Вам также может понравиться

- Woolf: Vermont Family Characteristics by CountyДокумент1 страницаWoolf: Vermont Family Characteristics by CountyPhilip TortoraОценок пока нет

- Bernie Sanders Medical ReportДокумент1 страницаBernie Sanders Medical ReportPhilip TortoraОценок пока нет

- Woolf: Inflation-Adjusted Spending Per Vermont PupilДокумент1 страницаWoolf: Inflation-Adjusted Spending Per Vermont PupilPhilip TortoraОценок пока нет

- Woolf: Number of Vermont Married CouplesДокумент1 страницаWoolf: Number of Vermont Married CouplesPhilip TortoraОценок пока нет

- Quinnipiac Presidential PollДокумент9 страницQuinnipiac Presidential PollPhilip TortoraОценок пока нет

- Woolf: Initial Claims For Unemployment InsuranceДокумент1 страницаWoolf: Initial Claims For Unemployment InsurancePhilip TortoraОценок пока нет

- Woolf: Vermont Labor Force and JobsДокумент1 страницаWoolf: Vermont Labor Force and JobsPhilip TortoraОценок пока нет

- Woolf: Vermont Median Family Income Jan 2016Документ1 страницаWoolf: Vermont Median Family Income Jan 2016Philip TortoraОценок пока нет

- Woolf: Vermont Earned Income Tax CreditДокумент1 страницаWoolf: Vermont Earned Income Tax CreditPhilip TortoraОценок пока нет

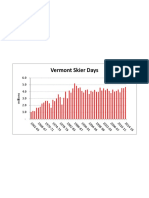

- Woolf: Vermont Skier DaysДокумент1 страницаWoolf: Vermont Skier DaysPhilip TortoraОценок пока нет

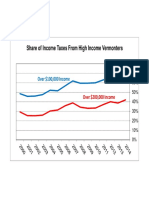

- Woolf: Share of Income Taxes From High Income VermontersДокумент1 страницаWoolf: Share of Income Taxes From High Income VermontersPhilip TortoraОценок пока нет

- Woolf: Vermont Gasoline and Fuel Oil PricesДокумент1 страницаWoolf: Vermont Gasoline and Fuel Oil PricesPhilip TortoraОценок пока нет

- November 2012 Vaughan Real Estate Market UpdateДокумент5 страницNovember 2012 Vaughan Real Estate Market Updateinfo7761Оценок пока нет

- Woolf: Vermont Labor Force & JobsДокумент1 страницаWoolf: Vermont Labor Force & JobsPhilip TortoraОценок пока нет

- PDF: Northfield Fatal Fire Search Warrant ApplicationДокумент10 страницPDF: Northfield Fatal Fire Search Warrant ApplicationPhilip TortoraОценок пока нет

- Woolf: Vermont Media Income by Household TypeДокумент1 страницаWoolf: Vermont Media Income by Household TypePhilip TortoraОценок пока нет

- Woolf: Vermont PopulationДокумент1 страницаWoolf: Vermont PopulationPhilip TortoraОценок пока нет

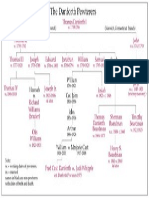

- The Danforth PewterersДокумент1 страницаThe Danforth PewterersPhilip TortoraОценок пока нет

- Woolf: Keurig Green Mountain Stock PriceДокумент1 страницаWoolf: Keurig Green Mountain Stock PricePhilip TortoraОценок пока нет

- Affidavit: United States vs. Mark McLoudДокумент9 страницAffidavit: United States vs. Mark McLoudPhilip TortoraОценок пока нет

- Art Woolf: FY12 Vermont Government SpendingДокумент1 страницаArt Woolf: FY12 Vermont Government SpendingPhilip TortoraОценок пока нет

- Art Woolf: Percentage of Students Achieving A Score of Proficient or AdvancedДокумент1 страницаArt Woolf: Percentage of Students Achieving A Score of Proficient or AdvancedPhilip TortoraОценок пока нет

- Art Woolf: Vermont Construction EmploymentДокумент1 страницаArt Woolf: Vermont Construction EmploymentPhilip TortoraОценок пока нет

- Art Woolf: State and Local Taxes As A Share of Personal IncomeДокумент1 страницаArt Woolf: State and Local Taxes As A Share of Personal IncomePhilip TortoraОценок пока нет

- Art Woolf: Vermont Percent of Under 65 Population Without Health InsuranceДокумент1 страницаArt Woolf: Vermont Percent of Under 65 Population Without Health InsurancePhilip TortoraОценок пока нет

- PDF: Court Papers Filed in Randy Quaid CaseДокумент18 страницPDF: Court Papers Filed in Randy Quaid CasePhilip TortoraОценок пока нет

- PDF: Court Papers Filed in Evi Quaid CaseДокумент23 страницыPDF: Court Papers Filed in Evi Quaid CasePhilip TortoraОценок пока нет

- Art Woolf: Vermont Payroll EmploymentДокумент1 страницаArt Woolf: Vermont Payroll EmploymentPhilip TortoraОценок пока нет

