Вам также может понравиться

- Liberalisation of Insurance Services RefinedДокумент22 страницыLiberalisation of Insurance Services RefinedJojin JoseОценок пока нет

- Comparative study of public & private life insurersДокумент9 страницComparative study of public & private life insurersAamir Sohail KurashiОценок пока нет

- Historical Development of InsuranceДокумент5 страницHistorical Development of InsuranceFbarrsОценок пока нет

- INSURANCE LAW IN INDIAДокумент44 страницыINSURANCE LAW IN INDIAVaibhav AhujaОценок пока нет

- History of Life Insurance in IndiaДокумент4 страницыHistory of Life Insurance in IndiaGanesh DadgeОценок пока нет

- Law of InsuranceДокумент7 страницLaw of InsuranceJack Dowson100% (1)

- Study on LIC and Insurance Sector in IndiaДокумент43 страницыStudy on LIC and Insurance Sector in Indiajugnu_dubeyОценок пока нет

- Insurance ProjДокумент20 страницInsurance ProjMahesh ParabОценок пока нет

- Reliance Life Insurance ReportДокумент116 страницReliance Life Insurance ReportTimothy Brown100% (1)

- Life Insurance Progress in India Since 2000Документ15 страницLife Insurance Progress in India Since 2000Abhishek VanigothaОценок пока нет

- How Actuaries Help Plan for an Uncertain FutureДокумент12 страницHow Actuaries Help Plan for an Uncertain FuturePrajakta Kadam67% (3)

- IRDA and Insurance Administration in IndiaДокумент18 страницIRDA and Insurance Administration in IndiaSneha SharmaОценок пока нет

- Chapter #5 Fire Insurance: Key ConceptsДокумент17 страницChapter #5 Fire Insurance: Key ConceptsOptimistic EyeОценок пока нет

- Motor InsuranceДокумент35 страницMotor InsuranceS1626Оценок пока нет

- Brief History of InsuranceДокумент9 страницBrief History of InsuranceVijay100% (1)

- Oriental InsuranceДокумент24 страницыOriental InsuranceSumit BorichaОценок пока нет

- Chapter 1-What Is Insurance?Документ20 страницChapter 1-What Is Insurance?Akshada Chitnis100% (2)

- Claim Management Life Insurance - DocsДокумент3 страницыClaim Management Life Insurance - DocsShubham NamdevОценок пока нет

- HDFC LifeДокумент66 страницHDFC LifeChetan PahwaОценок пока нет

- Contribution of Insurance IndustryДокумент32 страницыContribution of Insurance IndustrysayedhossainОценок пока нет

- CHANGES IN INSURANCE SECTOR (A Study On Public Awareness)Документ47 страницCHANGES IN INSURANCE SECTOR (A Study On Public Awareness)Ramaduta80% (5)

- Lic Final ReportДокумент109 страницLic Final ReportAbhisek BanerjeeОценок пока нет

- Types of NBFCДокумент16 страницTypes of NBFCathiraОценок пока нет

- Accident InsuranceДокумент26 страницAccident InsuranceNandini JaganОценок пока нет

- Central University of South Bihar School of Law& GovernanceДокумент4 страницыCentral University of South Bihar School of Law& GovernanceKumar KishanОценок пока нет

- InsuranceДокумент215 страницInsuranceAastha MishraОценок пока нет

- B Law Winding Up and Dissolution of A CompanyДокумент14 страницB Law Winding Up and Dissolution of A Companyakhtar03100% (1)

- Issues and Challenges of Insurance Industry in IndiaДокумент3 страницыIssues and Challenges of Insurance Industry in Indianishant b100% (1)

- SBI Life InsuranceДокумент41 страницаSBI Life InsuranceSandeep Mauriya0% (1)

- Fdi in InsuranceДокумент8 страницFdi in InsuranceSanthosh KumarОценок пока нет

- Literature Review on Insurance Management AutomationДокумент5 страницLiterature Review on Insurance Management AutomationAncy KalungaОценок пока нет

- Development of Insurance Law in IndiaДокумент2 страницыDevelopment of Insurance Law in Indiashakti ranjan mohantyОценок пока нет

