Вам также может понравиться

- Isa 580Документ12 страницIsa 580baabasaamОценок пока нет

- PSA-580 Written RepresentationДокумент20 страницPSA-580 Written Representationcolleenyu0% (1)

- International Standard On Auditing 580 Written RepresentationsДокумент17 страницInternational Standard On Auditing 580 Written RepresentationsAnas IftikharОценок пока нет

- Psa 580 Revised and RedraftedДокумент20 страницPsa 580 Revised and RedraftedJongseong ParkОценок пока нет

- Isa 810Документ18 страницIsa 810baabasaamОценок пока нет

- SSA-210-R1 Agreeing The Terms of Audit EngagementsДокумент22 страницыSSA-210-R1 Agreeing The Terms of Audit EngagementsAndreiОценок пока нет

- Psa 210 RedraftedДокумент40 страницPsa 210 RedraftedRarajОценок пока нет

- ISA 580 Standalone 2009 HandbookДокумент20 страницISA 580 Standalone 2009 HandbookMariana MirelaОценок пока нет

- Hapter Udit EPORT (SA 700, 701, 705, 706) : Objective of The Auditor As Per SA 700Документ11 страницHapter Udit EPORT (SA 700, 701, 705, 706) : Objective of The Auditor As Per SA 700S.SeethalakshmiОценок пока нет

- A Project Report On:: Third Year: Sixth SemesterДокумент11 страницA Project Report On:: Third Year: Sixth SemesterNikhl MahajanОценок пока нет

- Communicating Audit Results to GovernanceДокумент26 страницCommunicating Audit Results to GovernancecolleenyuОценок пока нет

- PSA 810 Report on Summary Financial StatementsДокумент17 страницPSA 810 Report on Summary Financial StatementsLorelyn LariozaОценок пока нет

- Proposed Conforming Amendments To Other SSAs1Документ8 страницProposed Conforming Amendments To Other SSAs1AndreiОценок пока нет

- SA 450 EvaluationДокумент13 страницSA 450 Evaluationjohnsondevasia80Оценок пока нет

- Singapore Standard On AuditingДокумент19 страницSingapore Standard On AuditingbabylovelylovelyОценок пока нет

- Audit ReportДокумент62 страницыAudit ReportPranay NavvulaОценок пока нет

- Shaivi Shah - AUDITДокумент12 страницShaivi Shah - AUDITShaiviОценок пока нет

- "Representations by Management", Issued by The Council of The Institute of CharteredДокумент7 страниц"Representations by Management", Issued by The Council of The Institute of CharteredRishabh GuptaОценок пока нет

- 1Документ35 страниц1Rommel CruzОценок пока нет

- SSA 210: Key requirements for agreeing audit termsДокумент21 страницаSSA 210: Key requirements for agreeing audit termsbabylovelylovelyОценок пока нет

- SLAuS 700: Forming an Opinion and Reporting on Financial StatementsДокумент9 страницSLAuS 700: Forming an Opinion and Reporting on Financial Statementsnaveen pragash100% (1)

- Gaap and AuditДокумент35 страницGaap and AuditAayushi AroraОценок пока нет

- Evaluate Financial MisstatementsДокумент11 страницEvaluate Financial MisstatementsSebastian GarciaОценок пока нет

- Audit ReportДокумент18 страницAudit ReportSricharan Reddy R100% (1)

- PAPS-1000Ph Revised FinalДокумент11 страницPAPS-1000Ph Revised FinalNigelT.LeeОценок пока нет

- GN - S.143Документ12 страницGN - S.143Goda AgrajaОценок пока нет

- © The Institute of Chartered Accountants of IndiaДокумент138 страниц© The Institute of Chartered Accountants of IndiaPraveen Reddy DevanapalleОценок пока нет

- SSA 450 EVALUATION OF MISSTATEMENTSДокумент10 страницSSA 450 EVALUATION OF MISSTATEMENTSbabylovelylovelyОценок пока нет

- Sa 700 PDFДокумент67 страницSa 700 PDFRoshanjit ThakurОценок пока нет

- SA 450 EVALUATION OF MISSTATEMENTSДокумент13 страницSA 450 EVALUATION OF MISSTATEMENTSLaura D'souzaОценок пока нет

- ISA 701 (Revised) Communicating Key Audit Matters in The Independent Auditor's Report PDFДокумент24 страницыISA 701 (Revised) Communicating Key Audit Matters in The Independent Auditor's Report PDFIrina TosunОценок пока нет

