Вам также может понравиться

- A Firm's Sources of FinancingДокумент19 страницA Firm's Sources of FinancingisqmaОценок пока нет

- Budgeting Case Study: Put Laura's Budget TogetherДокумент2 страницыBudgeting Case Study: Put Laura's Budget TogetherUsman Ali50% (2)

- Code of Conduct for NBP EmployeesДокумент9 страницCode of Conduct for NBP Employeesasif khaniОценок пока нет

- Control Obj For Non-Current AssetsДокумент6 страницControl Obj For Non-Current AssetsTrần TùngОценок пока нет

- Negotiable Instruments Act, 1881 PDFДокумент61 страницаNegotiable Instruments Act, 1881 PDFmackjbl100% (3)

- Engineering Economy Replacement StudyДокумент28 страницEngineering Economy Replacement Studycyper zoonОценок пока нет

- 3 Service DesignfghДокумент51 страница3 Service DesignfghThomasGetyeОценок пока нет

- Guide to Hire Purchase FinancingДокумент21 страницаGuide to Hire Purchase FinancingkarthinathanОценок пока нет

- Perk Valuation of Motor CarДокумент18 страницPerk Valuation of Motor CarcapkaggarwalОценок пока нет

- Intercity Operations RFPДокумент11 страницIntercity Operations RFPJoseph LimОценок пока нет

- 3.1 Intro Equip Leasing Types of LeasesДокумент12 страниц3.1 Intro Equip Leasing Types of LeasesDecoster PardeepОценок пока нет

- Over-Capitalization Meaning, Causes and EffectsДокумент9 страницOver-Capitalization Meaning, Causes and EffectsselvakrishnaОценок пока нет

- Hire PurchaseДокумент30 страницHire PurchaseLeny MichaelОценок пока нет

- Hire Purchase PPT 1Документ17 страницHire Purchase PPT 1Virender Singh SahuОценок пока нет

- Example of Asset ReplacementДокумент1 страницаExample of Asset ReplacementflorentinaОценок пока нет

- Advantages and Disadvantages of LeasingДокумент1 страницаAdvantages and Disadvantages of LeasingMaribel ZafeОценок пока нет

- Data Bundles - MTN OnlineДокумент3 страницыData Bundles - MTN Onlineboewulf100% (1)

- Lecture 10-12 Capital Reconstruction SchemeДокумент23 страницыLecture 10-12 Capital Reconstruction SchemeGabriel korteyОценок пока нет

- Notes On Provident Fund & E.S.IДокумент2 страницыNotes On Provident Fund & E.S.IBhumika Pithadiya100% (2)

- Periodic Inventory SystemДокумент16 страницPeriodic Inventory SystemSohel Bangi100% (1)

- Plastic MoneyДокумент20 страницPlastic MoneyMohammad Saba100% (1)

- Types of LeasingДокумент22 страницыTypes of LeasingRavish Chitgope100% (2)

- How Companies Turn Cost Centers Into Profitable Business UnitsДокумент8 страницHow Companies Turn Cost Centers Into Profitable Business UnitschandanshaktiОценок пока нет

- Business Law Module GuideДокумент21 страницаBusiness Law Module GuideKai Sheng TanОценок пока нет

- TSI Physical Verification & TaggingДокумент6 страницTSI Physical Verification & TaggingCA Virendra ChhajerОценок пока нет

- Depreciation Calculation in ExcelДокумент8 страницDepreciation Calculation in ExcelVasanth Kumar VОценок пока нет

- Airport SLA GuideДокумент3 страницыAirport SLA GuideSa Xev100% (1)

- Asset Management: How AMCs Work for InvestorsДокумент2 страницыAsset Management: How AMCs Work for InvestorsDhoni KhanОценок пока нет

- BPMS Project IT HelpDeskДокумент16 страницBPMS Project IT HelpDeskfanwellОценок пока нет

- 06 Housing Finance - 2, (S-2) Auto, Personal, Edu LoansДокумент40 страниц06 Housing Finance - 2, (S-2) Auto, Personal, Edu LoansTarannum Aurora 20DM226Оценок пока нет

- Operating CostingДокумент37 страницOperating CostingkhairejoОценок пока нет

- 1 Lecture Let's Write An Impactful Business Plan!Документ41 страница1 Lecture Let's Write An Impactful Business Plan!Billyrefanto JpgОценок пока нет

- Hire PurchaseДокумент8 страницHire PurchaseAdityaОценок пока нет

- Finance InductionДокумент19 страницFinance InductionmenonpratishОценок пока нет

