Вам также может понравиться

- Format - MT799 MT760 MT 103.23Документ3 страницыFormat - MT799 MT760 MT 103.23kingmaker100% (11)

- Research ProposalДокумент3 страницыResearch ProposalAurangzaib Shahbaz100% (3)

- Final Research ProposalДокумент19 страницFinal Research ProposalAli Safina50% (2)

- B3 PDFДокумент465 страницB3 PDFabdulramani mbwana100% (7)

- Islamic and Conventional Banking Comparative Analysis, Pakistan's PerspectiveДокумент91 страницаIslamic and Conventional Banking Comparative Analysis, Pakistan's PerspectiveSaid Ali93% (15)

- Meezan Bank Internship ReportДокумент32 страницыMeezan Bank Internship ReportRanaAakashAhmadОценок пока нет

- Role of Commercial Banks in The Economic Development of PakistanДокумент2 страницыRole of Commercial Banks in The Economic Development of Pakistanasmi100% (2)

- Market Power, Stability, and Performance in Islamic Banks of Pakistan Research ProposalДокумент7 страницMarket Power, Stability, and Performance in Islamic Banks of Pakistan Research ProposalIrfan AliОценок пока нет

- Final ThesisДокумент86 страницFinal ThesisSuresh Muthu75% (16)

- Comparing Working Capital Management of Chemical and Medicine CompaniesДокумент17 страницComparing Working Capital Management of Chemical and Medicine CompaniesEmi KhanОценок пока нет

- Insurance Law-ContributionДокумент5 страницInsurance Law-ContributionDavid FongОценок пока нет

- AP.2902 - Property-Plant-And-Equipment - With AnswersДокумент9 страницAP.2902 - Property-Plant-And-Equipment - With AnswersEuhanna Karla BacolodОценок пока нет

- Challenges Facing Islamic BankingДокумент92 страницыChallenges Facing Islamic BankingMohamed Elgazwi88% (8)

- Comparison of Islamic and Conventional BanksДокумент57 страницComparison of Islamic and Conventional BanksInam Ul Haq ShahОценок пока нет

- People Perception Toward Islamic BankingДокумент15 страницPeople Perception Toward Islamic BankingHaroonОценок пока нет

- Factors affecting growth of Islamic Banking in PakistanДокумент25 страницFactors affecting growth of Islamic Banking in PakistanRana AhsanОценок пока нет

- Research Proposal - Determinants of Local Islamic Bank's Profitability in Malaysia 1Документ44 страницыResearch Proposal - Determinants of Local Islamic Bank's Profitability in Malaysia 1Khairi Izuan100% (1)

- Finance ThesisДокумент32 страницыFinance Thesissami_janiОценок пока нет

- Impact of Capital Structure on Profitability in Sri Lankan Manufacturing SectorДокумент45 страницImpact of Capital Structure on Profitability in Sri Lankan Manufacturing Sectoramith chathurangaОценок пока нет

- Important Projects Topics in FinanceДокумент10 страницImportant Projects Topics in Financesaddam hussainОценок пока нет

- Comparison Between Islamic Banking and Conventional Banking ProductsДокумент5 страницComparison Between Islamic Banking and Conventional Banking ProductsMuhammad TahirОценок пока нет

- The Study of Islamic Banking With Special Reference To Dubai Islamic BankДокумент69 страницThe Study of Islamic Banking With Special Reference To Dubai Islamic BankOmar Sharif100% (2)

- Importance of Islamic BankingДокумент1 страницаImportance of Islamic BankingBenish Gulzar100% (4)

- Accounting for Musyarakah Financing: Understanding the Key Concepts and TransactionsДокумент16 страницAccounting for Musyarakah Financing: Understanding the Key Concepts and TransactionsHadyan AntoroОценок пока нет

- Financial Crises 2007Документ30 страницFinancial Crises 2007Shubham GuptaОценок пока нет

- MBA Finance Thesis Topics List PDF: Equity Analysis of BanksДокумент4 страницыMBA Finance Thesis Topics List PDF: Equity Analysis of BanksbagyaОценок пока нет

- Determinants of Corporate Investment Decisions in VietnamДокумент10 страницDeterminants of Corporate Investment Decisions in VietnamAndy PhuongОценок пока нет

- Financial Analysis of Selected Textile CompaniesДокумент76 страницFinancial Analysis of Selected Textile CompaniesShahid Mehmood80% (10)

- Optimize Working Capital ManagementДокумент8 страницOptimize Working Capital ManagementAnnapurna VinjamuriОценок пока нет