- Report On BhartiДокумент57 страницReport On BhartiWendy CannonОценок пока нет

- A Study On Insurance (Life Insurance Corporation) : DeclarationДокумент42 страницыA Study On Insurance (Life Insurance Corporation) : DeclarationMonil ChhedaОценок пока нет

- Micro Insurance 2Документ61 страницаMicro Insurance 2salmaОценок пока нет

- Finacial Performance of Life InsuracneДокумент24 страницыFinacial Performance of Life InsuracneCryptic LollОценок пока нет

- IC33 Revised Edition EnglishДокумент513 страницIC33 Revised Edition Englishhdsk82Оценок пока нет

- Insurance, Negotiable Instruments and Banking Assignment: "Insurable Interest"Документ19 страницInsurance, Negotiable Instruments and Banking Assignment: "Insurable Interest"OwaisWarsiОценок пока нет

- Insurance ProjectДокумент9 страницInsurance ProjectVineeth ReddyОценок пока нет

- Insurance Notes: Life InsuranceДокумент18 страницInsurance Notes: Life InsuranceJinuro SanОценок пока нет

- Chapter - 1 Introduction To Insurance in India: Vivek College of CommerceДокумент69 страницChapter - 1 Introduction To Insurance in India: Vivek College of CommerceRutu_Ko_7037Оценок пока нет

- Social SecurityДокумент4 страницыSocial SecurityRajaDurai RamakrishnanОценок пока нет

- Legal Aspects of Indian BusinessДокумент124 страницыLegal Aspects of Indian BusinessGuruKPO100% (3)

- A Study on Awareness Towards Life InsuranceДокумент94 страницыA Study on Awareness Towards Life InsurancekanujkohliОценок пока нет

- Royal Sundaram General InsuranceДокумент22 страницыRoyal Sundaram General InsuranceVinayak BhardwajОценок пока нет

- Crop Insurance Crop Insurance in IndiaДокумент11 страницCrop Insurance Crop Insurance in IndiaprabhuОценок пока нет

- Banking and Insurance ElementsДокумент11 страницBanking and Insurance ElementsNisarg ShahОценок пока нет

- IRDA - Insurance RegulatorДокумент52 страницыIRDA - Insurance RegulatorShubham PatilОценок пока нет

- Insurance Ombudsman Explained: Key Roles and ResponsibilitiesДокумент25 страницInsurance Ombudsman Explained: Key Roles and ResponsibilitiesParameshwar Bhat NОценок пока нет

- Research On Life InsuranceДокумент90 страницResearch On Life InsuranceDhananjay SharmaОценок пока нет

- MINOR PROJECT On InsuranceДокумент53 страницыMINOR PROJECT On InsurancedivyaОценок пока нет

- Claim Settlement of GICДокумент51 страницаClaim Settlement of GICSusilPandaОценок пока нет

- A Study of Fire Insurance With Refernce To Bajaj Allianz General InsuranceДокумент90 страницA Study of Fire Insurance With Refernce To Bajaj Allianz General InsuranceshreyaОценок пока нет

- Life Insurance: AN Assignment OnДокумент40 страницLife Insurance: AN Assignment OnAmar AhirwarОценок пока нет

- Higher standards in insurance make a differenceДокумент18 страницHigher standards in insurance make a differencechintamani1992Оценок пока нет

- Aviation INSURANCE FinalДокумент53 страницыAviation INSURANCE FinalHarish AgarwalОценок пока нет

- History of Insurance in IndiaДокумент2 страницыHistory of Insurance in Indianavigatorsoluti7331Оценок пока нет

- Life InsuranceДокумент39 страницLife Insurancearjunmba11962450% (2)

- Insurance Act 1938 IIBSДокумент23 страницыInsurance Act 1938 IIBSbapparoyОценок пока нет

- RFP - Visa OutsourcingДокумент12 страницRFP - Visa OutsourcingromsbhojakОценок пока нет

- WR CSP 21 NameList Engl 021121Документ325 страницWR CSP 21 NameList Engl 021121Mohd BilalОценок пока нет

- USA V Baladian Nov 29, 2021 Protective Order Re DiscoveryДокумент6 страницUSA V Baladian Nov 29, 2021 Protective Order Re DiscoveryFile 411Оценок пока нет