- Factoring Advantages and Dis AdvantagesДокумент1 страницаFactoring Advantages and Dis AdvantagesSiva RockОценок пока нет

- Guidelines for Preparing Effective Industrial Attachment ReportsДокумент7 страницGuidelines for Preparing Effective Industrial Attachment ReportsDZADZA YAOVIОценок пока нет

- Inventory Management ProjectДокумент89 страницInventory Management ProjectVinay Singh100% (1)

- E-PAYMENTДокумент3 страницыE-PAYMENTDave EdgarОценок пока нет

- Project Hire Purchase and LeasingДокумент29 страницProject Hire Purchase and Leasingsawantrohan214Оценок пока нет

- Leverage (Financial Management)Документ2 страницыLeverage (Financial Management)Rika Miyazaki100% (1)

- Chapter Five: Freight Forwarding OverviewДокумент19 страницChapter Five: Freight Forwarding OverviewAhmed HonestОценок пока нет

- Housing Finance: Presented by Sulekha Beri I.D.NO .43847Документ46 страницHousing Finance: Presented by Sulekha Beri I.D.NO .43847mehakdadwalОценок пока нет

- Expense ManagementДокумент4 страницыExpense Managementdemiss gebrieОценок пока нет

- Replacement Analysis: by Group IДокумент18 страницReplacement Analysis: by Group I55MESuman sahaОценок пока нет

- Replacement Analysis RevisedДокумент54 страницыReplacement Analysis RevisedCha Tingjuy100% (1)

- Engineering Economins-Replacement and Retention DecisionsДокумент74 страницыEngineering Economins-Replacement and Retention DecisionsAlbany SmashОценок пока нет

- Solar PV Sys Engg-Mod 10 1W Economic-Cons-mksДокумент39 страницSolar PV Sys Engg-Mod 10 1W Economic-Cons-mksOsama AsgharОценок пока нет

- Replace Equipment AnalysisДокумент12 страницReplace Equipment AnalysisPOGAKU KEERTHI MADHURIОценок пока нет

- EOQ and Differential Cost AnalysisДокумент4 страницыEOQ and Differential Cost AnalysisMerlita TuralbaОценок пока нет

- Principles of Engineering Economy: Analyze Costs & Maximize ProfitsДокумент4 страницыPrinciples of Engineering Economy: Analyze Costs & Maximize Profitsadamong99Оценок пока нет

- 6.3 Applying Annual-Worth Analysis 6.3.1 Benefits of AE AnalysisДокумент6 страниц6.3 Applying Annual-Worth Analysis 6.3.1 Benefits of AE Analysisshintya nadaОценок пока нет

- Replacement AnalysisДокумент34 страницыReplacement AnalysisShamsul AffendiОценок пока нет

- The Objective of Chapter 9 Is To Address The Question of Whether A Currently Owned Asset Should Be Kept in Service or Immediately ReplacedДокумент24 страницыThe Objective of Chapter 9 Is To Address The Question of Whether A Currently Owned Asset Should Be Kept in Service or Immediately ReplacedAykut YıldızОценок пока нет

- Asset Investment DecisionДокумент8 страницAsset Investment DecisionOnaderu Oluwagbenga EnochОценок пока нет

- Types of Replacement Policies:: Classification: InternalДокумент4 страницыTypes of Replacement Policies:: Classification: InternalCMОценок пока нет

- Replacement AnalysisДокумент18 страницReplacement AnalysisVishal MeenaОценок пока нет

- Life cycle costing for assetsДокумент19 страницLife cycle costing for assetsByamukama AsaphОценок пока нет

- Replacement and Maintenance AnalysisДокумент53 страницыReplacement and Maintenance AnalysisHimanshu MishraОценок пока нет

- Lecture NotesДокумент26 страницLecture NotesSAMSONIОценок пока нет

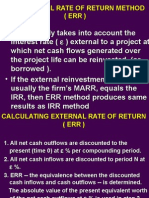

- CALCULATE EXTERNAL RATE OF RETURN (ERRДокумент19 страницCALCULATE EXTERNAL RATE OF RETURN (ERRJomer GiraoОценок пока нет

- DepreciationДокумент26 страницDepreciationBalu BalireddiОценок пока нет

- (Thesis) 2011 - The Technical Analysis Method of Moving Average Trading. Rules That Reduce The Number of Losing Trades - Marcus C. TomsДокумент185 страниц(Thesis) 2011 - The Technical Analysis Method of Moving Average Trading. Rules That Reduce The Number of Losing Trades - Marcus C. TomsFaridElAtracheОценок пока нет

