Вам также может понравиться

- Business Plan Template Excel FreeДокумент13 страницBusiness Plan Template Excel FreeShreya More75% (8)

- Mitc For Amazon Pay Credit CardДокумент7 страницMitc For Amazon Pay Credit CardBlain Santhosh FernandesОценок пока нет

- General Vs BarramedaДокумент11 страницGeneral Vs BarramedaShivaОценок пока нет

- Servicewide Specialists v. CAДокумент2 страницыServicewide Specialists v. CAd2015memberОценок пока нет

- BankruptcyДокумент56 страницBankruptcycharlesayres83100% (1)

- Darvas Box SummaryДокумент7 страницDarvas Box SummaryVijayОценок пока нет

- Global Business Holdings v. SurecompДокумент2 страницыGlobal Business Holdings v. Surecompd2015member100% (1)

- Tuason v. ZamoraДокумент1 страницаTuason v. Zamorad2015member100% (1)

- Lalican Vs Insular LifeДокумент1 страницаLalican Vs Insular LifeGian Tristan MadridОценок пока нет

- Allied Bank Vs CAДокумент4 страницыAllied Bank Vs CAEllen Glae DaquipilОценок пока нет

- Prudential Guarantee and Assurance Inc. v. Trans Asia Shipping Lines G.R. No. 151890 June 20 2006Документ3 страницыPrudential Guarantee and Assurance Inc. v. Trans Asia Shipping Lines G.R. No. 151890 June 20 2006Abilene Joy Dela CruzОценок пока нет

- Mortgages 2019Документ60 страницMortgages 2019Ivana JayОценок пока нет

- 029 Mactan Cebu Intl Airport vs. Marcos 261 Scra 667 DigestДокумент1 страница029 Mactan Cebu Intl Airport vs. Marcos 261 Scra 667 DigestjayinthelongrunОценок пока нет

- The Canadian Patriot Special: Republic or Colony?Документ49 страницThe Canadian Patriot Special: Republic or Colony?Matthew EhretОценок пока нет

- Journey Towards CashlessДокумент89 страницJourney Towards CashlessKatherine Valiente100% (1)

- Sanitary Steam Vs CAДокумент1 страницаSanitary Steam Vs CAEhlla MacatangayОценок пока нет

- PAMECA v. CAДокумент2 страницыPAMECA v. CAd2015member83% (6)

- 06 Blue Cross Health Care, Inc. v. OlivaresДокумент3 страницы06 Blue Cross Health Care, Inc. v. OlivaresRem SerranoОценок пока нет

- 1 Argente Vs West Coast LifeДокумент1 страница1 Argente Vs West Coast LifePiaОценок пока нет

- FIRST LEPANTO-TAISHO INSURANCE CORPORATION vs. CHEVRON Phil Case Digest 2012 (Surety)Документ2 страницыFIRST LEPANTO-TAISHO INSURANCE CORPORATION vs. CHEVRON Phil Case Digest 2012 (Surety)Sam LeynesОценок пока нет

- Francisco v. Toll Regulatory BoardДокумент3 страницыFrancisco v. Toll Regulatory Boardd2015memberОценок пока нет

- Zialcita-Yuseco v. SimmonsДокумент1 страницаZialcita-Yuseco v. Simmonsd2015memberОценок пока нет

- People v. JolliffeДокумент1 страницаPeople v. Jolliffed2015memberОценок пока нет

- Cebu Shipyard V William LinesДокумент2 страницыCebu Shipyard V William LinesJanelle ManzanoОценок пока нет

- Soliman, National Leather, EdralinДокумент3 страницыSoliman, National Leather, EdralinjohnmiggyОценок пока нет

- Recentes v. CFIДокумент1 страницаRecentes v. CFId2015memberОценок пока нет

- First Lepanto v. ChevronДокумент2 страницыFirst Lepanto v. ChevronRoger Pascual CuaresmaОценок пока нет

- Home Loan Research Report 1Документ33 страницыHome Loan Research Report 1HK195929% (7)

- Sps Dalion v. CAДокумент1 страницаSps Dalion v. CAd2015memberОценок пока нет

- Travellers Insurance & Surety Corporation Vs Hon. Court of Appeals & Vicente MendozaДокумент2 страницыTravellers Insurance & Surety Corporation Vs Hon. Court of Appeals & Vicente Mendozamonet_antonio50% (2)

