Вам также может понравиться

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- People V JP Morgan ComplaintДокумент31 страницаPeople V JP Morgan ComplaintJames EdwardsОценок пока нет

- SSRN Id2023011Документ54 страницыSSRN Id2023011sterkejanОценок пока нет

- TBP Conf Oct 2012Документ27 страницTBP Conf Oct 2012annawitkowski88Оценок пока нет

- Single SlideДокумент1 страницаSingle Slideannawitkowski88Оценок пока нет

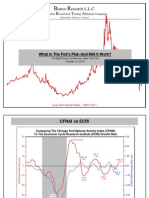

- Ianco Esearch L.L.C. A R T A: What Is The Fed's Plan and Will It Work?Документ44 страницыIanco Esearch L.L.C. A R T A: What Is The Fed's Plan and Will It Work?annawitkowski88Оценок пока нет

- Taxes and The EconomyДокумент23 страницыTaxes and The Economychristian_trejbal100% (1)

- Exhibit 15 - Whistleblower Affidavit (Redacted)Документ11 страницExhibit 15 - Whistleblower Affidavit (Redacted)annawitkowski88Оценок пока нет

- Research Division: Federal Reserve Bank of St. LouisДокумент43 страницыResearch Division: Federal Reserve Bank of St. Louisannawitkowski88Оценок пока нет

- Richmond Fed Research Digest: Frictional Wage Dispersion in Search Models: A Quantitative AssessmentДокумент11 страницRichmond Fed Research Digest: Frictional Wage Dispersion in Search Models: A Quantitative Assessmentannawitkowski88Оценок пока нет

- Fed SideДокумент1 страницаFed Sideannawitkowski88Оценок пока нет

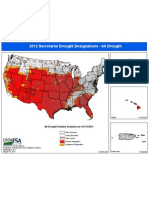

- Usda Drought Fast Track Designations 081512Документ1 страницаUsda Drought Fast Track Designations 081512annawitkowski88Оценок пока нет

- The Boom and Bust of U.S. Housing Prices From Various Geographic PerspectivesДокумент29 страницThe Boom and Bust of U.S. Housing Prices From Various Geographic Perspectivesannawitkowski88Оценок пока нет

- Income, Poverty, and Health Insurance Coverage in The United States: 2011Документ89 страницIncome, Poverty, and Health Insurance Coverage in The United States: 2011annawitkowski88Оценок пока нет

- Income, Poverty, and Health Insurance Coverage in The United States: 2011Документ89 страницIncome, Poverty, and Health Insurance Coverage in The United States: 2011annawitkowski88Оценок пока нет

- Woodford Rules Jackson Hole WyomingДокумент97 страницWoodford Rules Jackson Hole WyominglatecircleОценок пока нет

- Finance and Economics Discussion Series Divisions of Research & Statistics and Monetary Affairs Federal Reserve Board, Washington, D.CДокумент36 страницFinance and Economics Discussion Series Divisions of Research & Statistics and Monetary Affairs Federal Reserve Board, Washington, D.Cannawitkowski88Оценок пока нет

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5795)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (345)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1091)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- DeloitteConsulting - Nancy Singhal ResumeДокумент4 страницыDeloitteConsulting - Nancy Singhal ResumeHemant BharadwajОценок пока нет

- Advanced Control System by N.D.prasadДокумент26 страницAdvanced Control System by N.D.prasadAshish IndarapuОценок пока нет

- Engine Start Button E46 MANUALДокумент6 страницEngine Start Button E46 MANUALBilly GeorgiouОценок пока нет

- Photos - MV. Bahtera CemerlangДокумент46 страницPhotos - MV. Bahtera CemerlangEka Prasetya NugrahaОценок пока нет

- PEMA Practical Observations - Rail Mounted Crane InterfacesДокумент26 страницPEMA Practical Observations - Rail Mounted Crane InterfacesShaiju Narayanan100% (1)

- TLC Pharmaceutical Standards: Safety Data SheetДокумент4 страницыTLC Pharmaceutical Standards: Safety Data SheetFABIOLA FLOОценок пока нет

- Listing of SecuritiesДокумент5 страницListing of SecuritiesticktacktoeОценок пока нет

- Pink and White PresentationДокумент25 страницPink and White PresentationAngela María SarmientoОценок пока нет

- PBL Marketing Rahul YadavДокумент8 страницPBL Marketing Rahul YadavVIVEKANAND MISHRAОценок пока нет

- PSTC-Appendix C - Cleaning Test SurfacesДокумент4 страницыPSTC-Appendix C - Cleaning Test SurfacesChung LeОценок пока нет

- DecoderДокумент7 страницDecodervaani munjalОценок пока нет

- Compiler Design - 2Документ104 страницыCompiler Design - 2jemal12174Оценок пока нет

- Chapter - 1: Richard GersterДокумент80 страницChapter - 1: Richard GersterSanjay ShankpalОценок пока нет

- Python in A Nutshell: Python's Whys & HowsДокумент4 страницыPython in A Nutshell: Python's Whys & Howstvboxsmart newОценок пока нет

- MACFOS Investors-PresentationДокумент29 страницMACFOS Investors-PresentationIDEasОценок пока нет

- 5 1 5 PDFДокумент376 страниц5 1 5 PDFSaransh KejriwalОценок пока нет

- Autodesk 2015 Products Direct Download LinksДокумент2 страницыAutodesk 2015 Products Direct Download LinksALEXОценок пока нет

- Designing Data Analysis ProcedureДокумент15 страницDesigning Data Analysis ProcedureShadowStorm X3GОценок пока нет

- TextДокумент2 страницыTextArron LuОценок пока нет

- Struts 2 InterceptorsДокумент14 страницStruts 2 InterceptorsRamasamy GoОценок пока нет

- B C21 2019 IGC1 Element 2 How Health and Safety Management Systems V3 WMДокумент38 страницB C21 2019 IGC1 Element 2 How Health and Safety Management Systems V3 WMMecif Salah eddineОценок пока нет

- G11 W8 The Consequences of My ActionsДокумент3 страницыG11 W8 The Consequences of My Actionslyka garciaОценок пока нет

- Midterm: Mathematics For Engineers (W2021)Документ5 страницMidterm: Mathematics For Engineers (W2021)spppppОценок пока нет

- Audit Quality and Audit Firm ReputationДокумент10 страницAudit Quality and Audit Firm ReputationEdosa Joshua AronmwanОценок пока нет

- Dezurik Cast Stainless Steel Knife Gate Valves KGN RSB KGN Msu KGN RSB Resilient Seated Technical 29-00-1dДокумент8 страницDezurik Cast Stainless Steel Knife Gate Valves KGN RSB KGN Msu KGN RSB Resilient Seated Technical 29-00-1dOleg ShkolnikОценок пока нет

- NR # 2484B 08.03.2011 - B - Probe On Government's Tenement Housing Program PushedДокумент1 страницаNR # 2484B 08.03.2011 - B - Probe On Government's Tenement Housing Program Pushedpribhor2Оценок пока нет

- L - 043 - Weekly Report - LiwaДокумент84 страницыL - 043 - Weekly Report - LiwaMahmoudОценок пока нет

- Module 2 - Govt GrantДокумент4 страницыModule 2 - Govt GrantLui100% (1)

- 264 752 Bohlender Graebener Neo8s Spec SheetДокумент3 страницы264 752 Bohlender Graebener Neo8s Spec SheetCarlОценок пока нет

- Report HRTP Sanofi PakistanДокумент13 страницReport HRTP Sanofi PakistanANUS AHMED KHANОценок пока нет