- Vdocuments - MX - Blackbook Project On Mutual Funds PDFДокумент88 страницVdocuments - MX - Blackbook Project On Mutual Funds PDFAbu Sufiyan ShaikhОценок пока нет

- Abacus v. AmpilДокумент11 страницAbacus v. AmpilNylaОценок пока нет

- AHAP Insurance Financial SummaryДокумент2 страницыAHAP Insurance Financial SummaryluvzaelОценок пока нет

- Philippine Health Care Providers Dispute Over Documentary Stamp Tax AssessmentДокумент2 страницыPhilippine Health Care Providers Dispute Over Documentary Stamp Tax AssessmentGeralyn GabrielОценок пока нет

- Retail IndustryДокумент3 страницыRetail IndustryakavinashkillerОценок пока нет

- Financial MarketДокумент8 страницFinancial Marketindusekar83Оценок пока нет

- Accounting For Cash and Cash TransactionДокумент63 страницыAccounting For Cash and Cash TransactionAura Angela SeradaОценок пока нет

- Goods and Services Tax (GST) in IndiaДокумент30 страницGoods and Services Tax (GST) in IndiarupalОценок пока нет

- SOLMAN-CHAPTER-14-INVESTMENTS-IN-ASSOCIATES_IA-PART-1B_2020ed (3)Документ27 страницSOLMAN-CHAPTER-14-INVESTMENTS-IN-ASSOCIATES_IA-PART-1B_2020ed (3)Meeka CalimagОценок пока нет

- Ark Israel Innovative Technology Etf Izrl HoldingsДокумент2 страницыArk Israel Innovative Technology Etf Izrl HoldingsmikiОценок пока нет

- EF2A1 HDT Budget Upto Direct Taxes PCB4 1629376359978Документ30 страницEF2A1 HDT Budget Upto Direct Taxes PCB4 1629376359978Mamta Patel100% (1)

- St. Mary's Financial Accounting Comprehensive ExerciseДокумент5 страницSt. Mary's Financial Accounting Comprehensive ExerciseOrnet Studio100% (1)

- My - Invoice - 12 Jan 2023, 18 - 01 - 08Документ2 страницыMy - Invoice - 12 Jan 2023, 18 - 01 - 08Rohit Kumar DubeyОценок пока нет

- CPA Exam Questions on FASB Conceptual FrameworkДокумент26 страницCPA Exam Questions on FASB Conceptual FrameworkTerry GuОценок пока нет

- ACCA F7 Revision Mock June 2013 QUESTIONS Version 4 FINAL at 25 March 2013 PDFДокумент11 страницACCA F7 Revision Mock June 2013 QUESTIONS Version 4 FINAL at 25 March 2013 PDFPiyal HossainОценок пока нет

- Dvorak Mar 23Документ103 страницыDvorak Mar 23glimmertwins100% (1)

- Computation FY 18-19 PDFДокумент6 страницComputation FY 18-19 PDFRuch JainОценок пока нет

- ICE Cotton BrochureДокумент6 страницICE Cotton BrochureAmeya PagnisОценок пока нет

- Accounts - Past Years Que CompilationДокумент393 страницыAccounts - Past Years Que CompilationSavya SachiОценок пока нет

- Landbank RequirementsДокумент3 страницыLandbank Requirementsgee gambol50% (4)

- Pedro Santos' Transportation Business General Journal For The Month of JulyДокумент8 страницPedro Santos' Transportation Business General Journal For The Month of Julyლ itsmooncakes ́ლОценок пока нет

- A Case For Economic Democracy by Gary Dorrien - Tikkun Magazine PDFДокумент7 страницA Case For Economic Democracy by Gary Dorrien - Tikkun Magazine PDFMegan Jane JohnsonОценок пока нет

- Mobile Services Tax InvoiceДокумент3 страницыMobile Services Tax Invoicekumarvaibhav301745Оценок пока нет

- Entrepreneur Management Questions and AnswersДокумент24 страницыEntrepreneur Management Questions and AnswersArun DassiОценок пока нет

- Implementing Your Business PlanДокумент10 страницImplementing Your Business PlanGian Carlo Devera71% (7)

- Intercompany transactions elimination for consolidated financial statementsДокумент13 страницIntercompany transactions elimination for consolidated financial statementsicadeliciafebОценок пока нет

- ZF-02 Posting Credit Note SPPLДокумент10 страницZF-02 Posting Credit Note SPPLGhosh2Оценок пока нет

- OBLICON - Chapter 1 ProblemДокумент1 страницаOBLICON - Chapter 1 ProblemArahОценок пока нет