Вам также может понравиться

- 06 Short Term Financing ManagementДокумент8 страниц06 Short Term Financing ManagementLee TeukОценок пока нет

- fINAL PPT REPORTING-SPECIAL TOPICSДокумент26 страницfINAL PPT REPORTING-SPECIAL TOPICSFelicity Joy CruelОценок пока нет

- Sources of Finance - CreditДокумент12 страницSources of Finance - CreditSanta PinkaОценок пока нет

- Short Term FinancingДокумент12 страницShort Term FinancingNischal Jung0% (1)

- Business Finance PPT - 12 Short Term Sources of FinancingДокумент25 страницBusiness Finance PPT - 12 Short Term Sources of FinancingELMSS100% (1)

- Current Liabilities Management SOLUTIONSДокумент9 страницCurrent Liabilities Management SOLUTIONSJack Herer100% (1)

- CL ExercisesДокумент13 страницCL ExercisesJas AlbosОценок пока нет

- G7 Fund ManagementДокумент43 страницыG7 Fund ManagementKim Andrea TupasОценок пока нет

- Short Terrm Financing FinalДокумент21 страницаShort Terrm Financing FinalAtika Gando SuriОценок пока нет

- Chapter 13Документ39 страницChapter 13Marwa HassanОценок пока нет

- Busfin 7 Sources and Uses of Short Term and Long Term FundsДокумент5 страницBusfin 7 Sources and Uses of Short Term and Long Term FundsRenz Abad50% (2)

- Working Capital Management (GROUP 5)Документ33 страницыWorking Capital Management (GROUP 5)Cyrylle AngelesОценок пока нет

- FINANCE MANAGEMENT FIN420 CHP 7Документ28 страницFINANCE MANAGEMENT FIN420 CHP 7Yanty Ibrahim100% (3)

- Chapter 4 - Sources and Uses of FundsДокумент17 страницChapter 4 - Sources and Uses of Fundsmarissa casareno almueteОценок пока нет

- Notes in Short Term FinancingДокумент3 страницыNotes in Short Term FinancingLiana Monica LopezОценок пока нет

- Current Liabilities Management: Prepared by Keldon BauerДокумент35 страницCurrent Liabilities Management: Prepared by Keldon BauerMónica GarzaОценок пока нет

- Sources of Short-Term Financing: (Chapter 8) (Chapter 6 - Pages 151 - 155)Документ14 страницSources of Short-Term Financing: (Chapter 8) (Chapter 6 - Pages 151 - 155)Princess AduanaОценок пока нет

- Assignment For BM...Документ9 страницAssignment For BM...Anonymous xOqiXnW9Оценок пока нет

- Chapter 8 - Short Term FinancingДокумент45 страницChapter 8 - Short Term FinancingCindy Jane Omillio100% (1)

- Chapter 12 Senior SecurityДокумент23 страницыChapter 12 Senior SecuritySumonОценок пока нет

- Types of Borrowers-Lending ProcessДокумент39 страницTypes of Borrowers-Lending ProcessEr YogendraОценок пока нет

- Short Term Sources of FinanceДокумент3 страницыShort Term Sources of FinanceRachit AgarwalОценок пока нет

- Short-Term Financing: After Studying This Chapter, You Will Be Able ToДокумент13 страницShort-Term Financing: After Studying This Chapter, You Will Be Able ToMohammad Salim HossainОценок пока нет

- Short Term FinanceДокумент11 страницShort Term Financethisispurva100% (1)

- Sources of Short Term and Long Term FinanceДокумент6 страницSources of Short Term and Long Term FinanceSharath KannanОценок пока нет

- Working Capital Management: BhushanДокумент42 страницыWorking Capital Management: BhushanDrisya NpОценок пока нет

- Sources of FinanceДокумент10 страницSources of FinanceOmer UddinОценок пока нет

- Chapter 6-8 - Sources of Finance & Short Term FinanceДокумент8 страницChapter 6-8 - Sources of Finance & Short Term FinanceTAN YUN YUNОценок пока нет

- Working Capital Management SlidesДокумент25 страницWorking Capital Management SlidesFirdaus LasnangОценок пока нет

- Bank CreditДокумент5 страницBank Creditnhan thanhОценок пока нет

- BBA2030493Документ14 страницBBA2030493Saad AhmedОценок пока нет

- Sources and Uses of Short-Term and Long - Term FundsДокумент20 страницSources and Uses of Short-Term and Long - Term FundsMichelle RotairoОценок пока нет

- FM Chapter 14Документ6 страницFM Chapter 14Ma. Christina ErminoОценок пока нет

- FM Lecture 9Документ28 страницFM Lecture 9Awan NadiaОценок пока нет

- Credit PlanningДокумент9 страницCredit PlanningMonika Saini100% (1)

- Finance Module 05 - Week 5Документ8 страницFinance Module 05 - Week 5Christian ZebuaОценок пока нет

- Working Capital Working Capital (Accounting Terms) Liquidity LiquidationДокумент6 страницWorking Capital Working Capital (Accounting Terms) Liquidity LiquidationRömëla BröçëОценок пока нет

