Вам также может понравиться

- Types of stamps and concepts of stamp dutyДокумент5 страницTypes of stamps and concepts of stamp dutyNikhil Kasat100% (2)

- Financial Swaps EditedДокумент19 страницFinancial Swaps EditedMaria U DavidОценок пока нет

- 2013-06 Credit Derivatives Workshop - JPMДокумент156 страниц2013-06 Credit Derivatives Workshop - JPMjamieelliottОценок пока нет

- International DerivativesДокумент56 страницInternational DerivativesPradyumna SwainОценок пока нет

- Derivatives - Futures and ForwardsДокумент56 страницDerivatives - Futures and ForwardsSriram VasudevanОценок пока нет

- Commodity Broker ListДокумент33 страницыCommodity Broker Listdabuffman9497Оценок пока нет

- Guide to Swaps and DerivativesДокумент32 страницыGuide to Swaps and Derivativesswesam123Оценок пока нет

- Risks and Derivatives ExplainedДокумент59 страницRisks and Derivatives ExplainedVikramTripathiОценок пока нет

- OTC Derivatives - Product History and Regulation (9-09)Документ87 страницOTC Derivatives - Product History and Regulation (9-09)Manish AnandОценок пока нет

- DerivativesДокумент79 страницDerivativesPaul Christian Lopez FiedacanОценок пока нет

- Technical Analysis of Stocks & Commodities TASC APRIL 2020 PDFДокумент64 страницыTechnical Analysis of Stocks & Commodities TASC APRIL 2020 PDFMattia80% (5)

- COPPER BrochureДокумент8 страницCOPPER BrochurelaxmiccОценок пока нет

- Kenneth Shaleen Volume and Open Interest PDFДокумент235 страницKenneth Shaleen Volume and Open Interest PDFHenry Ng67% (3)

- Derivatives Chapter 2 (Introduction To Futures)Документ45 страницDerivatives Chapter 2 (Introduction To Futures)zaryОценок пока нет

- Derivatives Chapter 2 (Introduction To Futures)Документ45 страницDerivatives Chapter 2 (Introduction To Futures)zaryОценок пока нет

- Introduction of Currency DerivativesДокумент28 страницIntroduction of Currency DerivativesChetan Patel100% (1)

- f59676736 Slide 1Документ18 страницf59676736 Slide 1Hassan AliОценок пока нет

- Investing in Fixed Income Securities: Understanding the Bond MarketОт EverandInvesting in Fixed Income Securities: Understanding the Bond MarketОценок пока нет

- International Money Market InstrumentsДокумент18 страницInternational Money Market InstrumentsThapar McaОценок пока нет

- Hedging With Financial DerivativesДокумент71 страницаHedging With Financial Derivativeshabiba ahmedОценок пока нет

- Introduction to Credit Derivatives: Understanding Risk and ReturnДокумент30 страницIntroduction to Credit Derivatives: Understanding Risk and ReturnSoumya MishraОценок пока нет

- A Study On Commodity DerivativeДокумент22 страницыA Study On Commodity DerivativeCm Chugh100% (1)

- My Project SharekhanДокумент154 страницыMy Project Sharekhankris_sone43% (7)

- FX Risk Management Transaction Exposure: Slide 1Документ55 страницFX Risk Management Transaction Exposure: Slide 1prakashputtuОценок пока нет

- Introduction To Agribusiness Management PDFДокумент141 страницаIntroduction To Agribusiness Management PDFAkanksha Deshmukh92% (12)

- Mining Finance Interview PrepДокумент17 страницMining Finance Interview PrepIshanSaneОценок пока нет

- Derivative MarketsДокумент60 страницDerivative MarketswaqarОценок пока нет

- CH 24Документ68 страницCH 24Rachel LeachonОценок пока нет

- Saqib M26 - MISH1520 - 06 - PPW - C25Документ40 страницSaqib M26 - MISH1520 - 06 - PPW - C25Tariq MahmoodОценок пока нет

- Financial Futures Markets: Chapter ObjectivesДокумент22 страницыFinancial Futures Markets: Chapter ObjectivesViệt NữОценок пока нет

- Chapter Five: Financial Risk ManagementДокумент26 страницChapter Five: Financial Risk ManagementJerome MogaОценок пока нет