- Insurance Case DigestsДокумент28 страницInsurance Case DigestsBernadette Quitoriano67% (3)

- JAIME T. GAISANO, Petitioner, vs. DEVELOPMENT INSURANCE AND SURETY CORPORATION, RespondentДокумент3 страницыJAIME T. GAISANO, Petitioner, vs. DEVELOPMENT INSURANCE AND SURETY CORPORATION, RespondentWilliam Azucena100% (1)

- Secuya v. de SelmaДокумент1 страницаSecuya v. de Selmad2015memberОценок пока нет

- 5 Nunez v. SLTEAS Phoenix Forcible EntryДокумент2 страницы5 Nunez v. SLTEAS Phoenix Forcible EntrySarah GantoОценок пока нет

- 5sundiang Aquino Commercial Law InsuranceДокумент142 страницы5sundiang Aquino Commercial Law InsuranceAtotz ToinkОценок пока нет

- Fue Leung V IACДокумент2 страницыFue Leung V IACd2015memberОценок пока нет

- ADPOE - Case Digest - Calo v. FuertesДокумент1 страницаADPOE - Case Digest - Calo v. Fuertesbrazenangel03Оценок пока нет

- 02 Evangelista v. JarencioДокумент2 страницы02 Evangelista v. Jarenciod2015memberОценок пока нет

- Great Pacific V CA G.R. No. 113899. October 13, 1999Документ2 страницыGreat Pacific V CA G.R. No. 113899. October 13, 1999Rosemarie Barnido MadarangОценок пока нет

- Korea Exchange Bank v. FilkorДокумент2 страницыKorea Exchange Bank v. Filkord2015memberОценок пока нет

- 21Документ1 страница21James WilliamОценок пока нет

- Doctrine of TracingДокумент34 страницыDoctrine of TracingAkmal SafwanОценок пока нет

- Musngi Vs West Coast InsuranceДокумент1 страницаMusngi Vs West Coast InsuranceSimon James SemillaОценок пока нет

- RCBC v. Royal CargoДокумент2 страницыRCBC v. Royal Cargod2015memberОценок пока нет

- Tan vs. CaДокумент2 страницыTan vs. CaMich AngelesОценок пока нет

- Velasco Vs Apostol DigestedДокумент3 страницыVelasco Vs Apostol DigestedMan2x SalomonОценок пока нет

- De Gala v. de GalaДокумент2 страницыDe Gala v. de Galad2015memberОценок пока нет

- Silicon Phils Inc Vs CirДокумент1 страницаSilicon Phils Inc Vs CirlacbayenОценок пока нет

- Envi Law Cases and Special Laws Part 2Документ42 страницыEnvi Law Cases and Special Laws Part 2mccm92Оценок пока нет

- Jen Sherry Wee Vs Atty. LimДокумент1 страницаJen Sherry Wee Vs Atty. LimTim PuertosОценок пока нет

- 120737-2004-Concept Placement Resources Inc. v. FunkДокумент4 страницы120737-2004-Concept Placement Resources Inc. v. FunkJee CortezОценок пока нет

- HH Hollero Construction Vs GsisДокумент1 страницаHH Hollero Construction Vs GsisAbhor TyrannyОценок пока нет

- Villareal v. RamirezДокумент2 страницыVillareal v. Ramirezd2015memberОценок пока нет

- Fieldmen'S Insurance Co., Inc. vs. Mercedes Vargas Vda. de Songco, Et Al. and Court of AppealsДокумент2 страницыFieldmen'S Insurance Co., Inc. vs. Mercedes Vargas Vda. de Songco, Et Al. and Court of AppealsTiff DizonОценок пока нет

- Insurance Case Digest 2Документ3 страницыInsurance Case Digest 2Jumel CapurcosОценок пока нет

- US vs. Reyes, 1 Phil. 375Документ2 страницыUS vs. Reyes, 1 Phil. 375Jay CruzОценок пока нет

- Security Bank v. CuencaДокумент2 страницыSecurity Bank v. Cuencad2015memberОценок пока нет

- VELASCO vs. APOSTOLДокумент2 страницыVELASCO vs. APOSTOLAlmarius CadigalОценок пока нет

- Nmims Final Report123 PDFДокумент46 страницNmims Final Report123 PDFHimanshu KhandelwalОценок пока нет

- Navia V Padrico - Case DigestДокумент2 страницыNavia V Padrico - Case DigestLourdes LescanoОценок пока нет

