Академический Документы

Профессиональный Документы

Культура Документы

4Q07 Earnings Release

Загружено:

LightRI0 оценок0% нашли этот документ полезным (0 голосов)

25 просмотров34 страницыLight posts R$1. Billion income in 2007 Annual income on a recurring basis totals R$226. Million. Net income amounted to R$1,077. Million against accrued losses of R$150. Million in 2006. In 2007, EBITDA totaled R$1,105. Million, a 49.7% growth compared to the EBITDA recorded in 2006.

Исходное описание:

Авторское право

© Attribution Non-Commercial (BY-NC)

Доступные форматы

PDF, TXT или читайте онлайн в Scribd

Поделиться этим документом

Поделиться или встроить документ

Этот документ был вам полезен?

Это неприемлемый материал?

Пожаловаться на этот документLight posts R$1. Billion income in 2007 Annual income on a recurring basis totals R$226. Million. Net income amounted to R$1,077. Million against accrued losses of R$150. Million in 2006. In 2007, EBITDA totaled R$1,105. Million, a 49.7% growth compared to the EBITDA recorded in 2006.

Авторское право:

Attribution Non-Commercial (BY-NC)

Доступные форматы

Скачайте в формате PDF, TXT или читайте онлайн в Scribd

0 оценок0% нашли этот документ полезным (0 голосов)

25 просмотров34 страницы4Q07 Earnings Release

Загружено:

LightRILight posts R$1. Billion income in 2007 Annual income on a recurring basis totals R$226. Million. Net income amounted to R$1,077. Million against accrued losses of R$150. Million in 2006. In 2007, EBITDA totaled R$1,105. Million, a 49.7% growth compared to the EBITDA recorded in 2006.

Авторское право:

Attribution Non-Commercial (BY-NC)

Доступные форматы

Скачайте в формате PDF, TXT или читайте онлайн в Scribd

Вы находитесь на странице: 1из 34

1

Light posts R$1.1 billion income

in 2007

Annual income on a recurring basis totals

R$226.0 million

In 2007, Lights net income amounted to R$1,077.2 million

against accrued losses of R$150.5 million in 2006, as a result of the

Companys better operating performance coupled with the use of

deferred tax credits totaling R$851.2 million. Net income on a

recurring basis; i.e., net of the use of tax credits, amounted to

R$226.0 million, 58.8% higher than the 2006 recurring income.

Net Revenue in 2007 totaled R$4,992.4 million, 0.8% higher

than in 2006, as a result of the stable behavior of the billed

consumption in the captive market, coupled with the flat tariff

change in 2007 in relation to 2006, until the tariff adjustment in

November 2007.

In 2007, EBITDA totaled R$1,105.0 million, a 49.7% growth

compared to the EBITDA recorded in 2006. Annual EBITDA margin

reached 22.1%, 7.2 p.p. higher than in 2006. "Cash EBITDA

1

for

the period was R$1,475.3 million, 11.1% higher than in 2006.

The Company's collection rate during 2007 stood at 99.4% of

billing, equivalent to a 6.4 p.p. improvement in relation to the

previous year. This result arose from debts negotiated with public

authorities and large customers, which have been regularizing their

current payments and paying their debts in installments, in addition

to efforts in improving collection with retail customers.

IR Contacts

Ronnie Vaz Moreira

CFO and Investor Relations

Officer

Ricardo Levy

Financial and IR Officer

Cristina Guedes

IR Manager

Tel: +55 (21) 2211-2650/

2660

Fax: +55 (21) 2211-2787

www.light.com.br

E-mail: ri@light.com.br

Conference Call

Date: 15/02/2008

Time: 2:30 PM (Brazil)

11:30 AM (US ET)

Phones:

Brazil:

+55 (11) 4688-6301

USA:

+1 (888) 700-0802

Other countries:

+1 (786) 924-8430

Simultaneous

interpretation into

English

Webcast:

www.light.com.br

(Portuguese and English)

Operational Highlights (GWh) 4Q07 4Q06 Var. % 2007 2006 Var. %

Grid Load* 8,510 8,162 4.3% 33,160 31,625 4.9%

Billed Energy - Distribution 4,554 4,582 -0.6% 18,307 18,260 0.3%

Transported Energy - TUSD 2,011 1,865 7.8% 7,984 7,012 13.9%

Sold Energy - Generation 1,279 1,229 4.1% 4,968 4,847 2.5%

Commercializated Energy (Esco) 44 - - 175 - -

Financial Highlights (R$ MM)