- Islamic Banking and FinanceДокумент83 страницыIslamic Banking and Financeanon_879522740Оценок пока нет

- 3P - Finance With Other DisciplinesДокумент2 страницы3P - Finance With Other DisciplinesRaju RajendranОценок пока нет

- Elements of Banking PDFДокумент138 страницElements of Banking PDFMbu Javis Enow83% (6)

- NBP Internship ReportДокумент142 страницыNBP Internship ReportShahid Mehmood78% (9)

- Assignment On of Islamic BankingДокумент14 страницAssignment On of Islamic BankingSanjani80% (5)

- Islamic Banking Vs Conventional BankingДокумент17 страницIslamic Banking Vs Conventional BankingFarrukh Ahmed Qureshi100% (19)

- Thesis Sobia ShahzadiДокумент89 страницThesis Sobia ShahzadiRabia 8828Оценок пока нет

- Benefits of Islamic BankingДокумент2 страницыBenefits of Islamic Bankingazamkha100% (1)

- Issues and Problems of Islamic BankingДокумент14 страницIssues and Problems of Islamic Bankingziadiqbal19100% (9)

- Reasearch Proposal On Mutual FundДокумент8 страницReasearch Proposal On Mutual FundpalashmkhОценок пока нет

- Mba DissertationДокумент233 страницыMba Dissertationitumeleng1Оценок пока нет

- Portfolio ManagementДокумент82 страницыPortfolio ManagementVenkatОценок пока нет

- Research Assignment,,ProposalДокумент22 страницыResearch Assignment,,ProposalAbreham GetachewОценок пока нет

- Risk Management in Banking A Study With Reference-Risk Management in Banking A Study With ReferenceДокумент12 страницRisk Management in Banking A Study With Reference-Risk Management in Banking A Study With ReferencePavithra GowthamОценок пока нет

- Financial Literacy: Challenges For Indian EconomyДокумент14 страницFinancial Literacy: Challenges For Indian EconomyJediGodОценок пока нет

- Impact of Liquidity Crisis To Commercial Banks in ZimbabweДокумент21 страницаImpact of Liquidity Crisis To Commercial Banks in ZimbabweAleck Makandwa100% (1)

- Research ProposalДокумент30 страницResearch ProposalHamdan YuafiОценок пока нет

- A Feasibility Study On Islamic Banking in IndiaДокумент4 страницыA Feasibility Study On Islamic Banking in IndianadhirshaОценок пока нет

- The Financial Analysis of Himalyan Bank ComДокумент28 страницThe Financial Analysis of Himalyan Bank ComSushil Paudel100% (1)

- Research Proposal PDFДокумент30 страницResearch Proposal PDFSimon Muteke100% (1)

- Money & Banking BBA 5thДокумент2 страницыMoney & Banking BBA 5thMehmud Raffæy0% (1)

- Internship Report On UBL 2011 PDFДокумент63 страницыInternship Report On UBL 2011 PDFInamullah KhanОценок пока нет

- Islamic Banking ThesisДокумент95 страницIslamic Banking Thesism_nafees91% (11)

- Definition of Investment and Investment MechanismДокумент12 страницDefinition of Investment and Investment MechanismShaheen Mahmud50% (2)

- Internship Report on Programs and Operations of Hashoo FoundationДокумент44 страницыInternship Report on Programs and Operations of Hashoo FoundationAbid Ul Lah100% (1)

- An Analysis of Financial Performance of BRAC Bank LTD - Al SukranДокумент56 страницAn Analysis of Financial Performance of BRAC Bank LTD - Al SukranAl Sukran86% (7)

- A Capital Structure Management OF Nepal Investment Bank LTD and Citizen Bank LTDДокумент7 страницA Capital Structure Management OF Nepal Investment Bank LTD and Citizen Bank LTDkamal lamaОценок пока нет

- Islamic Banking QuestionnaireДокумент4 страницыIslamic Banking QuestionnaireMayank Gupta100% (2)

- Imperatives of Financial Innovation For Islamic BanksДокумент10 страницImperatives of Financial Innovation For Islamic BanksAria RanggabumiОценок пока нет

- Proposal by Afize JemalДокумент54 страницыProposal by Afize Jemaloumer muktarОценок пока нет

- Financial Markets: The Recent Experience of A Developing EconomyДокумент15 страницFinancial Markets: The Recent Experience of A Developing EconomyVedant BhansaliОценок пока нет

- Dilla University College of Business and Economics Department of Accounting and FinanceДокумент26 страницDilla University College of Business and Economics Department of Accounting and FinanceKindhun Tegegn100% (1)

