Вам также может понравиться

- Public Financing for Small and Medium-Sized Enterprises: The Cases of the Republic of Korea and the United StatesОт EverandPublic Financing for Small and Medium-Sized Enterprises: The Cases of the Republic of Korea and the United StatesОценок пока нет

- Guidance Note on State-Owned Enterprise Reform for Nonsovereign and One ADB ProjectsОт EverandGuidance Note on State-Owned Enterprise Reform for Nonsovereign and One ADB ProjectsОценок пока нет

- (Microsoft Word - NBFCsДокумент4 страницы(Microsoft Word - NBFCsrvaidya2000Оценок пока нет

- Commercial Banks and Industrial Finance GÇô Evolving RoleДокумент26 страницCommercial Banks and Industrial Finance GÇô Evolving RoletarunОценок пока нет

- RETAIL BANKING IN INDIAДокумент28 страницRETAIL BANKING IN INDIAPreeti MishraОценок пока нет

- (Microsoft Word - Financial MarketsДокумент3 страницы(Microsoft Word - Financial Marketsrvaidya2000Оценок пока нет

- Current Fraud Trends in The Financial SectorДокумент28 страницCurrent Fraud Trends in The Financial SectorkrishnaraopvrОценок пока нет

- Retail BankingДокумент56 страницRetail BankingAnand RoseОценок пока нет

- FS Assignment 1Документ5 страницFS Assignment 1Manish SharmaОценок пока нет

- Bajaj FinanceДокумент65 страницBajaj FinanceAshutoshSharmaОценок пока нет

- HDFC Bank Car Loan Finance AnalysisДокумент40 страницHDFC Bank Car Loan Finance AnalysisAneesAnsariОценок пока нет

- Name: Jay Ketanbhai Changela Enrollment No.: 20fomba11508 For The Submission Of: SeeДокумент26 страницName: Jay Ketanbhai Changela Enrollment No.: 20fomba11508 For The Submission Of: SeeMAANОценок пока нет

- YES BANK'S FUTURE IN FINTECHДокумент5 страницYES BANK'S FUTURE IN FINTECHDeepak BhatiaОценок пока нет

- Rural Entrepreneurship FinancingДокумент4 страницыRural Entrepreneurship FinancingiamgauravaОценок пока нет

- Retail BankingДокумент15 страницRetail BankingjazzrulzОценок пока нет

- Universiti Utara Malaysia: Corporate Financial Management (BWFF5013)Документ14 страницUniversiti Utara Malaysia: Corporate Financial Management (BWFF5013)orient4Оценок пока нет

- Commercial Banks Rural India Challenges OpportunitiesДокумент16 страницCommercial Banks Rural India Challenges OpportunitiesRaghav guptaОценок пока нет

- Inancial Inclusion: - A Path Towards India's Future Economic GrowthДокумент30 страницInancial Inclusion: - A Path Towards India's Future Economic GrowthAnkur JainОценок пока нет

- The Future of Microfinance in IndiaДокумент3 страницыThe Future of Microfinance in IndiaSurbhi AgarwalОценок пока нет

- KPMG CII Indian BankingДокумент32 страницыKPMG CII Indian BankingMukesh Pareek100% (1)

- Role of Banks in Economic DevelopmentДокумент19 страницRole of Banks in Economic DevelopmentBatch 27Оценок пока нет

- Credit Risk Management in BanksДокумент53 страницыCredit Risk Management in Banksrahulhaldankar100% (1)

- Analysis of Growth Prospects of Non BankДокумент7 страницAnalysis of Growth Prospects of Non Bankmahesh toshniwalОценок пока нет

- BANKING INDUSTRY-Fundamental AnalysisДокумент19 страницBANKING INDUSTRY-Fundamental AnalysisGopi Krishnan.nОценок пока нет

- Fundamental analysis of India's banking industryДокумент19 страницFundamental analysis of India's banking industryGopi Krishnan.nОценок пока нет

- Introduction of Banking IndustryДокумент15 страницIntroduction of Banking IndustryArchana Mishra100% (1)

- Causes of NPAДокумент7 страницCauses of NPAsggovardhan0% (1)

- Financial Inclusion and Information Technology Usha Thorat: SpeechДокумент6 страницFinancial Inclusion and Information Technology Usha Thorat: SpeechBharat SuvarnaОценок пока нет

- BANKS LARGELY FAILED" Banks Largely Failed at Improving Financial Inclusion in IndiaДокумент6 страницBANKS LARGELY FAILED" Banks Largely Failed at Improving Financial Inclusion in IndiaParang MehtaОценок пока нет