- 24 Velasco v. ApostoДокумент1 страница24 Velasco v. Apostoclarence esguerraОценок пока нет

- Confidence and Trust.: Law On PartnershipsДокумент8 страницConfidence and Trust.: Law On PartnershipsDwight BlezaОценок пока нет

- Delsan Transport Lines vs. CAДокумент2 страницыDelsan Transport Lines vs. CAKris HannahОценок пока нет

- Title 9 LOSS PPT Presentation v1Документ17 страницTitle 9 LOSS PPT Presentation v1Nikolai SiccuanОценок пока нет

- Garcia Vs Hongkong Fire and Marine InsuranceДокумент2 страницыGarcia Vs Hongkong Fire and Marine InsurancejezzahОценок пока нет

- Great Pacific Life-vs-CAДокумент2 страницыGreat Pacific Life-vs-CAmario navalezОценок пока нет

- Belgian Vs MagallanesДокумент2 страницыBelgian Vs MagallanesTalina BinondoОценок пока нет

- 2023 Property Old CurriculumДокумент19 страниц2023 Property Old CurriculumAleiah Jean LibatiqueОценок пока нет

- 48 Pioneer Concrete V TodaroДокумент2 страницы48 Pioneer Concrete V TodaroKenzo RodisОценок пока нет

- Insular Life Assurance CoДокумент1 страницаInsular Life Assurance CoLDОценок пока нет

- 27 OCA Vs CanqueДокумент2 страницы27 OCA Vs CanqueJude Raphael CollantesОценок пока нет

- 2C Digests TAX I (Updated)Документ52 страницы2C Digests TAX I (Updated)Angelique Porta100% (1)

- G.R. No. 85141. November 28, 1989. Filipino Merchants Insurance Co., Inc., Petitioner, vs. Court of Appeals and Choa Tiek Seng, RespondentsДокумент10 страницG.R. No. 85141. November 28, 1989. Filipino Merchants Insurance Co., Inc., Petitioner, vs. Court of Appeals and Choa Tiek Seng, RespondentsTrea CheryОценок пока нет

- SAMAYLA, Luriza Legal Forms Week4-5Документ11 страницSAMAYLA, Luriza Legal Forms Week4-5Luriza SamaylaОценок пока нет

- Torts Cases IДокумент13 страницTorts Cases IRgenieDictadoОценок пока нет

- Lino Fernandez Vs MeralcoДокумент11 страницLino Fernandez Vs Meralcokristel jane caldozaОценок пока нет

- Atlas V CIRДокумент1 страницаAtlas V CIRBrylle Garnet DanielОценок пока нет

- 4 INSURANCE Part 1 Contracts of InsuranceДокумент5 страниц4 INSURANCE Part 1 Contracts of InsuranceRuby SantillanaОценок пока нет

- Villacorta Vs Insurance CommissionДокумент1 страницаVillacorta Vs Insurance CommissionKate HizonОценок пока нет

- TORTS - 36. Schmitz Transport and Brokerage Corp. v. Transport Venture, Inc.Документ14 страницTORTS - 36. Schmitz Transport and Brokerage Corp. v. Transport Venture, Inc.Mark Gabriel B. MarangaОценок пока нет

- Insular v. KhuДокумент2 страницыInsular v. KhuAleah LS KimОценок пока нет

- Fajardo v. CorralДокумент6 страницFajardo v. CorralAnthony Rey BayhonОценок пока нет

- 3 - 4 - 5 - 10 Mercantile DigestДокумент6 страниц3 - 4 - 5 - 10 Mercantile DigestjoОценок пока нет

- FRIA HazangДокумент2 страницыFRIA HazangAnonymous KvztB3Оценок пока нет

- Presumption of Negligence Pestano vs. Sumayang FactsДокумент2 страницыPresumption of Negligence Pestano vs. Sumayang FactsJayОценок пока нет

- Premium Double InsuranceДокумент9 страницPremium Double InsuranceLDОценок пока нет

- NobiagonДокумент5 страницNobiagonNyl John Caesar GenobiagonОценок пока нет

- Capital Insurance and Surety CoДокумент17 страницCapital Insurance and Surety CoMarc Gar-ciaОценок пока нет

- Traders Royal Bank v. CAДокумент1 страницаTraders Royal Bank v. CAd2015memberОценок пока нет

- Best Short StoriesДокумент3 страницыBest Short Storiesd2015memberОценок пока нет

