Вам также может понравиться

- rp5301fs Prop Tax Facts PDFДокумент2 страницыrp5301fs Prop Tax Facts PDFjspectorОценок пока нет

- Tax Freeze Guidance DocumentДокумент20 страницTax Freeze Guidance DocumentjspectorОценок пока нет

- 2012 Tax Rate ReportДокумент88 страниц2012 Tax Rate ReportZoe GallandОценок пока нет

- 16 Don'T-Miss Tax DeductionsДокумент4 страницы16 Don'T-Miss Tax DeductionsGon FloОценок пока нет

- NY COVID Rent ReliefДокумент2 страницыNY COVID Rent ReliefJoe SpectorОценок пока нет

- Intrim Union Budget 2019-20Документ12 страницIntrim Union Budget 2019-20Rukmani GuptaОценок пока нет

- Pro Mortgage Interest Tax Deduction: Ashley Sadighpour, Charlene Shi, Jeremy Sauvage, Nick Segal, & Matt WagonhurstДокумент8 страницPro Mortgage Interest Tax Deduction: Ashley Sadighpour, Charlene Shi, Jeremy Sauvage, Nick Segal, & Matt WagonhurstJiayu JinОценок пока нет

- County Administrator 2017 Budget MemoДокумент20 страницCounty Administrator 2017 Budget MemoFauquier NowОценок пока нет

- Forbes 2018 Tax GuideДокумент16 страницForbes 2018 Tax GuideJerry WhittonОценок пока нет

- Tax Update 2009Документ2 страницыTax Update 2009calebwoodsОценок пока нет

- 2011 Tax Reference GuideДокумент11 страниц2011 Tax Reference GuideSaver PlusОценок пока нет

- Revenue Sharing ReportДокумент12 страницRevenue Sharing ReportMaine Policy InstituteОценок пока нет

- Session 23-25 Permissible Deduction From Gross Total IncomeДокумент14 страницSession 23-25 Permissible Deduction From Gross Total Incomeomar zohorianОценок пока нет

- House PropertyДокумент19 страницHouse PropertyChandraОценок пока нет

- Income Tax ReturnДокумент57 страницIncome Tax ReturnMalik WasimОценок пока нет

- Taxes and InsuranceДокумент14 страницTaxes and InsuranceAbdullah RamzanОценок пока нет

- 2023 Proposed Fauquier Budget SummaryДокумент24 страницы2023 Proposed Fauquier Budget SummaryFauquier NowОценок пока нет

- Cut Your Clients Tax Bill: Individual Tax Planning Tips and StrategiesОт EverandCut Your Clients Tax Bill: Individual Tax Planning Tips and StrategiesОценок пока нет

- Atlantic City Recovery Plan in Brief 10.24.2016 - FINALДокумент23 страницыAtlantic City Recovery Plan in Brief 10.24.2016 - FINALPress of Atlantic CityОценок пока нет

- A. The Constitution and The Income Tax: Federal Income Tax Professor Morrison Fall 2003 CHAPTER 1: IntroductionДокумент67 страницA. The Constitution and The Income Tax: Federal Income Tax Professor Morrison Fall 2003 CHAPTER 1: IntroductioncjleopОценок пока нет

- Real Estate Recapture TaxДокумент5 страницReal Estate Recapture TaxmpboxeОценок пока нет

- Investment Submission Guidelines For F.Y. 2022-23Документ13 страницInvestment Submission Guidelines For F.Y. 2022-23harikrushnaОценок пока нет

- Joint Tax Hearing-Ron DeutschДокумент18 страницJoint Tax Hearing-Ron DeutschZacharyEJWilliamsОценок пока нет

- Evaluating School Funding ProposalsДокумент8 страницEvaluating School Funding ProposalspublicschoolnotebookОценок пока нет

- CCH Federal Taxation Comprehensive Topics 2013 1st Edition Harmelink Test Bank DownloadДокумент27 страницCCH Federal Taxation Comprehensive Topics 2013 1st Edition Harmelink Test Bank DownloadCecelia Taylor100% (23)