- Art Woolf: Vermont Employment Change Since RecessionДокумент1 страницаArt Woolf: Vermont Employment Change Since RecessionPhilip TortoraОценок пока нет

- Vermont State Police AMBER Alert ReviewДокумент5 страницVermont State Police AMBER Alert ReviewPhilip TortoraОценок пока нет

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5782)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (119)

- Motion To Quash Indictments Because Judge Oldner's Cumulative Actions Compromised The Integrity of The Indictment ProcessДокумент22 страницыMotion To Quash Indictments Because Judge Oldner's Cumulative Actions Compromised The Integrity of The Indictment ProcessThe Dallas Morning News100% (1)

- Sales Harrison Motors To Moles Vs IacДокумент4 страницыSales Harrison Motors To Moles Vs IacMariaAyraCelinaBatacanОценок пока нет

- Syllabus For Persons and Family Relations 2019 PDFДокумент6 страницSyllabus For Persons and Family Relations 2019 PDFLara Michelle Sanday BinudinОценок пока нет

- Municipal Ordinance No. 94-131Документ2 страницыMunicipal Ordinance No. 94-131Aryl LyraОценок пока нет

- MEC Withdrawal Transfer PDFДокумент2 страницыMEC Withdrawal Transfer PDFAnonymous K1z4NbxОценок пока нет

- Sample Board ResolutionДокумент4 страницыSample Board Resolution33215687955486% (37)

- Double TaxationДокумент5 страницDouble TaxationVidousha BoodanОценок пока нет

- Medicaid Services Manual Complete PDFДокумент1 788 страницMedicaid Services Manual Complete PDFGustavo AguirreОценок пока нет

- Gamboa Vs Teves 2011Документ3 страницыGamboa Vs Teves 2011Teoti Navarro ReyesОценок пока нет

- ELEM0313ra CebuДокумент151 страницаELEM0313ra CebuTheSummitExpressОценок пока нет

- Revised Administrative Order 79-2 11th CircuitДокумент4 страницыRevised Administrative Order 79-2 11th CircuitJudgeHSОценок пока нет

- Joseph Valverde Decision Letter PDFДокумент17 страницJoseph Valverde Decision Letter PDFMichael_Lee_RobertsОценок пока нет

- Indonesia Police OrganizationДокумент3 страницыIndonesia Police OrganizationRoyceezee AmvОценок пока нет

- Impact of The The Companies Act 2016 On Winding UpДокумент11 страницImpact of The The Companies Act 2016 On Winding UpAini RoslieОценок пока нет

- Chan-Tan v. Chan PDFДокумент17 страницChan-Tan v. Chan PDFCelina GonzalesОценок пока нет

- THOM v. BALTIMORE TRUST CO.Документ2 страницыTHOM v. BALTIMORE TRUST CO.Karen Selina AquinoОценок пока нет

- Indemnification AgreementДокумент6 страницIndemnification AgreementsalmanОценок пока нет

- Greece ECHR Ruling on Expat Voting RightsДокумент19 страницGreece ECHR Ruling on Expat Voting Rightsmcqueen2007Оценок пока нет

- Franchise Agreement for Gold Coin and Jewelry SalesДокумент14 страницFranchise Agreement for Gold Coin and Jewelry SalesKnowledge GuruОценок пока нет

- Corporation Code essentialsДокумент31 страницаCorporation Code essentialsJanette Sumagaysay100% (1)

- Malaysian Business Law Final AssessmentДокумент4 страницыMalaysian Business Law Final AssessmentRaihah Nabilah HashimОценок пока нет

- SC upholds acquittal of man charged with attempted rapeДокумент3 страницыSC upholds acquittal of man charged with attempted rapemaprecc07Оценок пока нет

- Ex-NASA Scientist Sues HPDДокумент10 страницEx-NASA Scientist Sues HPDHouston ChronicleОценок пока нет

- University of The Philippines College of LawДокумент12 страницUniversity of The Philippines College of LawLuis PerezОценок пока нет

- Bautista v. GonzalesДокумент16 страницBautista v. GonzalesKarl PunzalОценок пока нет

- Robert D. Quirk v. United States of America, Samuel Goldstein v. United States, 250 F.2d 909, 1st Cir. (1958)Документ4 страницыRobert D. Quirk v. United States of America, Samuel Goldstein v. United States, 250 F.2d 909, 1st Cir. (1958)Scribd Government DocsОценок пока нет

- Constitutional CommissionДокумент18 страницConstitutional Commissionsuperman6252100% (1)

- United States v. Edward Cardona, 903 F.2d 60, 1st Cir. (1990)Документ24 страницыUnited States v. Edward Cardona, 903 F.2d 60, 1st Cir. (1990)Scribd Government DocsОценок пока нет

- People vs. DansicoДокумент4 страницыPeople vs. DansicoPaolo MendioroОценок пока нет

- P1-MANILA TRADING & SUPPLY CO V MEDINA PDFДокумент3 страницыP1-MANILA TRADING & SUPPLY CO V MEDINA PDFKaye RodriguezОценок пока нет