- All Forms by Atty TeДокумент77 страницAll Forms by Atty TeJep Acido100% (1)

- Umil v. Ramos PDFДокумент3 страницыUmil v. Ramos PDFKJPL_1987Оценок пока нет

- Vasai Housing Federation AppendicesДокумент6 страницVasai Housing Federation AppendicesPrasadОценок пока нет

- Lawyers Oath PDFДокумент5 страницLawyers Oath PDFMegan ManahanОценок пока нет

- Omnibus Rules On Leave: Rule Xvi of The Omnibus Rules Implementing Book V of Eo 292Документ2 страницыOmnibus Rules On Leave: Rule Xvi of The Omnibus Rules Implementing Book V of Eo 292Miguel GonzalesОценок пока нет

- Letter 2Документ2 страницыLetter 2Scott AsherОценок пока нет

- Unit 1 IntroductionДокумент17 страницUnit 1 Introductionanne leeОценок пока нет

- Vakalatnama Supreme CourtДокумент2 страницыVakalatnama Supreme CourtSiddharth Chitturi80% (5)

- AutoPay Output Documents PDFДокумент2 страницыAutoPay Output Documents PDFAnonymous QZuBG2IzsОценок пока нет

- JOSE C. SABERON v. ATTY. FERNANDO T. LARONGДокумент4 страницыJOSE C. SABERON v. ATTY. FERNANDO T. LARONGshienna baccayОценок пока нет

- Murder Conviction UpheldДокумент9 страницMurder Conviction UpheldBobОценок пока нет

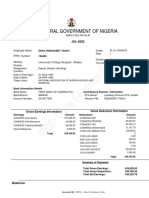

- Federal Pay Slip for Margaret Taiwo GiwaДокумент1 страницаFederal Pay Slip for Margaret Taiwo GiwaHalleluyah HalleluyahОценок пока нет

- Validation Proof of ClaimДокумент4 страницыValidation Proof of Claimroyalarch13100% (5)

- Law of Agency - Summary NotesДокумент8 страницLaw of Agency - Summary NotesWycliffe Ogetii91% (32)

- Appeal To High Court Under Code of Civil ProcedureДокумент2 страницыAppeal To High Court Under Code of Civil ProcedureShelly SachdevОценок пока нет

- Module 5 D Obligations With A Penal ClauseДокумент3 страницыModule 5 D Obligations With A Penal Clauseairam cabadduОценок пока нет

- Strict LiabilityДокумент11 страницStrict LiabilityMWAKISIKI MWAKISIKI EDWARDSОценок пока нет

- CHAPTER ONE: Statutes in General Enactment of Statutes: Jural and Generic Jural and ConcreteДокумент84 страницыCHAPTER ONE: Statutes in General Enactment of Statutes: Jural and Generic Jural and Concretenigel alinsugОценок пока нет

- Jobad 123541Документ1 страницаJobad 123541faheem ahmedОценок пока нет

- TortДокумент11 страницTortHarshVardhanОценок пока нет

- Q. Write A Short Note On FIR. Discuss The Guidelines Laid Down by The Supreme Court For Mandatory Registration of FIR in Lalita Kumari's CaseДокумент3 страницыQ. Write A Short Note On FIR. Discuss The Guidelines Laid Down by The Supreme Court For Mandatory Registration of FIR in Lalita Kumari's CaseshareenОценок пока нет

- CLAVERIA ActДокумент6 страницCLAVERIA ActCharles Aloba DalogdogОценок пока нет

- Contract Formation Issues in Betty and Albert's Car Sale NegotiationsДокумент2 страницыContract Formation Issues in Betty and Albert's Car Sale NegotiationsRajesh NagarajanОценок пока нет

- The Hidden History of The Second AmendmentДокумент96 страницThe Hidden History of The Second AmendmentAsanij100% (1)

- Nielson v. LepantoДокумент2 страницыNielson v. LepantoHazel P.Оценок пока нет

- Comfort Women Seek Official Apology from JapanДокумент4 страницыComfort Women Seek Official Apology from JapanCistron ExonОценок пока нет

- 50 Apo Fruits Corp V Land Bank of The PhilippinesДокумент5 страниц50 Apo Fruits Corp V Land Bank of The PhilippinesRae Angela GarciaОценок пока нет