- Islamic Syndication Vs ConventionalДокумент67 страницIslamic Syndication Vs ConventionalZubair BaigОценок пока нет

- Research MethodologyДокумент31 страницаResearch Methodologyshahzad ahmedОценок пока нет

- Master Policy Bond SPGIДокумент17 страницMaster Policy Bond SPGIDARSHAN ROYGAGAОценок пока нет

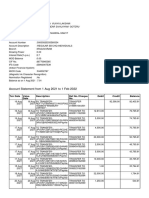

- Bank Statement SummaryДокумент8 страницBank Statement SummaryGULAB CHANDERОценок пока нет

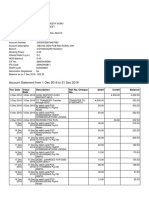

- Transaction StatementДокумент10 страницTransaction Statementsukeshsree sree33% (3)

- Citi Subsidiarys 2010 Exhibit 21-01Документ4 страницыCiti Subsidiarys 2010 Exhibit 21-01CarrieonicОценок пока нет

- Configure Dunning Procedures in SAPДокумент8 страницConfigure Dunning Procedures in SAPyalamanchili111Оценок пока нет

- R DJVFuh 3 Ri LB 7 Ep RДокумент13 страницR DJVFuh 3 Ri LB 7 Ep RKondayya JuttigaОценок пока нет

- Reconciling Bank Deposits and Interest Items for 7 YearsДокумент4 страницыReconciling Bank Deposits and Interest Items for 7 YearsJerwin Cases TiamsonОценок пока нет

- Export Finance: Presented By: Tamanna M.FTECH 2010-12 NIFT, GandhinagarДокумент19 страницExport Finance: Presented By: Tamanna M.FTECH 2010-12 NIFT, Gandhinagartamanna88Оценок пока нет

- Account Statement From 1 Dec 2016 To 31 Dec 2016: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceДокумент2 страницыAccount Statement From 1 Dec 2016 To 31 Dec 2016: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceENDLURI DEEPAK KUMARОценок пока нет

- CFP Risk Analysis and Insurance Planning Practice Book SampleДокумент34 страницыCFP Risk Analysis and Insurance Planning Practice Book SampleMeenakshi100% (7)

- Prêt-à-Porter RulesДокумент26 страницPrêt-à-Porter RulestobymaoОценок пока нет

- Gmail - Paper Acceptance Notification For Paper ID - IJISRT20AUG355Документ2 страницыGmail - Paper Acceptance Notification For Paper ID - IJISRT20AUG355Dialson PaulusОценок пока нет

- For Non Resident Indians: Account Opening FormДокумент16 страницFor Non Resident Indians: Account Opening Formshalabh2381Оценок пока нет

- The Reasons of This Question: 2. Levels of Career GoalsДокумент17 страницThe Reasons of This Question: 2. Levels of Career GoalsRaviraj ZalaОценок пока нет

- Comparative Study Housing Loans SBI UBIДокумент4 страницыComparative Study Housing Loans SBI UBINaresh HariyaniОценок пока нет

- Fi Annual 16Документ198 страницFi Annual 16sanchita sharmaОценок пока нет

- Proximate CauseДокумент4 страницыProximate CauseDavid GattОценок пока нет

- Loans and Credit CardsДокумент27 страницLoans and Credit CardsRose MarieОценок пока нет

- AudprobДокумент3 страницыAudprobJonalyn MoralesОценок пока нет

- CPA Board Examinations QuestionsДокумент14 страницCPA Board Examinations QuestionsJeane BongalanОценок пока нет

- Other STRBI Table No 15. Bank Group-Wise Classification of Loan Assets of Scheduled Commercial BanksДокумент4 страницыOther STRBI Table No 15. Bank Group-Wise Classification of Loan Assets of Scheduled Commercial BanksAman SinghОценок пока нет

- Bangayan vs. Rizal Commercial Banking CorporationДокумент31 страницаBangayan vs. Rizal Commercial Banking CorporationT Cel MrmgОценок пока нет

- A Study of Bank Audit ProcessДокумент61 страницаA Study of Bank Audit ProcessSunil PawarОценок пока нет

- Performance Appraisal System of AB Bank LTDДокумент67 страницPerformance Appraisal System of AB Bank LTDMahmud Abdullah100% (1)

- Online BankingДокумент40 страницOnline BankingIsmail HossainОценок пока нет

- Banking LawДокумент15 страницBanking LawDiksha OraonОценок пока нет