Gross Revenue 1,978 2,066 -4.2% 8,138 7,997 1.8%

Net Revenue 1,077 1,287 -16.3% 4,992 4,951 0.8%

EBITDA 73 366 -80.1% 1,105 738 49.7%

EBITDA Margin 6.8% 28.5% - 22.1% 14.9% -

Net Income 229 94 144.1% 1,077 -150 -

Net Debt 1,462 2,540 -42.4% 1,462 2,540 -42.4%

* Captive market + losses + network use

2

At year-end, the Companys net debt totaled R$1,462 million,

equivalent to a 42.4% reduction in relation to the end of 2006.

This decrease is a result of the conversion of R$800 million in

debentures of the 4

th

Issuance into shares and also of the higher

operating cash generation.

Over the second and third quarters of the 2007 fiscal year, the

Company, based on the opinion of its legal counsel and having

submitted the matter to prior assessment by its independent

auditors, and since it believes that the tax authorities right to levy

taxes has lapsed, carried out the reversal of provisions related to

the increase in the calculation basis of PIS/COFINS and the growth

of the COFINS rate from 2% to 3%, in the net amount of R$265.5

million (R$239.3 million posted in the Financial Results, R$163.0

million posted under Gross Revenue Deductions and the related

impacts on the IT/SC totaling R$136.8 million). These provision

reversals were reflected in the June and September quarterly

statements presented by the Company and reviewed by the

independent auditors, which issued an unqualified opinion. While

preparing its annual financial statements, the Company maintained

the previously adopted procedure, again based on the opinion of its

legal and accounting advisors. Our independent auditors changed

their understanding, and believe we should reconstitute the

provisions that were written off. In view of the new positioning

indicated by the independent auditors and in order to avoid a

qualification of its annual financial statements, the Companys

management decided to reconstitute the provisions. It is

important to note that such non-recurring provisions

impacted only the accounting result, with no impact on the

Company's cash. (See detailed explanation under exhibit V).

3

Segmentation of the Release

Light S.A. is a holding company that controls wholly-owned subsidiaries that participate in three

segments of the business: electricity distribution (Light SESA), generation (Light Energia) and

trading/services (Light Esco). In order to increase the transparency of its results and enable investors

to make a better evaluation, Light also presents its results in a segmented form.

Operating Performance

Distribution

The total electricity consumed in 2007 in Lights concession

area (captive + free customers) amounted to 23,653 GWh,

presenting a 3.3% growth in relation to 2006. This increase

was primarily due to consumption in the free market,

which accounted for 93.7% of this growth.

Captive Market

In 4Q07, consumption in the captive market

decreased 0.6% when compared to the same period

of the previous year, as a result of the reduced

number of low-voltage billable days in the period

(4.9 days, equivalent to approximately 69 GWh).

Taking into account this adjustment, total

consumption was in line with 4Q06. The industrial

class consumption reduction is explained by the

migration of three customers to the free market

between the periods, of which only one migrated

during 4Q07, offset by the increase in network use

(TUSD) collection.

In 2007, billed electricity amounted to 18,307 GWh,

equivalent to a 0.3% growth when compared to

2006. Despite the 1.9% and 3.1% increase in the residential and commercial classes, respectively,

there was a 14.3% reduction in industrial consumption, due to the migration of three customers in

2007 with an approximate average monthly consumption of 1,800 MWh, which was fully offset by the

expansion network use billings. Another factor contributing to the low growth in the consumption of the

Electric Power Consumption (GWh)

Total Market (Captive + Free)

18,260 18,307

4,644 5,346

22,904

23,653

2006 2007

Captive Free

0,3%

15,1%

3,3%

Electric Power Consumption (GWh)

4 Quarter

4,582

783

1,425

535

1,839

4,554

791

1,449

506

1,809

Residential Industrial Commercial Others Total

-1.6% -5.5% 1.7% 1.0% -0.6%

2006 2007

th

Electric Power Consumption (GWh)

Year

7,207

2,347

5,583

3,122

18,260

7,344

2,011

5,756

3,197

18,307

Residential Industrial Commercial Others Total

1.9% -14.3% 3.1% 2.4% 0.3%

2006 2007

4

captive market was the change in the billing methodology of public lighting, arranged with Rio Luz, a

local government utility, which resulted in the posting of a consumption 72 GWh lower this year in

comparison with the previous year.

