Вам также может понравиться

- Mary - Had - A - Little - Lamb Piece With DynamicsДокумент1 страницаMary - Had - A - Little - Lamb Piece With DynamicsJane Claire MagallanesОценок пока нет

- White Christmas - 8 - Acoustic GuitarДокумент1 страницаWhite Christmas - 8 - Acoustic GuitarJane Claire MagallanesОценок пока нет

- Ode To JoyДокумент2 страницыOde To JoyJane Claire MagallanesОценок пока нет

- White ChristmasДокумент1 страницаWhite ChristmasJane Claire MagallanesОценок пока нет

- Angels We Have Heard On HighДокумент1 страницаAngels We Have Heard On HighJane Claire MagallanesОценок пока нет

- You Are My All in All Canon Simplified - VioloncelloДокумент2 страницыYou Are My All in All Canon Simplified - VioloncelloJane Claire MagallanesОценок пока нет

- Angels We Have Heard On HighДокумент1 страницаAngels We Have Heard On HighJane Claire MagallanesОценок пока нет

- You Are My All in All Canon Simplified - Violin IIДокумент2 страницыYou Are My All in All Canon Simplified - Violin IIJane Claire MagallanesОценок пока нет

- Negotiable Instruments LawДокумент17 страницNegotiable Instruments LawJeffrey Ranes Doloriel Mendoza-Paasa100% (1)

- Carol of The BellsДокумент37 страницCarol of The BellsJane Claire Magallanes100% (1)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (890)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (265)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2219)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (119)

- Bankruptcy and ReorganizationДокумент13 страницBankruptcy and ReorganizationAnkita ChauhanОценок пока нет

- Financial Statement AnalysisДокумент2 страницыFinancial Statement AnalysisLJBernardoОценок пока нет

- 7 Intraday TricksДокумент15 страниц7 Intraday TricksAnonymous 5mSMeP2jОценок пока нет

- Lecture 3.1.2 - Equity CapitalДокумент34 страницыLecture 3.1.2 - Equity CapitalvaishnaviОценок пока нет

- Quiz For Financial StatementsДокумент4 страницыQuiz For Financial StatementsCherie Soriano AnanayoОценок пока нет

- Assignment # 5Документ6 страницAssignment # 5Muqaddas Zulfiqar100% (2)

- Investment DecisionДокумент6 страницInvestment DecisionAnonymous GywY2THОценок пока нет

- Accounting For Special Transactions and Business CombinationsДокумент3 страницыAccounting For Special Transactions and Business CombinationsJustine Reine CornicoОценок пока нет

- ValCom Syllabus BSMAДокумент14 страницValCom Syllabus BSMAMerel Rose FloresОценок пока нет

- FM Quiz ch1-3Документ7 страницFM Quiz ch1-3Noor SyuhaidaОценок пока нет

- FM - Dividend Policy and Dividend Decision Models (Cir 18.3.2020)Документ129 страницFM - Dividend Policy and Dividend Decision Models (Cir 18.3.2020)Rohit PanpatilОценок пока нет

- T-4 CRMДокумент26 страницT-4 CRMNamanОценок пока нет

- Fi3300 Chapter09Документ40 страницFi3300 Chapter09Yaru KamiОценок пока нет

- Session 3Документ90 страницSession 3Phuc Ho Nguyen MinhОценок пока нет

- AC15 Quiz 2Документ6 страницAC15 Quiz 2Kristine Esplana Toralde100% (1)

- Buffettology Sustainable GrowthДокумент12 страницBuffettology Sustainable GrowthLisa KrissОценок пока нет

- Intermediate Accounting 1&2 Quiz FinalsДокумент6 страницIntermediate Accounting 1&2 Quiz FinalsJohn ryan Del RosarioОценок пока нет

- Corporate and Other Laws: Ntermediate OurseДокумент181 страницаCorporate and Other Laws: Ntermediate Oursepriyal100% (1)

- Strategic Cost Management 2 Financial Analysis: Percentage Composition StatementsДокумент13 страницStrategic Cost Management 2 Financial Analysis: Percentage Composition StatementsAlexandra Nicole IsaacОценок пока нет

- Financial Reporting Solution Sr. No. Nature of Transaction Operating / Investing / Financing /not To Be ConsideredДокумент20 страницFinancial Reporting Solution Sr. No. Nature of Transaction Operating / Investing / Financing /not To Be ConsideredRITZ BROWNОценок пока нет

- Mobile App Manual PDFДокумент20 страницMobile App Manual PDFZaraki KenpachiОценок пока нет

- Questions On Trial Balance To StudentsДокумент6 страницQuestions On Trial Balance To Studentsveraji3735Оценок пока нет

- International Financial Management 13 Edition: by Jeff MaduraДокумент25 страницInternational Financial Management 13 Edition: by Jeff MaduraAbdulaziz Al-amroОценок пока нет

- Cash Flow and Financial PlanningДокумент64 страницыCash Flow and Financial PlanningKARL PASCUAОценок пока нет

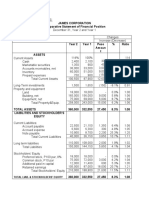

- Horizontal Analysis:: James Corporation Comparative Statement of Financial PositionДокумент7 страницHorizontal Analysis:: James Corporation Comparative Statement of Financial PositionJohn Francis IdananОценок пока нет

- Chapter-Four Financial InstrumentsДокумент15 страницChapter-Four Financial InstrumentsAbdiОценок пока нет

- 1.PDF Insolvency Law 10th EditionДокумент733 страницы1.PDF Insolvency Law 10th Editionliam.dalwai100% (1)

- FINE4016 Lecture Slides (Financial Statement Analysis I) 20170321 - Student VersionДокумент68 страницFINE4016 Lecture Slides (Financial Statement Analysis I) 20170321 - Student Versionjack100% (2)

- Seatwork Income MaДокумент3 страницыSeatwork Income MaJoyce Ann Agdippa Barcelona0% (1)

- ELEC2 - Module 3 - Liquidation Value MethodДокумент31 страницаELEC2 - Module 3 - Liquidation Value MethodMaricar PinedaОценок пока нет