- Futures Options and Swaps PPT MBA FINANCEДокумент11 страницFutures Options and Swaps PPT MBA FINANCEBabasab Patil (Karrisatte)Оценок пока нет

- Techniques of Asset/liability Management: Futures, Options, and SwapsДокумент19 страницTechniques of Asset/liability Management: Futures, Options, and SwapsNishant Verma100% (1)

- Future OptionsДокумент23 страницыFuture OptionsTho ThoОценок пока нет

- Derivados UP CFAДокумент47 страницDerivados UP CFAAugusto Peña ChavezОценок пока нет

- CUHK RMSC2001 Chapter 6 NotesДокумент17 страницCUHK RMSC2001 Chapter 6 NotesanthetОценок пока нет

- Derivatives and RMДокумент35 страницDerivatives and RMMichael WardОценок пока нет

- Currency Derivatives: South-Western/Thomson Learning © 2006Документ26 страницCurrency Derivatives: South-Western/Thomson Learning © 2006Harish Chowdary TummalaОценок пока нет

- FINMAR INSTITUTION - Chapter 24 Hedging With Financial DerivativesДокумент51 страницаFINMAR INSTITUTION - Chapter 24 Hedging With Financial DerivativesKenneth MallariОценок пока нет

- Derivatives - Futures: Forward ContractsДокумент5 страницDerivatives - Futures: Forward ContractsNeeta LokhundeОценок пока нет

- CH 06 Interest Rate FuturesДокумент28 страницCH 06 Interest Rate FuturesSyed Usama RashidОценок пока нет

- Currency FuturesДокумент4 страницыCurrency FuturesMubin PollobОценок пока нет

- Crude Oil Futures and Forward Contract GuideДокумент30 страницCrude Oil Futures and Forward Contract GuideArchana BalikramОценок пока нет

- Derivatives: Risks and RewardsДокумент15 страницDerivatives: Risks and RewardsAnkit SakhujaОценок пока нет

- Money MarketsДокумент21 страницаMoney Markets9986212378Оценок пока нет

- Financial Institutions Management - Chap024Документ20 страницFinancial Institutions Management - Chap024Wendy YipОценок пока нет

- S 57Документ18 страницS 57blah123123123Оценок пока нет

- D86femodule 6Документ47 страницD86femodule 6Sonia KapoorОценок пока нет

- Jignesh Shah Dhiren Prajapati Kaustubh Parkar Akash Jadhav Deepali Jain Rahul GavaliДокумент43 страницыJignesh Shah Dhiren Prajapati Kaustubh Parkar Akash Jadhav Deepali Jain Rahul GavaliDhiren Praj100% (1)

- Lecture 24 ME CH 24 Financial DerivativesДокумент53 страницыLecture 24 ME CH 24 Financial DerivativesAlif SultanliОценок пока нет

- Chapter 10 - Investment Strategies and Risk ManagementДокумент21 страницаChapter 10 - Investment Strategies and Risk Managementcyclone man100% (1)

- Lecture 141Документ35 страницLecture 141Krishan988Оценок пока нет

- Quiz Thị Trường Tài Chính Phái SinhДокумент25 страницQuiz Thị Trường Tài Chính Phái SinhNguyễn Thế BảoОценок пока нет

- The Money Markets: Presented by Group 1Документ28 страницThe Money Markets: Presented by Group 1Candice Bolay-ogОценок пока нет

- Transaction ExposureДокумент6 страницTransaction ExposureDennis MarchelОценок пока нет

- Currency Derivatives: South-Western/Thomson Learning © 2003Документ40 страницCurrency Derivatives: South-Western/Thomson Learning © 2003Lincy KurianОценок пока нет

- Hedge Fund Strategies: A Do It Yourself Approach: DisclaimerДокумент27 страницHedge Fund Strategies: A Do It Yourself Approach: DisclaimerdjbenbrownОценок пока нет

- Futures - Meaning, Types, Mechanism, SEBI GuidelinesДокумент49 страницFutures - Meaning, Types, Mechanism, SEBI GuidelinesKARISHMAAT67% (6)

- Commodities and Financial FuturesДокумент36 страницCommodities and Financial Futuresjhonatan jhonatanОценок пока нет