- BTC Reports - Final Tax Plan2013Документ10 страницBTC Reports - Final Tax Plan2013CarolinaMercuryОценок пока нет

- Truth in Taxation: For Taxes Payable in 2021 and Fiscal Year 2021 BudgetДокумент12 страницTruth in Taxation: For Taxes Payable in 2021 and Fiscal Year 2021 BudgetDuluth News TribuneОценок пока нет

- Affordable Housing FAQs 7-28-2014Документ1 страницаAffordable Housing FAQs 7-28-2014Josh YamatОценок пока нет

- Severance and Lump Sum Withholding Tax RatesДокумент1 страницаSeverance and Lump Sum Withholding Tax RatesAnonymous HbOTj4Оценок пока нет

- Home Loan Update 002842 PDFДокумент1 страницаHome Loan Update 002842 PDFShannon SmithОценок пока нет

- Deductions Under Section 80C For Investments in The Indian It Act 1961Документ20 страницDeductions Under Section 80C For Investments in The Indian It Act 1961saurav-maitra-3114Оценок пока нет

- Rebates For First Time BuyersДокумент5 страницRebates For First Time BuyersjohnОценок пока нет

- Budget 2010-11: by Karan Singh, MBA (General) Section - AДокумент32 страницыBudget 2010-11: by Karan Singh, MBA (General) Section - AscherrercuteОценок пока нет

- Comparison Between I.T. and DTCДокумент23 страницыComparison Between I.T. and DTCsharma.shalinee1626Оценок пока нет

- BudgetДокумент21 страницаBudgetshweta_narkhede01Оценок пока нет

- Executive Summary:: Tax Restructuring Policy ProposalДокумент6 страницExecutive Summary:: Tax Restructuring Policy ProposalThe Salt Lake TribuneОценок пока нет

- County Manager's Presentation To Rockingham County Board of Commissioners For 2018/19 Budget.Документ22 страницыCounty Manager's Presentation To Rockingham County Board of Commissioners For 2018/19 Budget.jeffreyhsykesОценок пока нет

- Tax Insight February 2016Документ1 страницаTax Insight February 2016banks305Оценок пока нет

- GOP Tax Bill HighlightsДокумент2 страницыGOP Tax Bill HighlightsWashington Examiner100% (1)

- Taxes: Tax StructureДокумент14 страницTaxes: Tax StructurePradeep NairОценок пока нет

- 2012 Kentucky Individual Income Tax Forms: WWW - Revenue.ky - GovДокумент76 страниц2012 Kentucky Individual Income Tax Forms: WWW - Revenue.ky - GovJason GrohОценок пока нет

- Tax Changes in India and Morocco Taxation CiaДокумент20 страницTax Changes in India and Morocco Taxation CiaMEERA JOSHY 1927436Оценок пока нет

- Tax FinalДокумент21 страницаTax Finalshweta_narkhede01Оценок пока нет

- Livingston County Adopted Budget (2023)Документ401 страницаLivingston County Adopted Budget (2023)Watertown Daily TimesОценок пока нет

- Bank of North Dakota Buydown ProgramДокумент3 страницыBank of North Dakota Buydown ProgramJeremy TurleyОценок пока нет

- VFN Tax and Tax Saving Session 2015Документ27 страницVFN Tax and Tax Saving Session 2015Sumit BawejaОценок пока нет

- Tax and SuperДокумент3 страницыTax and SuperEmmaОценок пока нет

- SUPPORT ActДокумент5 страницSUPPORT ActMary Claire PattonОценок пока нет

- Deductions 3Документ35 страницDeductions 3sanjeev kumar vsОценок пока нет

- FY 16 Analysis of Introduced Budget 102115Документ65 страницFY 16 Analysis of Introduced Budget 102115The Daily LineОценок пока нет

- Maryland Mortgage Program - Recapture TaxДокумент12 страницMaryland Mortgage Program - Recapture TaxNishika JGОценок пока нет

- Quick Notes on “The Trump Tax Cut: Your Personal Guide to the New Tax Law by Eva Rosenberg”От EverandQuick Notes on “The Trump Tax Cut: Your Personal Guide to the New Tax Law by Eva Rosenberg”Оценок пока нет

