Вам также может понравиться

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Taurus PPT'Документ8 страницTaurus PPT'Daniel ShettyОценок пока нет

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5795)

- Project TaxationДокумент37 страницProject TaxationDaniel ShettyОценок пока нет

- Audit of BankДокумент37 страницAudit of BankDaniel ShettyОценок пока нет

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- Dear Friends: Hojaye, Cocacola ENJOY" (WahateverДокумент6 страницDear Friends: Hojaye, Cocacola ENJOY" (WahateverDaniel ShettyОценок пока нет

- Koenigs EggДокумент7 страницKoenigs EggDaniel ShettyОценок пока нет

- S. M. SavariДокумент36 страницS. M. SavariDaniel ShettyОценок пока нет

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- 6th Central Pay Commission Salary CalculatorДокумент15 страниц6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- Strategic Management of SubwayДокумент6 страницStrategic Management of SubwayDaniel ShettyОценок пока нет

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Allen SollyДокумент9 страницAllen SollyDaniel Shetty100% (1)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

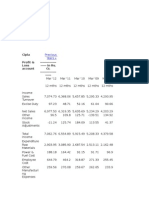

- Cipla Profit & Loss Account - in Rs. Cr.Документ3 страницыCipla Profit & Loss Account - in Rs. Cr.Daniel ShettyОценок пока нет

- StorytellingДокумент13 страницStorytellingDaniel ShettyОценок пока нет

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (345)

- FYP Indian Pharmaceutical IndustryДокумент37 страницFYP Indian Pharmaceutical IndustryDaniel ShettyОценок пока нет

- Sahil Mehmood Hussain Sayyad,: Kestone Intergrated Marketing Services Pvt. LTDДокумент1 страницаSahil Mehmood Hussain Sayyad,: Kestone Intergrated Marketing Services Pvt. LTDDaniel ShettyОценок пока нет

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- Pas 1Документ52 страницыPas 1Justine VeralloОценок пока нет

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- 2018 Za (Q + Ma) Ac1025Документ95 страниц2018 Za (Q + Ma) Ac1025전민건Оценок пока нет

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- Concept Questions: Chapter Twelve The Analysis of Growth and Sustainable EarningsДокумент64 страницыConcept Questions: Chapter Twelve The Analysis of Growth and Sustainable EarningsceojiОценок пока нет

- Feasibility StudyДокумент6 страницFeasibility Studyetc23Оценок пока нет

- Annual Report 2019 2020Документ208 страницAnnual Report 2019 2020bhalaОценок пока нет

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- Philippine Taxation Encyclopedia Third Release 2019 - 01Документ173 страницыPhilippine Taxation Encyclopedia Third Release 2019 - 01Patricia Arpilleda100% (1)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Cash Flow Statement - Indirect MethodДокумент5 страницCash Flow Statement - Indirect MethodBimal KrishnaОценок пока нет

- Profit Center AccountingДокумент11 страницProfit Center AccountingManish bhasinОценок пока нет

- ACCT220 CFR-1 OutlineДокумент6 страницACCT220 CFR-1 OutlineReward IntakerОценок пока нет

- Financial Statement Analysis On BEXIMCO and SQUAREДокумент33 страницыFinancial Statement Analysis On BEXIMCO and SQUAREYolowii XanaОценок пока нет

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- Chapter 2Документ83 страницыChapter 2Korubel Asegdew YimenuОценок пока нет

- Executive SummaryДокумент6 страницExecutive Summaryravikiran1955100% (1)

- KCC Bank: Project Report ONДокумент61 страницаKCC Bank: Project Report ONSunny KhushdilОценок пока нет

- ACCOUNTING 105 LESSON NO 1.doc1Документ4 страницыACCOUNTING 105 LESSON NO 1.doc1Lee SuarezОценок пока нет

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- Accounts Complier (QB) @mission - CA - InterДокумент350 страницAccounts Complier (QB) @mission - CA - Intershivangi sharma0907100% (1)

- ADEVA - Assignment Discussions On Interim Financial ReportingДокумент3 страницыADEVA - Assignment Discussions On Interim Financial ReportingMaria Kathreena Andrea AdevaОценок пока нет

- Adh Newipo IpoДокумент759 страницAdh Newipo IpoSathishKumarОценок пока нет

- Financial and Managerial Accounting Principlesinternational Edition 9th Edition Crosson Test BankДокумент38 страницFinancial and Managerial Accounting Principlesinternational Edition 9th Edition Crosson Test BankChristinaMcmahonbiqka100% (10)

- Principles of FinanceДокумент11 страницPrinciples of FinanceKim MadisonОценок пока нет

- Colegio de Dagupan: Solve The Following Problems in The Space ProvidedДокумент5 страницColegio de Dagupan: Solve The Following Problems in The Space ProvidedKurt dela TorreОценок пока нет

- Pertemuan 4 - Understanding Income StatementДокумент62 страницыPertemuan 4 - Understanding Income StatementJhoni LimОценок пока нет

- Fundamentals DeptalsДокумент7 страницFundamentals DeptalsSamantha Nicole BonitoОценок пока нет

- Multi-Stepped Income Statement DirectionsДокумент4 страницыMulti-Stepped Income Statement DirectionsMary92% (12)

- Financial Accounting, 5e: Weygandt, Kieso, & KimmelДокумент31 страницаFinancial Accounting, 5e: Weygandt, Kieso, & KimmelAuora BiancaОценок пока нет

- Revaluation and ImpairmentДокумент4 страницыRevaluation and ImpairmentWertdie stanОценок пока нет

- Massage Therapy Business Plan ExampleДокумент22 страницыMassage Therapy Business Plan ExampleSergei Biriukov100% (2)

- CFAP 1 AAFR Summer 2017Документ10 страницCFAP 1 AAFR Summer 2017Aqib SheikhОценок пока нет

- Accounting Principles 10th Edition Weygandt Kimmel Chapter 4 and 5Документ14 страницAccounting Principles 10th Edition Weygandt Kimmel Chapter 4 and 5NiizamUddinBhuiyan100% (1)

- Financial Accounting Sub2 PDFДокумент219 страницFinancial Accounting Sub2 PDFAkhilesh Vish100% (3)

- The Guide To Writing A Business Plan Is Designed To Help New or ExistingДокумент10 страницThe Guide To Writing A Business Plan Is Designed To Help New or ExistingSenelwa AnayaОценок пока нет

- A Step By Step Guide: How to Perform Risk Based Internal Auditing for Internal Audit BeginnersОт EverandA Step By Step Guide: How to Perform Risk Based Internal Auditing for Internal Audit BeginnersРейтинг: 4.5 из 5 звезд4.5/5 (11)