- Understanding The Money Market: - Money Market Instruments Are Low Risk, Highly Liquid, and ofДокумент12 страницUnderstanding The Money Market: - Money Market Instruments Are Low Risk, Highly Liquid, and oftapia4yeabuОценок пока нет

- DerivativesДокумент7 страницDerivativesMuhammadIjazAslamОценок пока нет

- Sellers: Depth of Market Market - Asp#Ixzz58Efpzor7Документ6 страницSellers: Depth of Market Market - Asp#Ixzz58Efpzor7Tom BenningaОценок пока нет

- Funding of Dealer Positions and Repurchase Agreements ExplainedДокумент130 страницFunding of Dealer Positions and Repurchase Agreements ExplainedKanchan SharmaОценок пока нет

- Financial Institutions: Submitted To: Sharique Ayubi Submitted By: Abdul Samad Munaf ID: 8905 Date: 9 December 2009Документ18 страницFinancial Institutions: Submitted To: Sharique Ayubi Submitted By: Abdul Samad Munaf ID: 8905 Date: 9 December 2009Muzammil YounusОценок пока нет

- L180030 - BBA Section B - Maham Fatima MirДокумент7 страницL180030 - BBA Section B - Maham Fatima MirMųhåmmāđÄbęêřОценок пока нет

- Exchange Rate Derivatives: South-Western/Thomson Learning © 2006Документ30 страницExchange Rate Derivatives: South-Western/Thomson Learning © 2006Adi PhasaОценок пока нет

- Finance CIA2 - AnkitaДокумент14 страницFinance CIA2 - AnkitaAnkita SinghОценок пока нет

- Financial Markets GuideДокумент118 страницFinancial Markets Guidechekurisekhar100% (1)

- Income Declaration Scheme Rules, 2016: Form 1Документ9 страницIncome Declaration Scheme Rules, 2016: Form 1Nikhil KasatОценок пока нет

- Sale DeedДокумент5 страницSale DeedNitin GoyalОценок пока нет

- DTL Sec 10Документ14 страницDTL Sec 10Nikhil KasatОценок пока нет

- BLack Money RulesДокумент23 страницыBLack Money RulesLive LawОценок пока нет

- Black Money BillДокумент30 страницBlack Money BillNikhil KasatОценок пока нет

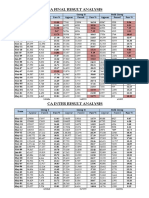

- CA Result AnalysisДокумент1 страницаCA Result AnalysisNikhil KasatОценок пока нет

- Delhi Dvat Registration InformationДокумент4 страницыDelhi Dvat Registration InformationNikhil KasatОценок пока нет

- Derivatives Markets in Interest Rate & Foreign Exchange RateДокумент20 страницDerivatives Markets in Interest Rate & Foreign Exchange RatehdjfhsjfhwjfОценок пока нет

- Banca SuranceДокумент32 страницыBanca SuranceNikhil KasatОценок пока нет

- Some Confusing & Debatable CSR Issues: Learning Series Vol.-I Issue - 2 2015-16Документ21 страницаSome Confusing & Debatable CSR Issues: Learning Series Vol.-I Issue - 2 2015-16Nikhil KasatОценок пока нет

- ApplicabiliTY of ProvisionsДокумент3 страницыApplicabiliTY of ProvisionsNikhil KasatОценок пока нет

- Agricultural Income: Agricultural Income: - As Per Sec 10 (1) Agricultural Income Earned by TheДокумент9 страницAgricultural Income: Agricultural Income: - As Per Sec 10 (1) Agricultural Income Earned by TheNikhil KasatОценок пока нет

- How to score 12-14 marks on Professional Ethics exam questionsДокумент2 страницыHow to score 12-14 marks on Professional Ethics exam questionsNikhil KasatОценок пока нет

- List of Indian As Convergence With IfrsДокумент1 страницаList of Indian As Convergence With IfrsNikhil KasatОценок пока нет

- Importance of ArticleshipДокумент6 страницImportance of ArticleshipNikhil KasatОценок пока нет

- Calculate Fees and Stamp Duty for Increase in Authorised Share CapitalДокумент10 страницCalculate Fees and Stamp Duty for Increase in Authorised Share CapitalNikhil KasatОценок пока нет