Network Use

Network use (TUSD) billings were equivalent to 2,011 GWh this

quarter, of which 65.9% were for transportation to free market

customers and the remainder was to concessionaires that border

Lights concession area. The volume of electricity transported to free

customers increased 2.8% in relation to 4Q06, as a result of the

migration of customers from the captive to the free market.

In 2007, the volume of network use amounted to 7,984 GWh, 13.9%

higher than the volume transported in 2006, and the volume

transported to free market customers and to other concessionaires

increased by 15.1% and 11.4%, respectively, compared to 2006. Year-

to-date, nine customers migrated to the free market, equivalent to a

total billed consumption of 91 GWh, more than offsetting the equivalent

consumption reduction in the captive market.

Free Market - GWh

4th Quarter

1,291

1,326

1,865

575

2,011

685

Free Utility Total

2006 2007

2.8%

19.2%

7.8%

Free market - GWh

Year

4,644

2,368

7,012

5,346

2,638

7,984

Free Utility Total

2006 2007

15.1%

11.4%

13.9%

5

Energetic Balance

Electricity Losses

Total electricity losses (past 12 months) increased

from 6,251 GWh in December 2006 to 6,834 GWh in

December 2007, equivalent to a 0.8 p.p. growth in

wire load.

In 2007, initiatives for preventing losses were re-

oriented and aimed at ensuring effective long-term

gains. Between January and December, over 290,000

consumers were visited by teams inspecting the illegal use of electricity, resulting in 72 GWh of

electricity recovered and 170 GWh of electricity incorporated in the period.

The first months of 2007 were marked by operating issues faced by the Company as a result of setting

forth the pace required for carrying out the initiatives of electricity recovery due to the stabilization of

the new business management system, SAP-CCS, which was implemented in October 2006. At the end

of 2007, the Company acquired new software in order to support fraud prevention initiatives.

0.9% Residential 40.1%

222.3 7,343.8

CCEAR 1.2% 72.8% Billed Industrial 11.0%

Light Energia Energy 2,011.1

302.8 98.2% Own load 18,307.0

Light Commercial 31.4%

32.4% 25,141.2 5,755.6

Losses of

8,310.2 Energy Others 17.5%

25,612.8 27.2% 6,834.2 3,196.5

45.0%

11,532.6 Basic netw.

losses

24.8% 1.8% Adjustment 0.0

6,351.0

-4.3%

-1,106.1

(*) Others= Purchase in Spot - Sale in Spot.

PROINFA

OTHERS(*)

(CCEE)

DISTRIBUTION ENERGETIC BALANCE - GWh

NORTE FLU

(CCEE)

Required E.

(CCEE)

AUCTIONS

(CCEE)

471.6

ITAIPU

(CCEE)

Position: january-december 2007

Light Losses Evolution

12 month

6

,

8

3

4

6

,

6

1

1

6

,

4

5

7

6

,

2

3

2

6

,

2

5

1

20.6

19.8

19.5

19.8

20.2

1 2 3 4 5

GWh Losses % Losses / Wire Load (Own + Transport)

6

As a result of the need of a substantial investment - related to the Companys activities for decreasing

its losses - and the high rate of existing delinquency, the Company decided to fully focus on the

collection of customers debts, due to the higher potential for recovering cash, which made possible a

higher level of investments in the prevention of losses from 2008.

A plan for adopting new measurement and distribution network protection technologies for preventing

losses was established. This project provides for the adoption of this technology with 140,000 low-

voltage customers in the first phase and the construction of a Measurement Control Center for

managing automated processes. The installation of the measurement equipment will begin in 2008. In

addition, the Company continues to invest in regular initiatives of inspection and normalization of

customers and to replace obsolete meters.

