementДокумент14 страницCategory ManagementRita Chatterji100% (1)

- HOLISTIC MARKETING: INFOSYS' INTEGRATED APPROACHДокумент15 страницHOLISTIC MARKETING: INFOSYS' INTEGRATED APPROACHsrijraj100% (1)

- Majid Al Futtaim Hypermarkets GeorgiaДокумент12 страницMajid Al Futtaim Hypermarkets GeorgiaGiga KutkhashviliОценок пока нет

- A System Study in Big BazarДокумент11 страницA System Study in Big BazarDivyaThilakanОценок пока нет

- Retail ManagementДокумент22 страницыRetail ManagementSharath Unnikrishnan Jyothi NairОценок пока нет

- Gaps Model of Service QualityДокумент43 страницыGaps Model of Service QualitySahil GuptaОценок пока нет

- Introduction To Retailing by Sumit ChangesДокумент118 страницIntroduction To Retailing by Sumit Changesshaswat ghildiyalОценок пока нет

- A Life Without Kulhad ChaiДокумент2 страницыA Life Without Kulhad ChaiHritik ShoranОценок пока нет

- FordДокумент11 страницFordAbhimanyu BhardwajОценок пока нет

- Archies Case GroupДокумент17 страницArchies Case GroupVenugopal NairОценок пока нет

- India PostДокумент38 страницIndia PostPravendraSinghОценок пока нет

- Media General - Balance ScorecardДокумент16 страницMedia General - Balance ScorecardSailesh Kumar Patel86% (7)

- An Overview of Revenue ManagementДокумент22 страницыAn Overview of Revenue ManagementThefoodiesway100% (1)

- Brand Audit TitanДокумент33 страницыBrand Audit TitanChetan Panara100% (1)

- Reliance Retail Presentation PDFДокумент32 страницыReliance Retail Presentation PDFRatnesh SinghОценок пока нет

- Reliance Fresh vs SPAR: Comparing India's Top SupermarketsДокумент42 страницыReliance Fresh vs SPAR: Comparing India's Top SupermarketsSiddharth Mohan100% (1)

- 1st Interim Report (DM 06 024)Документ6 страниц1st Interim Report (DM 06 024)Vishnu Vardhan Reddy DaripallyОценок пока нет

- Precision Turned Products World Summary: Market Values & Financials by CountryОт EverandPrecision Turned Products World Summary: Market Values & Financials by CountryОценок пока нет

- CromaДокумент18 страницCromaAditya MaluОценок пока нет

- Session 3 Framework of Production ManagementДокумент7 страницSession 3 Framework of Production ManagementNarayana Reddy100% (1)

- Information Systems in Big Bazaar RetailДокумент27 страницInformation Systems in Big Bazaar RetailHemant Saraf0% (1)

- Group 3 Sales - Airtel FinalДокумент17 страницGroup 3 Sales - Airtel FinalDivya YadavОценок пока нет

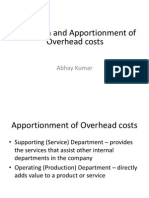

- Overhead Cost Allocation Methods for Support DepartmentsДокумент37 страницOverhead Cost Allocation Methods for Support Departmentsvaibhavmakkar54Оценок пока нет

- CRM Manager RoleДокумент2 страницыCRM Manager RoleCarlos GonzalezОценок пока нет

- Final Retail - Market SegmentationДокумент40 страницFinal Retail - Market Segmentationnavdeep984Оценок пока нет

- Deepak Parth Vidya Harish Neha WinstonДокумент42 страницыDeepak Parth Vidya Harish Neha WinstonParth PatelОценок пока нет

- mkt350 Kotler Chapter 2Документ67 страницmkt350 Kotler Chapter 2BabarKalamОценок пока нет

- Pantaloons Supply Chain: By: Mayank Kapoor (501/2018) Saumya Agarwal (504/2018) Lokesh Lochav (505/2018)Документ6 страницPantaloons Supply Chain: By: Mayank Kapoor (501/2018) Saumya Agarwal (504/2018) Lokesh Lochav (505/2018)Mayank kapoorОценок пока нет

- Introduction To CRMДокумент7 страницIntroduction To CRMalabotshubhangОценок пока нет

- Lecture Note - Retail Management - (Marketing Specialisaion) PDFДокумент51 страницаLecture Note - Retail Management - (Marketing Specialisaion) PDFShaini EkkaОценок пока нет

- Customer Relationship ManagementДокумент17 страницCustomer Relationship Managementdeepak balokhraОценок пока нет

- Smart GoalsДокумент25 страницSmart GoalsZeeshan KaramatОценок пока нет

- Balanced Score CardДокумент14 страницBalanced Score CardAbhishek Mittal50% (2)

- Spencers Hyper Market ReportДокумент35 страницSpencers Hyper Market ReportPranveer ShekhawatОценок пока нет

- Supply Chain Management: A Comparative Study Between Large Organized Food and Grocery Retailers in IndiaДокумент211 страницSupply Chain Management: A Comparative Study Between Large Organized Food and Grocery Retailers in IndiaSachin Kumar Ahuja100% (1)

