Вам также может понравиться

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- GUARANTY NL - GT The Company, Liked GT The Stock, Unliked - Will The Asset Sensitive Balance Sheet and Growing Retail Exposure Hurt Earnings - Rolling Foward PT To FY13Документ9 страницGUARANTY NL - GT The Company, Liked GT The Stock, Unliked - Will The Asset Sensitive Balance Sheet and Growing Retail Exposure Hurt Earnings - Rolling Foward PT To FY13MukarangaОценок пока нет

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- DIAMOND NL - The Beauty of Ugly Part 2 - 1H12 Pleasing - Consistency Required To Restore ConvictionДокумент6 страницDIAMOND NL - The Beauty of Ugly Part 2 - 1H12 Pleasing - Consistency Required To Restore ConvictionMukarangaОценок пока нет

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- CPI SJ - Glittery Prospects Priced-In - FY13 TP R205 - HOLDДокумент17 страницCPI SJ - Glittery Prospects Priced-In - FY13 TP R205 - HOLDMukarangaОценок пока нет

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (894)

- RSA - Half Full or Half EmptyДокумент28 страницRSA - Half Full or Half EmptyMukarangaОценок пока нет

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- SSA Banks - Denial Is Futile - Short Term Risks But Long-Term OpportunitiesДокумент13 страницSSA Banks - Denial Is Futile - Short Term Risks But Long-Term OpportunitiesMukarangaОценок пока нет

- CPI SJ - A Critique On Credit Risks & ROE - Solid Footing But We Maintain Our HOLD On Valuation RiskДокумент16 страницCPI SJ - A Critique On Credit Risks & ROE - Solid Footing But We Maintain Our HOLD On Valuation RiskMukarangaОценок пока нет

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- Kenyan Banks - A Follow Up On Credit Risks As Investors Become Increasingly Concerned - Salient Features On Mortgage SectorДокумент9 страницKenyan Banks - A Follow Up On Credit Risks As Investors Become Increasingly Concerned - Salient Features On Mortgage SectorMukarangaОценок пока нет

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Kenyan Banks - Time To Be Selective - We Remain Concerned by Credit Risks - Despite Higher Cost of Deposist, Banks Managed To Expand Spreads - Rolling PTs To FY13Документ22 страницыKenyan Banks - Time To Be Selective - We Remain Concerned by Credit Risks - Despite Higher Cost of Deposist, Banks Managed To Expand Spreads - Rolling PTs To FY13MukarangaОценок пока нет

- Kenyan Banks - A Critique To System Credit Risks - System NPLs Defying Logic But Regulators Need To Mind The GapДокумент22 страницыKenyan Banks - A Critique To System Credit Risks - System NPLs Defying Logic But Regulators Need To Mind The GapMukarangaОценок пока нет

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (265)

- SSA Banks Nigeria Kenya UgandaДокумент14 страницSSA Banks Nigeria Kenya UgandaMukarangaОценок пока нет

- Nigerian Banks - Atonement, Redemption and Resurrection - BUY Zenith - Diamond - Access - GT - HOLD First - UBAДокумент87 страницNigerian Banks - Atonement, Redemption and Resurrection - BUY Zenith - Diamond - Access - GT - HOLD First - UBAMukarangaОценок пока нет

- SSA Banks Nigeria Kenya Uganda Deja VuДокумент13 страницSSA Banks Nigeria Kenya Uganda Deja VuMukarangaОценок пока нет

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Kenyan Banks - Could Equity Be A Victim of Its Own SuccessДокумент22 страницыKenyan Banks - Could Equity Be A Victim of Its Own SuccessMukarangaОценок пока нет

- Kenyan Banks - Anchor Themes - Regionalisation and Mortgage Lending - BUY KCB - SELL CoopДокумент62 страницыKenyan Banks - Anchor Themes - Regionalisation and Mortgage Lending - BUY KCB - SELL CoopMukarangaОценок пока нет

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- Ugandan Banks - BUY Stanbic - HOLD DFCUДокумент44 страницыUgandan Banks - BUY Stanbic - HOLD DFCUMukarangaОценок пока нет

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- Ugandan Banks - BUY Stanbic - HOLD DFCUДокумент44 страницыUgandan Banks - BUY Stanbic - HOLD DFCUMukarangaОценок пока нет

- Capitec Bank - Valuation Looks Steep But Growth Outlook Is The Differentiating Factor - FinalДокумент54 страницыCapitec Bank - Valuation Looks Steep But Growth Outlook Is The Differentiating Factor - FinalMukarangaОценок пока нет

- ABIL - Reiterate Our SELL - Improving But Lags Our ExpectationsДокумент7 страницABIL - Reiterate Our SELL - Improving But Lags Our ExpectationsMukarangaОценок пока нет

- ABIL - Non-Retail Deposit Taking Strategy Clouds Long Term Growth Outlook - Initiating With A HOLDДокумент56 страницABIL - Non-Retail Deposit Taking Strategy Clouds Long Term Growth Outlook - Initiating With A HOLDMukarangaОценок пока нет

- ABIL - Non-Retail Deposit Taking Strategy Clouds Long Term Growth Outlook - Initiating With A HOLDДокумент56 страницABIL - Non-Retail Deposit Taking Strategy Clouds Long Term Growth Outlook - Initiating With A HOLDMukarangaОценок пока нет

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- RSA 2009 OutlookДокумент43 страницыRSA 2009 OutlookMukarangaОценок пока нет

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2219)