- Form 1040-ES (NR) : U.S. Estimated Tax For Nonresident Alien IndividualsДокумент9 страницForm 1040-ES (NR) : U.S. Estimated Tax For Nonresident Alien IndividualsBrokerAОценок пока нет

- Income TaxationДокумент12 страницIncome TaxationMonica Jarabelo RamintasОценок пока нет

- Midterm - Theory ReviewДокумент18 страницMidterm - Theory ReviewCameron BelangerОценок пока нет

- Week 3-Local TaxationДокумент23 страницыWeek 3-Local TaxationShanique WilliamsОценок пока нет

- RG146 Pocket GuideДокумент30 страницRG146 Pocket GuideMentor RG146Оценок пока нет

- Understanding Income TaxДокумент31 страницаUnderstanding Income TaxRajesh RoatОценок пока нет

- Surviving the New Tax Landscape: Smart Savings, Investment and Estate Planning StrategiesОт EverandSurviving the New Tax Landscape: Smart Savings, Investment and Estate Planning StrategiesОценок пока нет

- Caregiver Flyer 8.5x11-2019Документ1 страницаCaregiver Flyer 8.5x11-2019Public Information OfficeОценок пока нет

- Cyber Threat Actors Are Impersonating Maryland Government Agencies in Phishing SchemesДокумент2 страницыCyber Threat Actors Are Impersonating Maryland Government Agencies in Phishing SchemesPublic Information OfficeОценок пока нет

- Vital Living NetworkerДокумент34 страницыVital Living NetworkerPublic Information OfficeОценок пока нет

- D3 Lane Closures - 042718Документ8 страницD3 Lane Closures - 042718Public Information OfficeОценок пока нет

- Bike To Work DayДокумент1 страницаBike To Work DayPublic Information OfficeОценок пока нет

- Bethesda Bikeway Popup BTWRoute 05182018 V 4Документ1 страницаBethesda Bikeway Popup BTWRoute 05182018 V 4Public Information OfficeОценок пока нет

- Leggett Announces County Suit Against 14 Opioid CompaniesДокумент163 страницыLeggett Announces County Suit Against 14 Opioid CompaniesPublic Information OfficeОценок пока нет

- Press Release - Topping Off Event - Canopy by Hilton Washington DC Bethesda NorthДокумент4 страницыPress Release - Topping Off Event - Canopy by Hilton Washington DC Bethesda NorthPublic Information OfficeОценок пока нет

- Transportation Options For Older Adults and People With DisabilitiesДокумент2 страницыTransportation Options For Older Adults and People With DisabilitiesPublic Information OfficeОценок пока нет

- 9-2016 Beacon Villages Age FriendlyДокумент2 страницы9-2016 Beacon Villages Age FriendlyPublic Information OfficeОценок пока нет

- 150 Years of Advancement in Educational Equality: Friday, February 24 7Документ1 страница150 Years of Advancement in Educational Equality: Friday, February 24 7Public Information OfficeОценок пока нет

- "Sanctuary Cities" and Community PolicingДокумент3 страницы"Sanctuary Cities" and Community PolicingPublic Information OfficeОценок пока нет

- Celebrate Our OlympiansДокумент1 страницаCelebrate Our OlympiansPublic Information OfficeОценок пока нет

- W-9 FormДокумент2 страницыW-9 FormTrish HitОценок пока нет

- Chapter 6 - Gripping IFRS ICAP 2008 (Solution of Graded Questions)Документ71 страницаChapter 6 - Gripping IFRS ICAP 2008 (Solution of Graded Questions)Falah Ud Din SheryarОценок пока нет

- Aci Card and Merchant Management Solutions Product Line Flyer FL Us 0711 4795 PDFДокумент4 страницыAci Card and Merchant Management Solutions Product Line Flyer FL Us 0711 4795 PDFRazib ZoyОценок пока нет