Delinquency

In 4Q07, the Companys collection rate

continued to present a substantial improvement,

from 94.8% in 4Q06 to 98.6% of billings in

this quarter, as a result of improvements in

the receipt of billed electricity, as well as of the

installments of electricity debts negotiated

with large customers and public authorities. In

2007, there was a great expansion in anti-

delinquency initiatives based on the plan

implemented by the new management. The

Companys collection rate during 2007 stood at

99.4% of the billings, equivalent to a 6.4 p.p. improvement in relation to the previous year, positively

impacted by the receipt of debts from previous periods.

The creation of the provision for doubtful accounts

in 2007 accounted for 2.8% of gross revenue with

electricity billings, presenting a decrease of R$145.5 million, or 2.1 p.p., in relation to the provision

created in 2006, as shown in the following table. This change was the result of the improvements in

the collection profile in 2007, which was achieved primarily through the regularization of the payment

of bills by public authorities and large customers, with a highlight for the reversal of provisions for

Supervias debts, in the amount of R$86.9 million, based on the background of regular payments by

this company and also the agreement entered into for the payment in installments of the existing debt.

There are no longer any provisions related to Supervias debt.

R$ MM 4Q07 4Q06 2007 2006

Billing 1,952 1,972 7,886 7,913

Collection 1,925 1,870 7,840 7,360

Collection Tax 98.6% 94.8% 99.4% 93.0%

Collection Tax

12 month moving average

92%

93%

94%

95%

96%

97%

98%

99%

100%

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2006 2007

2006 2007 Variation

PDD 345.0 199.5 145.5

7

Relation between Electricity Losses and Delinquency

Losses and delinquency are interconnected issues. "Losses is the general name given to the difference

between the electricity purchased by Light and sent to the network and the volume it bills. Delinquency

measures the amount of billed electricity that is not paid.

Lights strategy focuses on reducing losses, through operational (improved measurement, improved

shielding of networks, improved management of disconnections and reconnections) and public

awareness measures, in addition to initiatives carried out with other parties interested in the reduction

of "informality. In relation to delinquency, the goal is also to reduce it through a more effective control

of debts and initiatives for improving collection, in addition to streamlining the relationship with large

customers.

It is also important to note that a substantial portion of losses (approximately 40%) takes place in risk

areas, where it is impossible for the Company to provide services within minimum safety levels. In

these communities, we are beginning to develop special initiatives, together with state and local

authorities, in addition to community representatives, with a view to achieving results in the medium

term.

Both issues - losses and delinquency - are interconnected. For instance, suppose the Company

identified a group of customers illegally using electricity and decided to charge them the estimated

consumption for the last six months. The monthly statistics would show a significant increase in billed

electricity, therefore reducing the rate of losses. On the other hand, it is very unlikely that this group of

customers, which already do not pay for their usual electricity consumption, would pay this billing,

therefore increasing delinquency levels.

The above-mentioned approach has already been adopted by Light, certainly with the best of

commercial intentions; however, it distorted the historical series of losses. In view of the non-efficacy

of this practice, Lights new management decided to eliminate this approach, which initially resulted in

the growth in the rate of losses, and to focus on the reduction of delinquency.

Consequently, the importance of a combined analysis of these two indicators becomes clear. Between

December 2006 and 2007, Light presented, therefore, a 0.8 p.p. increase in losses in relation to the

wire load, which was more than offset by the reduction in the provision for doubtful accounts, which

declined from 5.4% of gross revenue with electricity billings in 2006 to 2.8% in December 2007.

Concurrently, the Companys collection rate presented a further substantial improvement, arising from

the receipt of overdue debts of large customers, expanding from 93% of total billings in December

2006 to 99.4% in 2007.

8

It is possible, therefore, to perceive the importance of the strategy adopted in 2007. For 2008, the

Company intends to intensify the initiatives for preventing losses, increasing its investments to R$220

million in 2008, compared to R$70 million in 2007.

Operating Quality

In 2007, Light maintained electricity service levels, investing R$54 million in network automation and

in increasing the capacity of circuits and transformers. In relation to performance, there was a marginal

expansion of the DEC as a result of adverse weather conditions in periods in which said conditions are

not usual, having an impact on this quality indicator. The FEC indicator remained at the same level of

2006, maintaining Light among the best distributing companies in Brazil in relation to its supply quality.