- Mancon ActivityДокумент3 страницыMancon Activityjane B0% (1)

- Lecture 09Документ17 страницLecture 09simraОценок пока нет

- Consumer CreditДокумент57 страницConsumer Creditmanik_mittal3Оценок пока нет

- WC - Merits and DemeritsДокумент23 страницыWC - Merits and DemeritsARUN100% (1)

- FINMNN1 Chapter 4 Short Term Financial PlanningДокумент16 страницFINMNN1 Chapter 4 Short Term Financial Planningkissmoon732Оценок пока нет

- Chapter 7. Sources of FinanceДокумент20 страницChapter 7. Sources of FinanceHastings KapalaОценок пока нет

- 5 Consumer Financ-2Документ13 страниц5 Consumer Financ-2thullimilli leelaprasadОценок пока нет

- Chapter FiveДокумент7 страницChapter FiveChala tursaОценок пока нет

- Finance ExamДокумент9 страницFinance ExamTEOH WEN QIОценок пока нет

- FinmanДокумент3 страницыFinmanKaren LaccayОценок пока нет

- Business Finance M3Документ6 страницBusiness Finance M3Katrina LuzungОценок пока нет

- Commercial and Industrial LoansДокумент36 страницCommercial and Industrial LoansAngela ChuaОценок пока нет

- MCQ Working Capital Management CPAR 1 84Документ18 страницMCQ Working Capital Management CPAR 1 84PiaElemos85% (13)

- Module - 7 Working Capital Management and Financing: Meaning, Importance, Concepts ofДокумент5 страницModule - 7 Working Capital Management and Financing: Meaning, Importance, Concepts ofPintoo Kumar GuptaОценок пока нет

- Short Term FinancingДокумент16 страницShort Term FinancingDinesh RamrakhyaniОценок пока нет

- 9new - 471233 - Learning Material - SMEДокумент28 страниц9new - 471233 - Learning Material - SMERavi KumarОценок пока нет

- Short Term FinancingДокумент16 страницShort Term FinancingSaha SuprioОценок пока нет

- Raising Funds Through EquityДокумент20 страницRaising Funds Through Equityapi-3705920Оценок пока нет

- Working Capital ManagementДокумент30 страницWorking Capital ManagementEvangelineОценок пока нет

- CH5 FinancingДокумент2 страницыCH5 FinancingSamir SubediОценок пока нет

- Approved: How to Get Your Business Loan Funded Faster, Cheaper, & with Less StressОт EverandApproved: How to Get Your Business Loan Funded Faster, Cheaper, & with Less StressРейтинг: 5 из 5 звезд5/5 (1)

- The Bullwhip Effect in HPs Supply ChainДокумент9 страницThe Bullwhip Effect in HPs Supply Chainsoulhudson100% (1)

- Food Safety and Hygiene LayoutДокумент9 страницFood Safety and Hygiene LayoutJann Kerky100% (1)

- KFC CaseДокумент2 страницыKFC CaseJann KerkyОценок пока нет

- SFPC Operational Definition InstructionsДокумент2 страницыSFPC Operational Definition InstructionsJann KerkyОценок пока нет

- Precision Delivery Inc. Case StudyДокумент2 страницыPrecision Delivery Inc. Case StudyJann Kerky0% (1)

- Guidelines of Martial LawДокумент16 страницGuidelines of Martial LawJann KerkyОценок пока нет

- EbitДокумент3 страницыEbitJann KerkyОценок пока нет

- Horizontal and Vertical Analysis DetailsДокумент9 страницHorizontal and Vertical Analysis DetailsJann KerkyОценок пока нет

- 10 AxiomsДокумент6 страниц10 AxiomsJann KerkyОценок пока нет

- Cash BudgetДокумент3 страницыCash BudgetJann Kerky0% (1)

- Analysis of Financial StatementsДокумент20 страницAnalysis of Financial StatementsJann KerkyОценок пока нет

- Chapter 2: Atomic Structure & Interatomic Bonding: Issues To Address..Документ36 страницChapter 2: Atomic Structure & Interatomic Bonding: Issues To Address..putriyusairah_91Оценок пока нет

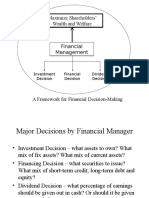

- Maximize Shareholders' Wealth and Welfare: Investment Decision Financial Decision Dividend DecisionДокумент6 страницMaximize Shareholders' Wealth and Welfare: Investment Decision Financial Decision Dividend DecisionJann KerkyОценок пока нет

- The Tragic MythДокумент4 страницыThe Tragic MythJann KerkyОценок пока нет

- The GoalДокумент3 страницыThe GoalJann KerkyОценок пока нет

- Analysis of Financial Statements: Answers To End-Of-Chapter QuestionsДокумент15 страницAnalysis of Financial Statements: Answers To End-Of-Chapter QuestionsAditya R HimawanОценок пока нет