- Accounting and Auditing Update October 2014Документ32 страницыAccounting and Auditing Update October 2014bhatepoonamОценок пока нет

- Case Studies Financial ServicesДокумент12 страницCase Studies Financial ServicesHemant JainОценок пока нет

- Indian Banking: The New Landscape : K. C. ChakrabartyДокумент6 страницIndian Banking: The New Landscape : K. C. Chakrabartyrgovindan123Оценок пока нет

- Crisis-proof Indian banking sector delivers inclusive growthДокумент3 страницыCrisis-proof Indian banking sector delivers inclusive growthMithesh PhadtareОценок пока нет

- Shyamala Gopinath: Retail Banking - Opportunities and ChallengesДокумент5 страницShyamala Gopinath: Retail Banking - Opportunities and ChallengesAmol ShindeОценок пока нет

- DISSERTATION RE NikhilДокумент37 страницDISSERTATION RE NikhilNikhil Ranjan50% (2)

- Chapter 3Документ4 страницыChapter 3Cupid CuteОценок пока нет

- Service Sector BankingДокумент63 страницыService Sector BankingsayliОценок пока нет

- Akshu Full ProjectДокумент73 страницыAkshu Full ProjectAshwini VenugopalОценок пока нет

- BANKING2Документ21 страницаBANKING2Ansh JunejaОценок пока нет

- Rural Banking in IndiaДокумент63 страницыRural Banking in IndiaAniket AutkarОценок пока нет

- A Study On Customer Perception Towards The Services Offered in Retail Banking by South Indian Bank, Vennikulam Branch (Kerala)Документ71 страницаA Study On Customer Perception Towards The Services Offered in Retail Banking by South Indian Bank, Vennikulam Branch (Kerala)Lini Susan John100% (4)

- What Is Financial InclusionДокумент10 страницWhat Is Financial InclusionSanjeev ReddyОценок пока нет

- Banking SectorДокумент10 страницBanking SectorMichael ChawiyaОценок пока нет

- Research ProjectДокумент79 страницResearch ProjectPriyanka SadaphuleОценок пока нет

- Complete Analysis of Bandhan BankДокумент18 страницComplete Analysis of Bandhan BankAkashОценок пока нет

- Blackbook FinalДокумент86 страницBlackbook Finalgunesh somayaОценок пока нет

- Project Draft - 10927873Документ2 страницыProject Draft - 10927873moneyeeshОценок пока нет

- Challenges and Scope of Retail Banking in IndiaДокумент6 страницChallenges and Scope of Retail Banking in Indiasearock25decОценок пока нет

- Study Retail Banking Operations Customer OpinionsДокумент47 страницStudy Retail Banking Operations Customer Opinionszaru1121Оценок пока нет

- Electronica Finance Limited: Designing The Future of Micro, Small, and Medium EnterprisesДокумент11 страницElectronica Finance Limited: Designing The Future of Micro, Small, and Medium EnterprisesSamadarshi SiddharthaОценок пока нет

- Role of Commercial Bank in The Economic Development of INDIAДокумент5 страницRole of Commercial Bank in The Economic Development of INDIAVaibhavRanjankar0% (1)

- Indian Economy OverviewДокумент26 страницIndian Economy OverviewGokul KrishnanОценок пока нет

- Beyond Hoopla: Simply Financial InclusionДокумент3 страницыBeyond Hoopla: Simply Financial InclusionJatinder HandooОценок пока нет

- Vishakha Black Book ProjectДокумент48 страницVishakha Black Book ProjectrohitОценок пока нет

- Indian Banking SectorДокумент5 страницIndian Banking Sector2612010Оценок пока нет

- SWOT Analysis of Indian Banking Sector and SBI BankДокумент5 страницSWOT Analysis of Indian Banking Sector and SBI BankRITIKAОценок пока нет

- Financing SMEs in IndiaДокумент3 страницыFinancing SMEs in Indiaram9261891Оценок пока нет

- Credit Score EssayДокумент24 страницыCredit Score EssaypavistatsОценок пока нет

- Service Sector: BankingДокумент62 страницыService Sector: Bankingsteffszone100% (4)

- Toward Inclusive Access to Trade Finance: Lessons from the Trade Finance Gaps, Growth, and Jobs SurveyОт EverandToward Inclusive Access to Trade Finance: Lessons from the Trade Finance Gaps, Growth, and Jobs SurveyОценок пока нет

- Letter To Prof R VaidyanathanДокумент2 страницыLetter To Prof R Vaidyanathanrvaidya2000Оценок пока нет

- Aranganin Pathaiyil ProfileДокумент5 страницAranganin Pathaiyil Profilervaidya2000Оценок пока нет

