Вам также может понравиться

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (120)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- Answer and CounterclaimДокумент86 страницAnswer and Counterclaimthe kingfishОценок пока нет

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Tata Case SolutionДокумент10 страницTata Case Solutionshantanu_malviya_1100% (1)

- Dak Complaint WMДокумент15 страницDak Complaint WMthe kingfish100% (1)

- Dak Complaint WMДокумент15 страницDak Complaint WMthe kingfish100% (1)

- Altman Z, Messod Beneish M, Piotroski F-ScoresДокумент4 страницыAltman Z, Messod Beneish M, Piotroski F-ScoresInternational Journal in Management Research and Social ScienceОценок пока нет

- IB Economics IA SampleДокумент26 страницIB Economics IA SampleYeşim Eylül ÇimenciОценок пока нет

- Ichimoku Charting UBS FORMATIONДокумент19 страницIchimoku Charting UBS FORMATIONemerzak100% (4)

- Karissa Bowley MotionДокумент4 страницыKarissa Bowley Motionaswarren77Оценок пока нет

- File Stamped Louisiana v. U.S. Dept of Education Title IXДокумент43 страницыFile Stamped Louisiana v. U.S. Dept of Education Title IXthe kingfishОценок пока нет

- Mabil FileДокумент30 страницMabil Filethe kingfishОценок пока нет

- Hale, Ronnie - Grat LustДокумент2 страницыHale, Ronnie - Grat Lustthe kingfish100% (1)

- Mabil FileДокумент30 страницMabil Filethe kingfishОценок пока нет

- Dau Mabil 18 DPS Motion To DismissДокумент9 страницDau Mabil 18 DPS Motion To Dismissthe kingfishОценок пока нет

- BlackRock Inc., Et Al.Документ33 страницыBlackRock Inc., Et Al.the kingfishОценок пока нет

- Wanted 4-9-24Документ2 страницыWanted 4-9-24the kingfishОценок пока нет

- Biggart Gilmer ComplaintДокумент2 страницыBiggart Gilmer Complaintthe kingfishОценок пока нет

- Wilson - Shaken Baby AbuseДокумент2 страницыWilson - Shaken Baby Abusethe kingfishОценок пока нет

- Peoples CompllaintДокумент33 страницыPeoples Compllaintthe kingfishОценок пока нет

- Floyd Jacobs FileДокумент23 страницыFloyd Jacobs Filethe kingfishОценок пока нет

- Mabil WM TRO RequestДокумент3 страницыMabil WM TRO Requestthe kingfish100% (1)

- Press Release Update NAME CORRECTION Ridgecrest HomicideДокумент3 страницыPress Release Update NAME CORRECTION Ridgecrest Homicidethe kingfishОценок пока нет

- Rapid Edited 1Документ8 страницRapid Edited 1the kingfishОценок пока нет

- RDI Contract, 2024.03.12Документ40 страницRDI Contract, 2024.03.12the kingfish100% (1)

- Ivana Fis File RedactedДокумент14 страницIvana Fis File Redactedthe kingfishОценок пока нет

- Where Is All The Money Going - An Analysis of Inside and Outside The Classroom Education SpendingДокумент6 страницWhere Is All The Money Going - An Analysis of Inside and Outside The Classroom Education Spendingthe kingfishОценок пока нет

- Bennett Charles Polic ReportДокумент6 страницBennett Charles Polic Reportthe kingfishОценок пока нет

- Angelique Arrest Report RecordДокумент2 страницыAngelique Arrest Report Recordthe kingfishОценок пока нет

- Most WantedДокумент2 страницыMost Wantedthe kingfishОценок пока нет

- Ivana Fis File - RedactedДокумент14 страницIvana Fis File - Redactedthe kingfishОценок пока нет

- Floyd Jacobs FileДокумент23 страницыFloyd Jacobs Filethe kingfishОценок пока нет

- 828 Sports Ventures Overview - Gluckstadt WMДокумент9 страниц828 Sports Ventures Overview - Gluckstadt WMthe kingfishОценок пока нет