- Energy TransformationДокумент6 страницEnergy TransformationJann KerkyОценок пока нет

- Sample FinalДокумент9 страницSample FinalJann KerkyОценок пока нет

- Chapter 2: Atomic Structure & Interatomic Bonding: Issues To Address..Документ36 страницChapter 2: Atomic Structure & Interatomic Bonding: Issues To Address..putriyusairah_91Оценок пока нет

- Telfer - Food As ArtДокумент10 страницTelfer - Food As ArtJann Kerky100% (1)

- Problems and SolutionsДокумент31 страницаProblems and SolutionsJann KerkyОценок пока нет

- Accord 2013 BrochureДокумент25 страницAccord 2013 BrochureJann KerkyОценок пока нет

- July 8 Pages - Gowrie NewsДокумент16 страницJuly 8 Pages - Gowrie NewsTonya HarrisonОценок пока нет

- Accounting ExamsДокумент56 страницAccounting Examsjhie boterОценок пока нет

- Peer Review Report Phase 1 AndorraДокумент75 страницPeer Review Report Phase 1 AndorraOECD: Organisation for Economic Co-operation and DevelopmentОценок пока нет

- CimbДокумент36 страницCimba1an_wongОценок пока нет

- Assignment On Dhaka Bank LimitedДокумент23 страницыAssignment On Dhaka Bank LimitedMd Wasiq DayemОценок пока нет

- Sanction LetterДокумент7 страницSanction LetterPrimon KarmakarОценок пока нет

- Industry Report - Payment GatewaysДокумент12 страницIndustry Report - Payment Gatewayskunal KatariaОценок пока нет

- Kotak Mahindra Bank Q3 FY20 Earnings Conference Call: January 20, 2020Документ18 страницKotak Mahindra Bank Q3 FY20 Earnings Conference Call: January 20, 2020divya mОценок пока нет

- Class 2Документ87 страницClass 2tipsyturtleОценок пока нет

- AML& KYC QuestionsДокумент93 страницыAML& KYC QuestionsNiranjan ReddyОценок пока нет

- CBO Attachement (1) - 1-1Документ18 страницCBO Attachement (1) - 1-1Gemechis cherinet BedadaОценок пока нет

- Financial Institution and MarketДокумент52 страницыFinancial Institution and Marketsabit hussenОценок пока нет

- Myanmar's Financial Sector A Challenging Environment For Banks ( (3 RD Edition, 2016)Документ96 страницMyanmar's Financial Sector A Challenging Environment For Banks ( (3 RD Edition, 2016)THAN HANОценок пока нет

- 0167XXXXXXXXX841702 08 2019 PDFДокумент3 страницы0167XXXXXXXXX841702 08 2019 PDFKirti SharmaОценок пока нет

- What Is Personal Loan?: Personal Loans (Growth in Last 5 Financial Years)Документ16 страницWhat Is Personal Loan?: Personal Loans (Growth in Last 5 Financial Years)Apurva JawadeОценок пока нет

- C. People's Reaction About Liquidated BanksДокумент3 страницыC. People's Reaction About Liquidated BanksGiovanno Macario PОценок пока нет

- Hindu Undivided Family Letter Super User 4.5Документ3 страницыHindu Undivided Family Letter Super User 4.5ratnesh vaviaОценок пока нет

- BrazilДокумент16 страницBrazilSaulo FernandesОценок пока нет

- Banas Vs Asia Pacific NILДокумент2 страницыBanas Vs Asia Pacific NILBeverlyn JamisonОценок пока нет

- Market Wizard Newsletter Issue 66 - Sip BasketДокумент81 страницаMarket Wizard Newsletter Issue 66 - Sip Basketsudheera cОценок пока нет

- Indian Financial SystemДокумент2 страницыIndian Financial SystemAkash PawarОценок пока нет

- Meaning of E-Banking: 3.2 Automated Teller MachineДокумент16 страницMeaning of E-Banking: 3.2 Automated Teller Machinehuneet SinghОценок пока нет

- Bouncing Check LawДокумент18 страницBouncing Check LawMichael Ang SauzaОценок пока нет

- Trading Stocks: QES Group Eversafe RubberДокумент5 страницTrading Stocks: QES Group Eversafe RubberAmir HasridzОценок пока нет

- As Per Nepal Rastra BankДокумент2 страницыAs Per Nepal Rastra BankMandil BhandariОценок пока нет

- Banking Mangement SystemДокумент10 страницBanking Mangement SystemFirew KifleОценок пока нет

- RFBT - Chapter 5 - Philippine Deposit Insurance CorporationДокумент6 страницRFBT - Chapter 5 - Philippine Deposit Insurance Corporationlaythejoylunas21Оценок пока нет

- Delaware Administrative Code Banking 2205Документ2 страницыDelaware Administrative Code Banking 2205tarun.mitra19854923Оценок пока нет

- Fair MoneyДокумент223 страницыFair MoneyCoy HopperОценок пока нет

- Untuk Interview XenditДокумент5 страницUntuk Interview XenditDinda BazliahОценок пока нет