- Reporting on Financial Statements (ISA 700Документ22 страницыReporting on Financial Statements (ISA 700baabasaamОценок пока нет

- Singapore Standard On AuditingДокумент29 страницSingapore Standard On AuditingbabylovelylovelyОценок пока нет

- What Is This ConvertДокумент12 страницWhat Is This ConvertAhmed HussainОценок пока нет

- ISA 800 - Audits of Financial Statements Prepared Under Special Purpose FrameworksДокумент11 страницISA 800 - Audits of Financial Statements Prepared Under Special Purpose FrameworksbaabasaamОценок пока нет

- Unit 6Документ14 страницUnit 6YonasОценок пока нет

- AASC Alert 001 of 2011 Revised Audit OpinionДокумент3 страницыAASC Alert 001 of 2011 Revised Audit OpinionGlenn TaduranОценок пока нет

- 12the Auditors Report On FS (Samples)Документ22 страницы12the Auditors Report On FS (Samples)Franz CampuedОценок пока нет

- Forming Audit Opinions & Financial ReportsДокумент10 страницForming Audit Opinions & Financial ReportsRufina B VerdeОценок пока нет

- Module - 2 Auditor'S Report: Objectives of The AuditorДокумент20 страницModule - 2 Auditor'S Report: Objectives of The AuditorVijay KumarОценок пока нет

- Draft Accounting Standard 1 on Financial Statement PresentationДокумент26 страницDraft Accounting Standard 1 on Financial Statement PresentationratiОценок пока нет

- Psa 210 PDFДокумент22 страницыPsa 210 PDFLuzz LandichoОценок пока нет

- Sec 7060Документ17 страницSec 7060Fallon LoboОценок пока нет

- PSA-706 Emphasis On Matter Paragraphs & Other Matter Paragraphs in The Independent Auditor's ReportДокумент14 страницPSA-706 Emphasis On Matter Paragraphs & Other Matter Paragraphs in The Independent Auditor's ReportcolleenyuОценок пока нет

- Reports On Audited Financial Statements PDFДокумент28 страницReports On Audited Financial Statements PDFoptimistic070% (1)

- Audit EngagementДокумент2 страницыAudit EngagementMuhammad Usman SaeedОценок пока нет

- Auditing: Module 4 Forming An Opinion and Reporting On Financial StatementsДокумент48 страницAuditing: Module 4 Forming An Opinion and Reporting On Financial StatementsJohn Archie AntonioОценок пока нет

- Comm - Ica Asa510 App1ill1Документ3 страницыComm - Ica Asa510 App1ill1Hay JirenyaaОценок пока нет

- ISA 700 eДокумент41 страницаISA 700 eAvinash BabykuttyОценок пока нет

- Format of Management Representation LetterДокумент6 страницFormat of Management Representation LetterSarowar AlamОценок пока нет

- Singapore Standard On AuditingДокумент14 страницSingapore Standard On AuditingbabylovelylovelyОценок пока нет

- Forming An Opinion and Reporting On Financial StatementsДокумент19 страницForming An Opinion and Reporting On Financial StatementsMyka4Оценок пока нет

- Illustration 2 - CFS - Ind As Auditor's Report - Listed - Unqualified - 201904Документ14 страницIllustration 2 - CFS - Ind As Auditor's Report - Listed - Unqualified - 201904Vrinda AgrawalОценок пока нет

- Revised Audit ReportДокумент16 страницRevised Audit ReportTekumani Naveen KumarОценок пока нет

- PSA 700 on Forming an Opinion and Auditor's ReportДокумент1 страницаPSA 700 on Forming an Opinion and Auditor's Reportkimjoonmyeon22Оценок пока нет

- Audit Report ElementsДокумент15 страницAudit Report ElementsAninditra NuraufiОценок пока нет

- Codification of Statements on Standards for Accounting and Review Services: Numbers 1 - 23От EverandCodification of Statements on Standards for Accounting and Review Services: Numbers 1 - 23Оценок пока нет

- Codification of Statements on Standards for Accounting and Review Services: Numbers 21-24От EverandCodification of Statements on Standards for Accounting and Review Services: Numbers 21-24Оценок пока нет

- Annual Update and Practice Issues for Preparation, Compilation, and Review EngagementsОт EverandAnnual Update and Practice Issues for Preparation, Compilation, and Review EngagementsОценок пока нет

- Engagement Essentials: Preparation, Compilation, and Review of Financial StatementsОт EverandEngagement Essentials: Preparation, Compilation, and Review of Financial StatementsОценок пока нет

