Вам также может понравиться

- BGMEA A. Member PDFДокумент10 страницBGMEA A. Member PDFzemid2kОценок пока нет

- IELTS Essay TemplateДокумент1 страницаIELTS Essay Templatezemid2k75% (4)

- IELTS Task 2Документ10 страницIELTS Task 2zemid2k100% (4)

- IeltsДокумент1 страницаIeltszemid2k100% (1)

- Dhaka TobacooДокумент1 страницаDhaka Tobacoozemid2kОценок пока нет

- Page No.: Chapter One: Introduction of The ReportДокумент2 страницыPage No.: Chapter One: Introduction of The Reportzemid2kОценок пока нет

- ItДокумент17 страницItzemid2kОценок пока нет

- P&GДокумент22 страницыP&Gzemid2k100% (1)

- Section One: Introduction: Table ofДокумент7 страницSection One: Introduction: Table ofzemid2kОценок пока нет

- CVДокумент2 страницыCVzemid2kОценок пока нет

- Chapter-01: Introduction of The ReportДокумент10 страницChapter-01: Introduction of The Reportzemid2kОценок пока нет

- Dealy Tution FeeДокумент1 страницаDealy Tution Feezemid2kОценок пока нет

- Subject: Application For The Post of "Management Trainee"Документ1 страницаSubject: Application For The Post of "Management Trainee"zemid2kОценок пока нет

- MISДокумент2 страницыMISzemid2k67% (3)

- InsuranceДокумент14 страницInsurancezemid2kОценок пока нет

- SourceДокумент26 страницSourcezemid2kОценок пока нет

- Green HouseДокумент18 страницGreen Housezemid2kОценок пока нет

- Dealy Tution FeeДокумент1 страницаDealy Tution Feezemid2kОценок пока нет

- AssignmentДокумент26 страницAssignmentzemid2kОценок пока нет

- Marketing CommunicationДокумент7 страницMarketing Communicationzemid2kОценок пока нет

- Compe Titive Analysis of YahooДокумент4 страницыCompe Titive Analysis of Yahoozemid2kОценок пока нет

- Term Paper For HRM 501Документ3 страницыTerm Paper For HRM 501zemid2kОценок пока нет

- CV of SaidulДокумент3 страницыCV of Saidulzemid2kОценок пока нет

- HRM 501 - Chapter1-2-5-6-7Документ20 страницHRM 501 - Chapter1-2-5-6-7zemid2kОценок пока нет

- Term PaperДокумент2 страницыTerm Paperzemid2kОценок пока нет

- GRAMEENPHONEДокумент3 страницыGRAMEENPHONEzemid2kОценок пока нет

- Promotion Is All About Companies Communicating With CustomersДокумент3 страницыPromotion Is All About Companies Communicating With Customerszemid2kОценок пока нет

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (120)

- Customers' Satisfaction Towards Automated Teller Machine: ManagementДокумент4 страницыCustomers' Satisfaction Towards Automated Teller Machine: ManagementmohitОценок пока нет

- Black BookДокумент86 страницBlack BookDilip AhirОценок пока нет

- Final Project: University of Central PunjabДокумент45 страницFinal Project: University of Central PunjabWaleed HayatОценок пока нет

- Yes Bank StatementДокумент6 страницYes Bank StatementApsra Group100% (1)

- Module 1: Introduction To Operating System: Need For An OSДокумент15 страницModule 1: Introduction To Operating System: Need For An OSDr Ramu KuchipudiОценок пока нет

- Comparative Analysis of Commercial Bank (Icici and Idbi Bank)Документ27 страницComparative Analysis of Commercial Bank (Icici and Idbi Bank)GUDDUОценок пока нет

- Internship Report On MCB Limited (1412) MultanДокумент36 страницInternship Report On MCB Limited (1412) MultanAbdul KareemОценок пока нет