- NAACP Reeves OpinionДокумент3 страницыNAACP Reeves Opinionthe kingfishОценок пока нет

- Committee Chairs Announcement 1.12.2024Документ2 страницыCommittee Chairs Announcement 1.12.2024the kingfish100% (1)

- Interim OrderДокумент6 страницInterim Orderthe kingfishОценок пока нет

- Chapter 13Документ13 страницChapter 13Haseeb Ahmed ShaikhОценок пока нет

- Assignment 3 - Financial MarketsДокумент4 страницыAssignment 3 - Financial MarketsToni MarquezОценок пока нет

- Complete Trading Journal For ShareДокумент3 страницыComplete Trading Journal For ShareHaslina Mohd SallehОценок пока нет

- Fins2624 Problem Set 5 Tutorial QuestionДокумент5 страницFins2624 Problem Set 5 Tutorial QuestionPhebieon MukwenhaОценок пока нет

- Finance Modeling Handbook (00000002)Документ1 страницаFinance Modeling Handbook (00000002)baronfgfОценок пока нет

- Assignment On BaringsДокумент10 страницAssignment On Baringsimtehan_chowdhuryОценок пока нет

- Global Capital Market NotesДокумент10 страницGlobal Capital Market NotesAbdulrahman AlotaibiОценок пока нет

- Market Analysis Feb 2024Документ17 страницMarket Analysis Feb 2024Subba TОценок пока нет

- 2010 07 06 - 010528 - Byp1 4Документ3 страницы2010 07 06 - 010528 - Byp1 4Muhammad RamadhanОценок пока нет

- Kinross Gold Corporation: Institutional Equity Research Intraday NoteДокумент6 страницKinross Gold Corporation: Institutional Equity Research Intraday NoteAvi CohenОценок пока нет

- Kanchan YadavДокумент14 страницKanchan YadavNandini JaganОценок пока нет

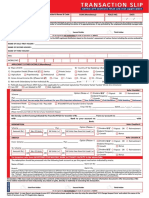

- Kotak - Transaction SlipДокумент2 страницыKotak - Transaction SlipJephiasОценок пока нет

- Enhanced Gis Revised v.2013 092513Документ9 страницEnhanced Gis Revised v.2013 092513itsmichikoОценок пока нет

- Activity 5 Non Current Assets Held For Sale and Discontinued OperationsДокумент3 страницыActivity 5 Non Current Assets Held For Sale and Discontinued Operationsnglc srzОценок пока нет

- Depreciation Is A Term Used Reference To TheДокумент14 страницDepreciation Is A Term Used Reference To TheMuzammil IqbalОценок пока нет

- PDFДокумент40 страницPDFAnonymous kvZykMivОценок пока нет

- Money Supply: Economics ProjectДокумент9 страницMoney Supply: Economics ProjectabhimussoorieОценок пока нет

- International Acc Quizlet No7Документ3 страницыInternational Acc Quizlet No7수지Оценок пока нет

- Bom Unit-3Документ89 страницBom Unit-3Mr. animeweedОценок пока нет

- Pom NotesДокумент6 страницPom NotesJanisha RadazaОценок пока нет

- E. Market Size PotentialДокумент4 страницыE. Market Size Potentialmesadaeterjohn.studentОценок пока нет

- FRM CaseДокумент14 страницFRM CaseKevval BorichaОценок пока нет

- UT Dallas Syllabus For Fin6316.001.11s Taught by David Springate (Spring8)Документ7 страницUT Dallas Syllabus For Fin6316.001.11s Taught by David Springate (Spring8)UT Dallas Provost's Technology GroupОценок пока нет

- Overview of Non-Bank Financial Institute of BangladeshДокумент7 страницOverview of Non-Bank Financial Institute of BangladeshSakib AhmedОценок пока нет

- What Are The Functions, Attributes And, Kinds of MoneyДокумент2 страницыWhat Are The Functions, Attributes And, Kinds of MoneyAngelie JalandoniОценок пока нет

- CHAPTER 5 - Portfolio TheoryДокумент58 страницCHAPTER 5 - Portfolio TheoryKabutu ChuungaОценок пока нет