The Company will continue to pursue the improvement of its supply quality in order to remain among

the best distributing companies in Brazil, always keeping its quality indicators at satisfactory levels,

within the limits allowed by ANEEL. In order to ensure this performance, the Company will continue to

carry out its investment program in 2008, which will amount to R$55 million, being allocated in

preventive maintenance, network optimization and expansion in the capacity of circuits and

transformers.

Generation

The electricity sold in the free and regulated contracting environments in 4Q07 totaled 1,253.0 GWh,

4.9% higher than in 4Q06, as a result of the increase in sales to free customers.

In CCEEs Short-Term Market (Spot), estimated sales are expected to reach 26.5 GWh, 22.7% below

the volume verified in the same period of 2006 (34.3 GWh), as a result of the directing of electricity

sales from the Spot market to the free contracting market.

The global estimated volume of electricity sold this quarter grew 4.1% when compared to 4Q06, and is

expected to amount to 1,279 GWh. In 2007, according to CCEEs closing estimates, this volume should

reach 4,967 GWh, also 2.5% higher than the volume sold in 2006, as illustrated in the chart below.

ELC / EFC - 12 Month Moving Average

7.67

8.77

6.30

9.08

7.98

6.30 EFC

ELC

2007 2006 2005

9

Trading

In 2007, in the area of electricity trading, Light Esco operated in the direct purchase and sale of

electricity (as a trader), in the brokerage of purchase and sale electricity transactions (as a broker) and

as a representative and consultant for free consumers. In the trading activity, Grupo Light, through its

Light Esco subsidiary, traded 390 GWh related to a portfolio of 30 customers, as compared to only two

customers in 2006. In the brokerage activity, which began in 2007, the Company negotiated 1,200

GWh for a portfolio of ten customers.

In addition, the Company entered into long-term electricity sale agreements, effective from 2008

through 2010, equivalent to 40 average-MW. These agreements include customers such as AMBEV,

Dedini and Natura. The long-term agreements have ensured consolidated revenue of approximately

R$280 million for Light Esco over the next ten years. In the area of energy efficiency, three new

projects were approved involving central air-conditioning systems and the lighting of large commercial

centers, amounting to a total investment of R$3.5 million, with an average rate of return of 20%. The

process of connecting the new building of the "district cooling center, implemented and operated by

Light Esco at Centro Empresarial Rio Office Park, in the city of Rio de Janeiro, was initiated, and

operations are expected to begin in March 2008. New businesses are currently being analyzed,

including the offering of integrated electricity solutions for large-sized customers that carry out their

activities based on self-production facilities.

Tariff Adjustment

On November 6, 2007, ANEEL ratified the average adjustment of Lights tariff of 0.10% for the period

beginning November 7, 2007, including all consumer classes (residential, industrial, commercial, rural

and others).

The adjustment index, valid for the tariffs in the period between November 7, 2007 and November 6,

2008, consists of two parts: the structural component, which now is part of the tariff, with a 0.51%

adjustment; and the financial component, which is valid for the period of effectiveness of this tariff,

with a negative 0.41% adjustment.

LIGHT ENERGIA (GWh) 4Q07 4Q06 % 2007 2006 %

Regulated Contracting Environment Sales 1,140 1,113 2.4% 4,302 4,325 -0.5%

Free Contracting Environment Sales 113 81 39.4% 391 247 58.5%

Spot Sales (CCEE) 26 34 -22.7% 275 276 -0.4%

Total 1,279 1,229 4.1% 4,968 4,847 2.5%

10

The tariff adjustment process basically consists of transferring to the end-consumers the non-

manageable costs of the concession (the electricity purchased for distribution, industry charges and

transmission charges), since these are calculated in detail on an annual basis, whether in a year of

tariff adjustment or review. As for the manageable costs, their transfer in years of tariff adjustment (in

accordance with the rules set forth in the concession agreements of the distribution concessionaires) is

subject to the change in the IGPM less the X Factor, which is aimed at transferring to consumers the

annual efficiency gains of the concessionaire. The manageable costs of the concession are calculated in

detail only in years of tariff review (which in the case of Light SESA occurs every five years - the next

one is scheduled to November 2008).