- Stanbic Uganda - SBU - Ug 1H09Документ9 страницStanbic Uganda - SBU - Ug 1H09MukarangaОценок пока нет

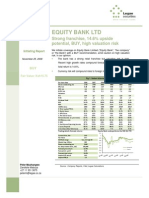

- Equity Bank Limited - Strong Franchise, 14.6% Potential Upsiide, BUY, High Valuation Risk2Документ40 страницEquity Bank Limited - Strong Franchise, 14.6% Potential Upsiide, BUY, High Valuation Risk2MukarangaОценок пока нет

- SBU - Ug - Reiteration of BUY - Potential Return 27%Документ6 страницSBU - Ug - Reiteration of BUY - Potential Return 27%MukarangaОценок пока нет

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- Zimbabwe - A Growth RecessionДокумент17 страницZimbabwe - A Growth RecessionMukarangaОценок пока нет

- Kenya - Equities Ripe For A ReboundДокумент15 страницKenya - Equities Ripe For A ReboundMukarangaОценок пока нет

- SSA Frontier Markets - Nov 5 2009)Документ34 страницыSSA Frontier Markets - Nov 5 2009)MukarangaОценок пока нет

- Max232 DatasheetДокумент9 страницMax232 DatasheetprincebahariОценок пока нет

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (119)

- Titan Case StudyДокумент14 страницTitan Case StudySaurabh SinghОценок пока нет

- AWS Compete: Microsoft's Response to AWSДокумент6 страницAWS Compete: Microsoft's Response to AWSSalman AslamОценок пока нет

- Reporting Outline (Group4 12 Abm1)Документ3 страницыReporting Outline (Group4 12 Abm1)Rafaelto D. Atangan Jr.Оценок пока нет

- Det Syll Divisional Accountant Item No 19Документ2 страницыDet Syll Divisional Accountant Item No 19tinaantonyОценок пока нет

- Gestion de La Calidad HoqДокумент8 страницGestion de La Calidad HoqLuisa AngelОценок пока нет

- Module 2 - Extra Practice Questions With SolutionsДокумент3 страницыModule 2 - Extra Practice Questions With SolutionsYatin WaliaОценок пока нет

- H4 Swing SetupДокумент19 страницH4 Swing SetupEric Woon Kim ThakОценок пока нет

- Sending DDDDWith Multiple Tabs of Excel As A Single Attachment in ABAPДокумент4 страницыSending DDDDWith Multiple Tabs of Excel As A Single Attachment in ABAPKumar Krishna KumarОценок пока нет

- India's Infosys: A Case Study For Attaining Both Ethical Excellence and Business Success in A Developing CountryДокумент3 страницыIndia's Infosys: A Case Study For Attaining Both Ethical Excellence and Business Success in A Developing CountrypritamashwaniОценок пока нет

- PNV-08 Employer's Claims PDFДокумент1 страницаPNV-08 Employer's Claims PDFNatarajan SaravananОценок пока нет

- Customer Satisfaction Report on Peaks AutomobilesДокумент72 страницыCustomer Satisfaction Report on Peaks AutomobilesHarmeet SinghОценок пока нет

- PsychographicsДокумент12 страницPsychographicsirenek100% (2)

- 1 - Impact of Career Development On Employee Satisfaction in Private Banking Sector Karachi - 2Документ8 страниц1 - Impact of Career Development On Employee Satisfaction in Private Banking Sector Karachi - 2Mirza KapalОценок пока нет

- MD - Nasir Uddin CVДокумент4 страницыMD - Nasir Uddin CVশুভবর্ণОценок пока нет

- Green Supply Chain Management PDFДокумент18 страницGreen Supply Chain Management PDFMaazОценок пока нет

- 1 MDL299356Документ4 страницы1 MDL299356Humayun NawazОценок пока нет

- Employee Suggestion Programs Save MoneyДокумент3 страницыEmployee Suggestion Programs Save Moneyimran27pk100% (1)

- Money ClaimДокумент1 страницаMoney Claimalexander ongkiatcoОценок пока нет

- Principles of Managerial Finance Brief 6Th Edition Gitman Test Bank Full Chapter PDFДокумент58 страницPrinciples of Managerial Finance Brief 6Th Edition Gitman Test Bank Full Chapter PDFdebbiemitchellgpjycemtsx100% (10)

- English For Hotel-1-1Документ17 страницEnglish For Hotel-1-1AQilla ZaraОценок пока нет

- TCS Connected Universe Platform - 060918Документ4 страницыTCS Connected Universe Platform - 060918abhishek tripathyОценок пока нет

- How industrial engineering can optimize mining operationsДокумент6 страницHow industrial engineering can optimize mining operationsAlejandro SanchezОценок пока нет

- Class 11 CH 2 NotesДокумент10 страницClass 11 CH 2 NotesJay KakadiyaОценок пока нет

- Motorcycle Industry Draft Report Final VersionДокумент60 страницMotorcycle Industry Draft Report Final VersionMuneer Gurmani0% (1)

- Appendix - Structural Vetting ProjectsДокумент37 страницAppendix - Structural Vetting Projectsqsultan100% (1)

- Sap CloudДокумент29 страницSap CloudjagankilariОценок пока нет

- Chapter1 - Fundamental Principles of ValuationДокумент21 страницаChapter1 - Fundamental Principles of ValuationだみОценок пока нет

- Oracle ACE WPДокумент23 страницыOracle ACE WPSyed Fahad KhanОценок пока нет

- Financial Consultant Excel SkillsДокумент1 страницаFinancial Consultant Excel SkillsOlgaОценок пока нет