- PayPal 2Документ9 страницPayPal 2Lucy Marie RamirezОценок пока нет

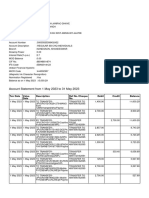

- Account Statement From 1 May 2023 To 31 May 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceДокумент10 страницAccount Statement From 1 May 2023 To 31 May 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit Balanceavinashdeshmukh7027Оценок пока нет

- Transfer PricingДокумент98 страницTransfer PricingMAHESH JAINОценок пока нет

- Taxation: DFA 2104YДокумент16 страницTaxation: DFA 2104YFhawez KodoruthОценок пока нет

- SAP FI NotesДокумент2 страницыSAP FI NotesvinodnagarajuОценок пока нет

- Ujikom PT Cahaya 18-19Документ37 страницUjikom PT Cahaya 18-19Jessyca GunawanОценок пока нет

- CH - 10 Tax Invoice, Credit and Debit Notes Que by ICAIДокумент3 страницыCH - 10 Tax Invoice, Credit and Debit Notes Que by ICAIk kakkarОценок пока нет

- Allama Iqbal Open University: Assignment # 2Документ13 страницAllama Iqbal Open University: Assignment # 2Irfan AslamОценок пока нет

- VerbiageДокумент5 страницVerbiageTuan Ku Rao100% (1)

- Tax Digest (Siao Tiao Hong V Cir)Документ2 страницыTax Digest (Siao Tiao Hong V Cir)Alex CustodioОценок пока нет

- 01.04.2022 To 20.02.2023Документ22 страницы01.04.2022 To 20.02.2023PrashantОценок пока нет

- Amazon - ChairДокумент1 страницаAmazon - Chairpiyush.sinhaОценок пока нет

- HDFC Bank Credit Cards GSTIN: 33AAACH2702H2Z6 HSN Code - 9971Документ3 страницыHDFC Bank Credit Cards GSTIN: 33AAACH2702H2Z6 HSN Code - 9971MadhuОценок пока нет

- AAДокумент11 страницAAJames wiliamОценок пока нет

- Income Tax Calulator With Functions and Robus Validation: PFC - Assignment - Part 1Документ4 страницыIncome Tax Calulator With Functions and Robus Validation: PFC - Assignment - Part 1tran nguyenОценок пока нет

- Assessment of House Tax in GPsДокумент2 страницыAssessment of House Tax in GPskamalakarvreddy0% (1)

- Gross Income: Income Taxation 5Th Edition (By: Valencia & Roxas) Suggested AnswersДокумент7 страницGross Income: Income Taxation 5Th Edition (By: Valencia & Roxas) Suggested AnswersAnonymous qpUaTkОценок пока нет

- What Is and Is Not Reportable On 1099Документ9 страницWhat Is and Is Not Reportable On 1099joy100% (3)

- TD Beyond Checking: Account SummaryДокумент4 страницыTD Beyond Checking: Account SummaryJohn BeanОценок пока нет

- 8.bill PrintДокумент1 страница8.bill Printricky009Оценок пока нет

- Postpaid Monthly Statement: This Month's SummaryДокумент4 страницыPostpaid Monthly Statement: This Month's SummaryJinesh JadavОценок пока нет

- Other Percentage TaxesДокумент40 страницOther Percentage TaxesKay Hanalee Villanueva NorioОценок пока нет

- Payroll Deductions Group 2Документ15 страницPayroll Deductions Group 2Ronel A GaviolaОценок пока нет

- Fatima's Receipt PDFДокумент2 страницыFatima's Receipt PDFFaraz NaqviОценок пока нет

- CIR V. TRANSITIONS OPTICAL PHILIPPINES, INC. (G.R. No. 227544, November 22, 2017)Документ2 страницыCIR V. TRANSITIONS OPTICAL PHILIPPINES, INC. (G.R. No. 227544, November 22, 2017)Digna LausОценок пока нет

- A New Look at Indirect Taxation in Developing Countries: University of TorontoДокумент11 страницA New Look at Indirect Taxation in Developing Countries: University of TorontoKatindig CarlОценок пока нет

- 2.5 Cash Books: Two Column Cash BookДокумент6 страниц2.5 Cash Books: Two Column Cash Bookwilliam koechОценок пока нет