- Anf 4dДокумент3 страницыAnf 4dNikhil KasatОценок пока нет

- Web Base Timesheet ApplicationДокумент4 страницыWeb Base Timesheet ApplicationNikhil KasatОценок пока нет

- Directors Report As Per StatusДокумент5 страницDirectors Report As Per StatusNikhil KasatОценок пока нет

- Privileges To Small CompaniesДокумент2 страницыPrivileges To Small CompaniesNikhil KasatОценок пока нет

- Ind As 2015Документ2 страницыInd As 2015Nikhil KasatОценок пока нет

- Valuation of InventoriesДокумент4 страницыValuation of InventoriesNikhil KasatОценок пока нет

- Tds On SalariesДокумент55 страницTds On SalariespunitОценок пока нет

- August Month CompliancesДокумент1 страницаAugust Month CompliancesNikhil KasatОценок пока нет

- Curriculum VitaeДокумент13 страницCurriculum VitaeNikhil KasatОценок пока нет

- CUSTOMS VALUATION COMPUTATIONДокумент8 страницCUSTOMS VALUATION COMPUTATIONNikhil KasatОценок пока нет

- C01Документ23 страницыC01Silvery DoeОценок пока нет

- Madura14e Ch05 FinalДокумент43 страницыMadura14e Ch05 FinalVũ Trần Nhật ViОценок пока нет

- Special Topics in Financial ManagementДокумент4 страницыSpecial Topics in Financial ManagementChristel Mae BoseoОценок пока нет

- FAQ on futures trading, squaring off positions, and margin requirementsДокумент155 страницFAQ on futures trading, squaring off positions, and margin requirementsMas ThulanОценок пока нет

- FFOM8ETBHДокумент7 страницFFOM8ETBHEnayet HossainОценок пока нет

- Market Focus: Use of Derivatives in BrazilДокумент20 страницMarket Focus: Use of Derivatives in Brazildavy1980Оценок пока нет

- Board of Trade of Chicago v. Olsen, 262 U.S. 1 (1923)Документ20 страницBoard of Trade of Chicago v. Olsen, 262 U.S. 1 (1923)Scribd Government DocsОценок пока нет

- How Naira-Settled OTC FX Futures WorkДокумент4 страницыHow Naira-Settled OTC FX Futures WorkmayorladОценок пока нет

- Inerals & Etals Eview: China To Release Base Metals' Stocks To Stabilise PricesДокумент20 страницInerals & Etals Eview: China To Release Base Metals' Stocks To Stabilise Priceskalyan majumdarОценок пока нет

- DM - IntroductionДокумент88 страницDM - IntroductionSagar PatilОценок пока нет

- Aluminium Value ChainДокумент25 страницAluminium Value Chainanmol gargОценок пока нет

- Investor Presentation (Company Update)Документ34 страницыInvestor Presentation (Company Update)Shyam SunderОценок пока нет

- DerivativesДокумент241 страницаDerivativesSomnath Rath (M20MS059)Оценок пока нет

- PROJECT On Commodity Market From Nirmal Bang by PLABAN KUNDUДокумент68 страницPROJECT On Commodity Market From Nirmal Bang by PLABAN KUNDUPlaban Kundu67% (6)

- The ConstructДокумент36 страницThe Constructjadie aliОценок пока нет

- Forward ContractДокумент31 страницаForward ContractsandipОценок пока нет

- Chapters 20, 22 & 24Документ59 страницChapters 20, 22 & 24Manidipa BoseОценок пока нет

- Investors' perception of India's equity derivatives marketДокумент53 страницыInvestors' perception of India's equity derivatives marketSubodh MalkarОценок пока нет

- Agriculture and CommodityДокумент10 страницAgriculture and CommodityKalkidan TerefeОценок пока нет

- Drinka and McNutt Market ProfileДокумент9 страницDrinka and McNutt Market Profilemail_ratanОценок пока нет

- Differences Between Forward, Futures and OptionsДокумент10 страницDifferences Between Forward, Futures and OptionsDIANA CABALLEROОценок пока нет

- Aditya Birla Money ProjectДокумент58 страницAditya Birla Money ProjectPrateek Rastogi100% (1)