Вам также может понравиться

- Howard Marks Letters: Risk Revisited AgainДокумент21 страницаHoward Marks Letters: Risk Revisited AgainKyithОценок пока нет

- Howard Marks - Getting LuckyДокумент13 страницHoward Marks - Getting LuckyZerohedgeОценок пока нет

- Factsheet Singapore Savings BondsДокумент2 страницыFactsheet Singapore Savings BondsKyithОценок пока нет

- China Merchant Pacific - DBS VickersДокумент9 страницChina Merchant Pacific - DBS VickersKyithОценок пока нет

- Openworld Listed Infra Update Jan2012Документ4 страницыOpenworld Listed Infra Update Jan2012KyithОценок пока нет

- John Bogle - The Arithmetic of All in Investment ExpensesДокумент9 страницJohn Bogle - The Arithmetic of All in Investment ExpensesKyithОценок пока нет

- Far East Hospitality Trust (D) - CIMBДокумент17 страницFar East Hospitality Trust (D) - CIMBKyithОценок пока нет

- Means, Ends and Dividends in A New World of Lower Yields and Longer LivesДокумент16 страницMeans, Ends and Dividends in A New World of Lower Yields and Longer LivesKyithОценок пока нет

- Grantham Quarterly Dec 2011Документ4 страницыGrantham Quarterly Dec 2011careyescapitalОценок пока нет

- CMPacific - DBS VickersДокумент7 страницCMPacific - DBS VickersKyithОценок пока нет

- Notes To Margin of SafetyДокумент19 страницNotes To Margin of SafetyTshi21100% (10)

- Accenture Achieving High Performance in The Postal Industry v2Документ24 страницыAccenture Achieving High Performance in The Postal Industry v2KyithОценок пока нет

- China Merchant Pacific - CIMBДокумент19 страницChina Merchant Pacific - CIMBKyithОценок пока нет

- MIIF - DBS VickersДокумент11 страницMIIF - DBS VickersKyithОценок пока нет

- Boustead Invests in Manganese Miner and Develop Indo Coal-Mining FacilitiesДокумент7 страницBoustead Invests in Manganese Miner and Develop Indo Coal-Mining FacilitiesKyithОценок пока нет

- China Merchant Pacific 2011 Sep 13 VickersДокумент13 страницChina Merchant Pacific 2011 Sep 13 VickersKyithОценок пока нет

- Singtel - DBS VickersДокумент3 страницыSingtel - DBS VickersKyithОценок пока нет

- The Pros and Cons of Rights Issues in ReitsДокумент6 страницThe Pros and Cons of Rights Issues in ReitsKyithОценок пока нет

- Telecommunications DBSVДокумент14 страницTelecommunications DBSVKyithОценок пока нет

- Jeff Foster, The Buffett of BasketballДокумент6 страницJeff Foster, The Buffett of BasketballKyithОценок пока нет

- MIIF - DBS VickersДокумент40 страницMIIF - DBS VickersKyithОценок пока нет

- 2011 Jul 08 - IIFL - SingtelДокумент37 страниц2011 Jul 08 - IIFL - SingtelKyithОценок пока нет

- Sabana by Daiwa 15 August 2011Документ5 страницSabana by Daiwa 15 August 2011KyithОценок пока нет

- First Reit - SiasДокумент13 страницFirst Reit - SiasKyithОценок пока нет

- Singapore TelecomДокумент19 страницSingapore TelecomKyithОценок пока нет

- Pec 110804 OirДокумент15 страницPec 110804 OirKyithОценок пока нет

- Philip - SabanaДокумент33 страницыPhilip - SabanaKyithОценок пока нет

- 2011 Jun 24 - DBS - Keppel T&TДокумент15 страниц2011 Jun 24 - DBS - Keppel T&TKyithОценок пока нет

- Telecommunications: Telecommunications: Paradigm Shifts With Cloud ComputingДокумент64 страницыTelecommunications: Telecommunications: Paradigm Shifts With Cloud ComputingKyithОценок пока нет

- Hutchison Port Holdings Trust 300511 DBSVДокумент8 страницHutchison Port Holdings Trust 300511 DBSVKyithОценок пока нет

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (265)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (119)