- Airtel Marketing MyopiaДокумент36 страницAirtel Marketing MyopiaBaskar NarayananОценок пока нет

- Presentation On Bharti AirtelДокумент36 страницPresentation On Bharti AirtelMohit ChaubeyОценок пока нет

- Price Wars in Telecommunications IndustryДокумент4 страницыPrice Wars in Telecommunications IndustryvishalchanduОценок пока нет

- Credit Research Report: Team 545Документ22 страницыCredit Research Report: Team 545D Ban ChoОценок пока нет

- Reliance Communication BCPДокумент11 страницReliance Communication BCPat118Оценок пока нет

- OpenSees Navigator GUIДокумент52 страницыOpenSees Navigator GUIjames_frankОценок пока нет

- Sathyabama: (Deemed To Be University)Документ3 страницыSathyabama: (Deemed To Be University)viktahjmОценок пока нет

- Bad To The Bone BeagleBone and BeagleBone Black BookДокумент425 страницBad To The Bone BeagleBone and BeagleBone Black Bookart100% (8)

- Microsoft Word 2016 Topics Word Basics: Getting Started With WordДокумент8 страницMicrosoft Word 2016 Topics Word Basics: Getting Started With WordMadelaine Dandan NiduaОценок пока нет

- Adaptive QuadratureДокумент35 страницAdaptive QuadratureMarsetiayuNingsih100% (1)

- Introduction Network AnalystДокумент67 страницIntroduction Network AnalystElmerCalizayaLlatasiОценок пока нет

- HTML markup guideДокумент2 страницыHTML markup guidefcmitcОценок пока нет

- Essential ETAP Features for Power System Modeling and AnalysisДокумент4 страницыEssential ETAP Features for Power System Modeling and AnalysissurajОценок пока нет

- L2 Lexical AnalysisДокумент59 страницL2 Lexical AnalysisDhruv PasrichaОценок пока нет

- DB Link CreationДокумент4 страницыDB Link CreationRamesh GurumoorthyОценок пока нет

- IV BTech I Semester CAD/CAM Exam QuestionsДокумент4 страницыIV BTech I Semester CAD/CAM Exam QuestionsMD KHALEELОценок пока нет

- Software Piracy Prevention: TheftДокумент11 страницSoftware Piracy Prevention: TheftSreedhara Venkata Ramana KumarОценок пока нет

- CS506 Solved Subjective Questions on Web DesignДокумент28 страницCS506 Solved Subjective Questions on Web DesignIqraОценок пока нет

- FLEXnet ID Dongle DriversДокумент24 страницыFLEXnet ID Dongle DriversAnonymous 44EspfОценок пока нет

- Cryptex TutДокумент15 страницCryptex Tutaditya7398Оценок пока нет

- Advanced Database Management SystemДокумент6 страницAdvanced Database Management SystemTanushree ShenviОценок пока нет

- Olympic Message System Usability: Early Testing Reveals 57 IssuesДокумент16 страницOlympic Message System Usability: Early Testing Reveals 57 Issuestrevor randyОценок пока нет

- Verifying The Iu-PS Interface: About This ChapterДокумент8 страницVerifying The Iu-PS Interface: About This ChapterMohsenОценок пока нет

- Arcgis For Desktop: Powerful ApplicationsДокумент3 страницыArcgis For Desktop: Powerful Applicationskarthikp207Оценок пока нет

- XML Unit 2 NotesДокумент24 страницыXML Unit 2 NotesJai SharmaОценок пока нет

- In Touch ArchestrAДокумент84 страницыIn Touch ArchestrAItalo MontecinosОценок пока нет

- EDSA Installation GuideДокумент49 страницEDSA Installation GuideKabau SirahОценок пока нет

- Ministry of Education Database System. by - Abdirashid JeeniДокумент82 страницыMinistry of Education Database System. by - Abdirashid JeeniAbdirashid JeeniОценок пока нет

- Price Ice BoxДокумент2 страницыPrice Ice BoxHaffiz AtingОценок пока нет

- MIT6 0002F16 ProblemSet5Документ13 страницMIT6 0002F16 ProblemSet5DevendraReddyPoreddyОценок пока нет

- IT 160 Final Lab Project - Chad Brown (VM37)Документ16 страницIT 160 Final Lab Project - Chad Brown (VM37)Chad BrownОценок пока нет

- Garmin Swim: Owner's ManualДокумент12 страницGarmin Swim: Owner's ManualCiureanu CristianОценок пока нет

- YouTube Brand Channel RedesignДокумент60 страницYouTube Brand Channel Redesignchuck_nottisОценок пока нет

- Health Informatics Course Overview and Learning ObjectivesДокумент4 страницыHealth Informatics Course Overview and Learning ObjectivesYhaz VillaОценок пока нет

- GUI Payroll SystemДокумент4 страницыGUI Payroll Systemfeezy1Оценок пока нет