- This Paper Is Not To Be Removed From The Examination HallsДокумент3 страницыThis Paper Is Not To Be Removed From The Examination HallsbabylovelylovelyОценок пока нет

- St104a Za 11Документ19 страницSt104a Za 11jjw1234Оценок пока нет

- Singapore Standard On AuditingДокумент19 страницSingapore Standard On AuditingbabylovelylovelyОценок пока нет

- SSA 530 Audit SamplingДокумент14 страницSSA 530 Audit SamplingbabylovelylovelyОценок пока нет

- Singapore Standard On AuditingДокумент7 страницSingapore Standard On AuditingbabylovelylovelyОценок пока нет

- Singapore Standard On Auditing: Conforming AmendmentsДокумент9 страницSingapore Standard On Auditing: Conforming AmendmentsbabylovelylovelyОценок пока нет

- Singapore Standard On AuditingДокумент14 страницSingapore Standard On AuditingbabylovelylovelyОценок пока нет

- St104a Za 11Документ19 страницSt104a Za 11jjw1234Оценок пока нет

- Singapore Standard On AuditingДокумент19 страницSingapore Standard On AuditingbabylovelylovelyОценок пока нет

- Singapore Standard On AuditingДокумент28 страницSingapore Standard On AuditingbabylovelylovelyОценок пока нет

- Singapore Standard On AuditingДокумент18 страницSingapore Standard On AuditingbabylovelylovelyОценок пока нет

- Singapore Standard On AuditingДокумент29 страницSingapore Standard On AuditingbabylovelylovelyОценок пока нет

- Singapore Standard On AuditingДокумент10 страницSingapore Standard On AuditingbabylovelylovelyОценок пока нет

- Singapore Standard On AuditingДокумент14 страницSingapore Standard On AuditingbabylovelylovelyОценок пока нет

- SSA 450 EVALUATION OF MISSTATEMENTSДокумент10 страницSSA 450 EVALUATION OF MISSTATEMENTSbabylovelylovelyОценок пока нет

- Singapore Standard On AuditingДокумент10 страницSingapore Standard On AuditingbabylovelylovelyОценок пока нет

- Communicating Deficiencies in Internal ControlДокумент11 страницCommunicating Deficiencies in Internal ControlbabylovelylovelyОценок пока нет

- Singapore Standard On AuditingДокумент10 страницSingapore Standard On AuditingbabylovelylovelyОценок пока нет

- Singapore Standard On AuditingДокумент20 страницSingapore Standard On AuditingbabylovelylovelyОценок пока нет

- HFHGFHGHDGSFDHDGGFGДокумент44 страницыHFHGFHGHDGSFDHDGGFGbabylovelylovelyОценок пока нет

- HFHGFHGHDGSFDHDGGFG QДокумент12 страницHFHGFHGHDGSFDHDGGFG QbabylovelylovelyОценок пока нет

- Communicating Deficiencies in Internal ControlДокумент11 страницCommunicating Deficiencies in Internal ControlbabylovelylovelyОценок пока нет

- SSA 210: Key requirements for agreeing audit termsДокумент21 страницаSSA 210: Key requirements for agreeing audit termsbabylovelylovelyОценок пока нет

- Singapore Standard On AuditingДокумент20 страницSingapore Standard On AuditingbabylovelylovelyОценок пока нет

- HFHGFHGHDGSFDHDGGFGДокумент17 страницHFHGFHGHDGSFDHDGGFGbabylovelylovelyОценок пока нет

- HFHGFHGHDGSFDHDGGFGДокумент31 страницаHFHGFHGHDGSFDHDGGFGbabylovelylovelyОценок пока нет

- Singapore Standard On AuditingДокумент12 страницSingapore Standard On AuditingbabylovelylovelyОценок пока нет

- HFHGFHGHDGSFDHDGGFGДокумент31 страницаHFHGFHGHDGSFDHDGGFGbabylovelylovelyОценок пока нет

- SSA 450 EVALUATION OF MISSTATEMENTSДокумент10 страницSSA 450 EVALUATION OF MISSTATEMENTSbabylovelylovelyОценок пока нет

- TRIPS AgreementДокумент32 страницыTRIPS AgreementVineet JainОценок пока нет

- Hechanova Vs Adil CaseДокумент3 страницыHechanova Vs Adil CaseCarol JacintoОценок пока нет

- DONALD HYDE, JACKIE HYDE V NJ Dept of Children and FamiliesДокумент7 страницDONALD HYDE, JACKIE HYDE V NJ Dept of Children and FamiliesopracrusadesОценок пока нет