- Asset Liability Management in BanksДокумент8 страницAsset Liability Management in Bankskpved92Оценок пока нет

- Draft Constitution of Made Men WorldwideДокумент11 страницDraft Constitution of Made Men WorldwidebrightОценок пока нет

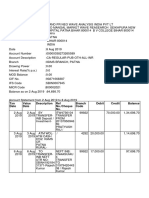

- TXN Date Value Date Description Ref No./Cheque No. Branch Code Debit Credit BalanceДокумент3 страницыTXN Date Value Date Description Ref No./Cheque No. Branch Code Debit Credit BalanceNishi GuptaОценок пока нет

- Present CEO of NCDEX Is ... ?: General AwarenessДокумент1 страницаPresent CEO of NCDEX Is ... ?: General Awarenesssateesh888Оценок пока нет

- PDF Pub Misc NontradhousingBR PDFДокумент28 страницPDF Pub Misc NontradhousingBR PDFkj55Оценок пока нет

- Accounting For Intercompany Transactions - FinalДокумент15 страницAccounting For Intercompany Transactions - FinalEunice WongОценок пока нет

- The Sunday Times - UBS Global Warming Index - Ilija Murisic - May 07Документ2 страницыThe Sunday Times - UBS Global Warming Index - Ilija Murisic - May 07akasaka99Оценок пока нет

- FinalsДокумент11 страницFinalsTong KennedyОценок пока нет

- Valuation Workbook QuestionsДокумент200 страницValuation Workbook QuestionsAugusto César0% (1)

- Error Correction (Part 2) - Suspense Accounts (Including RQS)Документ6 страницError Correction (Part 2) - Suspense Accounts (Including RQS)King JulianОценок пока нет

- Assessment Paper and Instructions To Candidates:: FM320 - Quantitative Finance Suitable For All CandidatesДокумент5 страницAssessment Paper and Instructions To Candidates:: FM320 - Quantitative Finance Suitable For All CandidatesYingzhi XuОценок пока нет

- Case Study ALSA Contract Negotiation Workshop - Local PartnerДокумент2 страницыCase Study ALSA Contract Negotiation Workshop - Local PartnerAMSОценок пока нет

- TVM Spring 2015Документ2 страницыTVM Spring 2015Kamran RaufОценок пока нет

- Proclamation of Sale: Motor VehiclesДокумент12 страницProclamation of Sale: Motor VehiclesJCMARRIE YUSOFОценок пока нет

- Heller, Jack, CPCUMARPДокумент4 страницыHeller, Jack, CPCUMARPTexas WatchdogОценок пока нет

- Maybank Moratorium FAQsДокумент7 страницMaybank Moratorium FAQsمحمدتوفيقОценок пока нет

- Working Capital Management AbstractДокумент14 страницWorking Capital Management AbstractPriyanka GuptaОценок пока нет

- Construction and Projects in Indonesia OverviewДокумент31 страницаConstruction and Projects in Indonesia OverviewDaniel LubisОценок пока нет

- Strategic Management GuideДокумент64 страницыStrategic Management GuideAlbert Ziwome0% (1)

- Civil Law Uribe Notes Civ Rev 2Документ74 страницыCivil Law Uribe Notes Civ Rev 2Chilzia RojasОценок пока нет

- Bank ReconciliationДокумент2 страницыBank ReconciliationPatrick BacongalloОценок пока нет

- NON Negotiable Unlimited Private BondДокумент2 страницыNON Negotiable Unlimited Private Bonddbush277886% (14)

- IB Chapter08Документ52 страницыIB Chapter08ismat arteeОценок пока нет

- Cash in Bank Register: Appendix 37Документ2 страницыCash in Bank Register: Appendix 37Lani LacarrozaОценок пока нет

- Final HBL PresentationДокумент75 страницFinal HBL PresentationShehzaib Sunny100% (4)

- ProjectДокумент79 страницProjectvishwajit bhoir100% (1)

- COM203 AmalgamationДокумент10 страницCOM203 AmalgamationLogeshОценок пока нет

- Civ Pro Q&AДокумент7 страницCiv Pro Q&ASGTОценок пока нет

- Accounting As The Language of BusinessДокумент2 страницыAccounting As The Language of BusinessjuliahuiniОценок пока нет