- BPI v. IAC & Sps CanlasДокумент1 страницаBPI v. IAC & Sps Canlasd2015memberОценок пока нет

- Sealand v. CAДокумент2 страницыSealand v. CAd2015memberОценок пока нет

- Luzon Stevedoring v. PSCДокумент2 страницыLuzon Stevedoring v. PSCd2015memberОценок пока нет

- Lemi v. ValenciaДокумент2 страницыLemi v. Valenciad2015memberОценок пока нет

- Ursal v. CTAДокумент1 страницаUrsal v. CTAd2015member100% (1)

- Alzate v. AldanaДокумент1 страницаAlzate v. Aldanad2015memberОценок пока нет

- Diolosa v. CAДокумент1 страницаDiolosa v. CAd2015memberОценок пока нет

- ACME Shoe v. CAДокумент1 страницаACME Shoe v. CAd2015memberОценок пока нет

- Quelnan v. VHFДокумент2 страницыQuelnan v. VHFd2015memberОценок пока нет

- Bank Reconciliation StatementДокумент40 страницBank Reconciliation StatementPrashant100% (1)

- Description: Tags: Top 100 Current Holders Cor Vers1Документ4 страницыDescription: Tags: Top 100 Current Holders Cor Vers1anon-20972Оценок пока нет

- Tybbi Auditing-II 2021Документ88 страницTybbi Auditing-II 2021Anonymous HackerОценок пока нет

- RBI/FED/2015-16/13 FED Master Direction No.18/2015-16 January 1, 2016Документ135 страницRBI/FED/2015-16/13 FED Master Direction No.18/2015-16 January 1, 2016harsh2709golchhaОценок пока нет

- Madina Book1 Arabic TextДокумент7 страницMadina Book1 Arabic TextChetan ChoudharyОценок пока нет

- The New Concept of Alignment, Bleaching and Bonding. A Course With Inman Aligner in Dubai, United Arab Emirates.Документ1 страницаThe New Concept of Alignment, Bleaching and Bonding. A Course With Inman Aligner in Dubai, United Arab Emirates.InmanAlignerОценок пока нет

- FYP Risk Management HDFC SecuritiesДокумент82 страницыFYP Risk Management HDFC Securitiespadmakar_rajОценок пока нет

- Smiths of Winterforge Rulebook 0.9Документ9 страницSmiths of Winterforge Rulebook 0.9NatsukiPLОценок пока нет

- The Financial Statement Auditing Environment: © 2017 Mcgraw-Hill Education (Malaysia) SDN BHDДокумент30 страницThe Financial Statement Auditing Environment: © 2017 Mcgraw-Hill Education (Malaysia) SDN BHDSarannyaRajendraОценок пока нет

- What Is A Continuing Guarantee and What Are Its Modes of RevocationДокумент4 страницыWhat Is A Continuing Guarantee and What Are Its Modes of RevocationNitya Nand Pandey100% (1)

- L3 Organizational Structure of BanksДокумент17 страницL3 Organizational Structure of Banksakshita raoОценок пока нет

- Co Operative Housing SocietyДокумент29 страницCo Operative Housing Societyvenkynaidu100% (1)

- Bank Reconciliation StatementsДокумент3 страницыBank Reconciliation StatementsPatrick Prem GomesОценок пока нет

- A01 Summer Training Project Report: Marketing MixДокумент56 страницA01 Summer Training Project Report: Marketing MixJaiHanumankiОценок пока нет

- Salient Features of Insurance LawДокумент7 страницSalient Features of Insurance Lawnusratopee100% (1)

- Karnataka ANNUAL REPORT English - 2016-17Документ82 страницыKarnataka ANNUAL REPORT English - 2016-17K Srinivasa MurthyОценок пока нет

- Publice Notice Merger Notification Arise B.V and NMB 20170629Документ2 страницыPublice Notice Merger Notification Arise B.V and NMB 20170629Anonymous iFZbkNw100% (2)

- MFL 16 17 Ar PDFДокумент120 страницMFL 16 17 Ar PDFSatvinder Deep SinghОценок пока нет

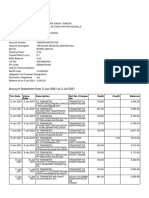

- Account Statement From 3 Jan 2021 To 3 Jul 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceДокумент8 страницAccount Statement From 3 Jan 2021 To 3 Jul 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceSanatan ThakurОценок пока нет