- Chapter 3 AnalysisДокумент13 страницChapter 3 AnalysisLeo KingОценок пока нет

- Effect of Bank Innovations On Financial Performance of Commercial Banks in KenyaДокумент261 страницаEffect of Bank Innovations On Financial Performance of Commercial Banks in KenyaPearl MarketОценок пока нет

- ITTДокумент126 страницITTNishant WaniОценок пока нет

- UntitledДокумент78 страницUntitledSiddhesh YerunkarОценок пока нет

- A Thesis On Correlation Between Customer Services and Its Satisfaction Level in HDFC BankДокумент52 страницыA Thesis On Correlation Between Customer Services and Its Satisfaction Level in HDFC Bankbittu jain100% (1)

- Marketing Plan For YES AccountДокумент52 страницыMarketing Plan For YES AccountVame ApiОценок пока нет

- Chase Bank Statement TemplateДокумент6 страницChase Bank Statement TemplateADMIN HR100% (1)

- DN Series 100D Product CardДокумент2 страницыDN Series 100D Product CardLuis JuárezОценок пока нет

- ResumeДокумент2 страницыResumePriyanka Aryan100% (1)

- NCR Selfserv 26 Atm PBF GroupДокумент56 страницNCR Selfserv 26 Atm PBF GroupJose MarcosОценок пока нет

- Project On Punjab National BankДокумент84 страницыProject On Punjab National BankViPul81% (27)

- A Comparative Analysis Among Bank Interest Rates in Calamba City of LagunaДокумент7 страницA Comparative Analysis Among Bank Interest Rates in Calamba City of LagunaAmalia BalilinОценок пока нет

- Tutorial 2 - 3Документ2 страницыTutorial 2 - 3Ahan TejaswiОценок пока нет

- C. Rules of Adminissibility - Documentary Evidence - Best Evidence Rule - Loon Vs Power Master Inc, 712 SCRAДокумент1 страницаC. Rules of Adminissibility - Documentary Evidence - Best Evidence Rule - Loon Vs Power Master Inc, 712 SCRAJocelyn Yemyem Mantilla VelosoОценок пока нет

- Standard Chartered Bank FinalДокумент78 страницStandard Chartered Bank FinalHimanshu Saini0% (1)

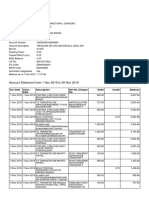

- Account Statement From 1 Nov 2019 To 30 Nov 2019: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceДокумент4 страницыAccount Statement From 1 Nov 2019 To 30 Nov 2019: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceChandru ChristurajОценок пока нет

- Charges & Fee - IDBI Bank Card Products: 1) Classic Debit Card/Women's Debit Card/Being Me Card/Kids CardДокумент5 страницCharges & Fee - IDBI Bank Card Products: 1) Classic Debit Card/Women's Debit Card/Being Me Card/Kids Cardrose thomsan thomsanОценок пока нет

- Help Manual For IOs Doing Inspection of Computerized Branches Updated Till 30th September 2008-1 PDFДокумент194 страницыHelp Manual For IOs Doing Inspection of Computerized Branches Updated Till 30th September 2008-1 PDFarpannathОценок пока нет

- Computer Science Project Topics and MaterialsДокумент38 страницComputer Science Project Topics and MaterialsEzekielОценок пока нет

- SCBLPДокумент18 страницSCBLPKamran Ali AbbasiОценок пока нет

- Modern Object-Oriented Software DevelopmentДокумент13 страницModern Object-Oriented Software DevelopmentNirmal PatleОценок пока нет

- How I Fired My Boss and Traveled For 13+ Years: Dan of Vagabond BuddhaДокумент38 страницHow I Fired My Boss and Traveled For 13+ Years: Dan of Vagabond BuddhaBob100% (1)

- Full Text Cases 81 To 100: TortsДокумент117 страницFull Text Cases 81 To 100: TortsLeeОценок пока нет