- NOV 2008 India PR ApprovingInvestmentДокумент6 страницNOV 2008 India PR ApprovingInvestmentrvaidya2000Оценок пока нет

- RESERVE BANK OF INDIA - : Investment in Credit Information CompaniesДокумент1 страницаRESERVE BANK OF INDIA - : Investment in Credit Information Companiesrvaidya2000Оценок пока нет

- How Did China Take Off US China Report 2012 "Uschinareport - Com-Wp-Con... Ds-2013!05!23290284.PDF" (1) .PDF - 1Документ25 страницHow Did China Take Off US China Report 2012 "Uschinareport - Com-Wp-Con... Ds-2013!05!23290284.PDF" (1) .PDF - 1rvaidya2000Оценок пока нет

- SGFX FinancialsДокумент33 страницыSGFX FinancialsPGurusОценок пока нет

- National Herald NarrativeДокумент2 страницыNational Herald Narrativervaidya2000Оценок пока нет

- Subramanian Testimony 31313Документ25 страницSubramanian Testimony 31313PGurusОценок пока нет

- Letter To PMДокумент3 страницыLetter To PMrvaidya2000Оценок пока нет

- Vimarsha On Indian Economy - Myth and RealityДокумент1 страницаVimarsha On Indian Economy - Myth and Realityrvaidya2000Оценок пока нет

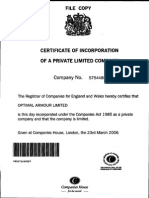

- Optimal Armour Corporate FilingsДокумент198 страницOptimal Armour Corporate FilingsPGurusОценок пока нет

- TVEs Growth Engines of China in 1980s - 1990s "WWW - Geoffrey-Hodgson - Inf... - Brakes-chinese-Dev - PDF"Документ24 страницыTVEs Growth Engines of China in 1980s - 1990s "WWW - Geoffrey-Hodgson - Inf... - Brakes-chinese-Dev - PDF"rvaidya2000Оценок пока нет

- Ahmedabad Press Conference Nov 19 2015Документ5 страницAhmedabad Press Conference Nov 19 2015PGurus100% (1)

- Composite Resin Corporate FilingsДокумент115 страницComposite Resin Corporate FilingsPGurus100% (2)

- Letter and Invitaion Give To Mr. r.v19!06!2015Документ2 страницыLetter and Invitaion Give To Mr. r.v19!06!2015rvaidya2000Оценок пока нет

- Brief Look at The History of Temples in IIT Madras Campus (Arun Ayyar, Harish Ganapathy, Hemanth C, 2014)Документ17 страницBrief Look at The History of Temples in IIT Madras Campus (Arun Ayyar, Harish Ganapathy, Hemanth C, 2014)Srini KalyanaramanОценок пока нет

- Sec 66AДокумент5 страницSec 66Arvaidya2000Оценок пока нет

- NGO's A Perspective 31-01-2015Документ29 страницNGO's A Perspective 31-01-2015rvaidya2000Оценок пока нет

- FDI in Retail - Facts & MythsДокумент128 страницFDI in Retail - Facts & Mythsrvaidya2000Оценок пока нет

- Why India Needs To Prepare For The Decline of The WestДокумент4 страницыWhy India Needs To Prepare For The Decline of The Westrvaidya2000Оценок пока нет

- GrantsДокумент1 страницаGrantsrvaidya2000Оценок пока нет

- Representation To PMДокумент31 страницаRepresentation To PMIrani SaroshОценок пока нет

- Timetable & AgendaДокумент6 страницTimetable & Agendarvaidya2000Оценок пока нет

- Shamelessness Is Paraded As ModernДокумент2 страницыShamelessness Is Paraded As Modernrvaidya2000Оценок пока нет

- Humbug Over KashmirДокумент4 страницыHumbug Over Kashmirrvaidya2000Оценок пока нет

- Secular Assault On The SacredДокумент3 страницыSecular Assault On The Sacredrvaidya2000Оценок пока нет

- Why The Retail Revolution Is Meeting Its NemesisДокумент3 страницыWhy The Retail Revolution Is Meeting Its Nemesisrvaidya2000Оценок пока нет

- Decline of The West Is Good For Us and Them - 11 Oct 2011Документ4 страницыDecline of The West Is Good For Us and Them - 11 Oct 2011rvaidya2000Оценок пока нет

- Why The Indian Housewife Deserves Paeans of PraiseДокумент3 страницыWhy The Indian Housewife Deserves Paeans of Praiservaidya2000Оценок пока нет

- Why Sub-Prime Is Not A Crisis in IndiaДокумент4 страницыWhy Sub-Prime Is Not A Crisis in Indiarvaidya2000Оценок пока нет