- Mudajaya Scholarship ApplicationДокумент4 страницыMudajaya Scholarship ApplicationAmir WafiyОценок пока нет

- Baguno Vs Agabao Primary JurisdictionДокумент8 страницBaguno Vs Agabao Primary JurisdictionKuyaОценок пока нет

- Affidavit of Undertaking of Compliance To The Minimum Qualifications and RequirementsДокумент1 страницаAffidavit of Undertaking of Compliance To The Minimum Qualifications and RequirementsKaren GuiuoОценок пока нет

- Prudential Bank Vs PanisДокумент7 страницPrudential Bank Vs PanisEller-jed M. Mendoza100% (2)

- Spouses Fuentes Vs RocaДокумент4 страницыSpouses Fuentes Vs RocaJuan Carlo CastanedaОценок пока нет

- Cao 29.11Документ15 страницCao 29.11tdfsksОценок пока нет

- Tumagan Et AlДокумент3 страницыTumagan Et AlKrisleen AbrenicaОценок пока нет

- Mutual, 2-Way NDAДокумент7 страницMutual, 2-Way NDAponticarlo7658Оценок пока нет

- International Business Lawst200813 - 0 PDFДокумент340 страницInternational Business Lawst200813 - 0 PDFkanika1Оценок пока нет

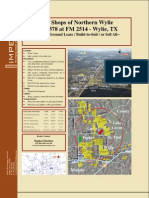

- Shops of Northern Wylie (Imperium Holdings)Документ3 страницыShops of Northern Wylie (Imperium Holdings)Imperium Holdings, LPОценок пока нет

- Balfour Vs BalfourДокумент2 страницыBalfour Vs BalfourIddi KassiОценок пока нет

- Is Estoppel A Fetter On The Exercise of DiscretionДокумент4 страницыIs Estoppel A Fetter On The Exercise of DiscretionKeabetswe Kolobetso MolotsiОценок пока нет

- Puravankara Projects Limited Vs MR P Dayananda Pai S - O Late P ..Документ8 страницPuravankara Projects Limited Vs MR P Dayananda Pai S - O Late P ..CacptCoachingОценок пока нет

- Civil Procedure OutlineДокумент102 страницыCivil Procedure OutlineMichael Morabito100% (2)

- Green NotesДокумент67 страницGreen NotesIzza AnsamaОценок пока нет

- LA TRINIDAD POLICE DEPARTMENT SERVICESДокумент12 страницLA TRINIDAD POLICE DEPARTMENT SERVICESLhor DeineОценок пока нет

- Special Power of Attorney DocДокумент3 страницыSpecial Power of Attorney DocgerrymanderingОценок пока нет

- Doehle-Philman Manning Agency Inc vs. Henry C. HaroДокумент2 страницыDoehle-Philman Manning Agency Inc vs. Henry C. HaroMigoy DAОценок пока нет

- Civil Service CommissionДокумент20 страницCivil Service CommissionClea Amber FullanteОценок пока нет

- End-Of-Semester Examination SEMESTER I, 2007/2008 SESSION: Ahmad Ibrahim Kulliyyah of LawsДокумент6 страницEnd-Of-Semester Examination SEMESTER I, 2007/2008 SESSION: Ahmad Ibrahim Kulliyyah of LawsShuq Faqat al-FansuriОценок пока нет

- Notice To Cease and Desist RedactДокумент2 страницыNotice To Cease and Desist Redactmellowjohnny100% (15)

- Law of Contract II Assignment IIДокумент10 страницLaw of Contract II Assignment IIFrancis BandaОценок пока нет

- Phil Trust Co v. BohananДокумент2 страницыPhil Trust Co v. BohanandiegavillanuevaОценок пока нет

- Eft Z'., - ( : Upreme TtourtДокумент10 страницEft Z'., - ( : Upreme TtourtEmir MendozaОценок пока нет

- PAL v. RamosДокумент2 страницыPAL v. Ramoskim_santos_20Оценок пока нет

- CONTRACTS Past Paper QuestionsДокумент3 страницыCONTRACTS Past Paper QuestionsKerine Williams-Figaro100% (1)

- Giben America, Incorporated v. Schelling America, Incorporated Werner Deuring, Individually, 48 F.3d 1216, 4th Cir. (1995)Документ3 страницыGiben America, Incorporated v. Schelling America, Incorporated Werner Deuring, Individually, 48 F.3d 1216, 4th Cir. (1995)Scribd Government DocsОценок пока нет