Since part of the non-manageable costs decreased over the last 12 months, primarily due to the

reduction of the CCC (Fuel Consumption Account - a subsidy for thermal-based generation in the

Northern region of Brazil) and the devaluation of the US dollar (index used to adjust the purchases of

electricity from Itaipu Binacional), the adjustment of Lights tariffs was lower than inflation for the

period.

Lights end-consumers perceived an average 4.79% reduction in their electricity bills as from

November 7. This occurred because of the financial adjustment included in the tariff relating to the

period between November 7, 2006 and November 6, 2007, coupled with the recovery of tariff

differences of previous periods, which had a 5.4% positive effect on the tariff for that period.

With the adoption of the tariff realignment, based on which high- and low-voltage consumers had

different adjustment indices, the average adjustment for each level of voltage calculated by ANEEL

took place as presented in the following table:

Structural TRI 0.51%

Financial Adictionals

CVA -0.72%

Others 0.31%

Total 0.10%

Tariff Readjustment - 2007

Tension Level Real change over 2006 fares

Low tension (residential) -5.30%

A4 -3.30%

A3a -4.11%

AS -3.30%

A2 -5.29%

Average Value -4.79%

11

Financial Performance

Gross and Net Revenue

Consolidated

In 4Q07, gross operating revenue amounted to R$1,978.5 million, 4.2% lower than the revenue posted

in 4Q06, reflecting the 4.79% reduction on Lights average tariff ratified in November 2007. In 2007,

gross revenue amounted to R$8,138.4 million, 1.8% higher than in the same period of the previous

year, as shown in the following table:

Net operating revenue in the quarter amounted to R$1,077.1 million, 16.3% lower than the 4Q06

result, affected by the reconstitution of the provisions related to the charge relative to the increase of

the COFINS rate from 2% to 3%, in the amount of R$163 million. Net revenue in 2007 totaled

R$4,992.4 million, 0.8% higher than the net revenue of the previous year, as shown in the following

table:

Gross Revenue (R$ MM) 4T07 4T06 Var. % 2007 2006 Var. %

Distribution 1,900.9 2,002.8 -5.1% 7,855.2 7,766.2 1.1%

Generation 86.3 73.2 17.9% 311.8 271.6 14.8%

Comercialization 8.1 1.9 316.3% 36.3 5.1 615.9%

Others and Eliminations (16.8) (11.8) 42.4% (65.0) (45.7) 42.3%

Consolidated 1,978.5 2,066.2 -4.2% 8,138.4 7,997.2 1.8%

Net Revenue (R$ MM) 4Q07 4Q06 Var. % 2007 2006 Var. %

Distribution

Billed consumption 1,014.0 1,092.4 -7.2% 4,171.7 4,209.4 -0.9%

Network use (TUSD) 79.0 99.6 -20.7% 92.8 377.9 -75.4%

Short-Term (Spot) 44.8 47.0 -4.7% 64.5 103.8 -37.9%

Others 38.0 (9.7) 44.9 51.9 -13.5%

Subtotal (1) 1,175.9 1,229.2 -4.3% 4,374.1 4,743.1 -7.8%

Reversal of COFINS Provision (163.0) - - -

Subtotal (2) 1,012.9 1,229.2 -17.6% 4,374.1 4,743.1 -7.8%

- - - -

Generation - - - -

Generation Auction Sale 72.3 66.5 8.7% 135.1 241.4 -44.0%

Short-Term (Spot) 0.6 0.5 189.3 4.3 4302.3%

Others 1.5 0.7 114.3% 0.5 3.2 -84.4%

Subtotal (3) 74.3 67.6 9.9% 324.9 248.9 30.5%

- - - -

Comercialization - - - -

Energy Sales 4.8 - 66.2 -

Others 1.9 1.7 11.8% 11.8 4.4 168.2%

Subtotal (4) 6.7 1.7 294.1% 78.0 4.4 1672.7%

- - - -

Others and Eliminations (5) (16.8) (11.8) (65.0) (45.7)

Subtotal 1,240.1 1,286.8 -3.6% 4,712.0 4,950.7 -4.8%

- - - -

Total 1,077.1 1,286.8 -16.3% 4,712.0 4,950.7 -4.8%

(1) It includes "Not Billed", which represents the energy consumption of the period but billed in the next period

(2) Free and regulated contracting environment

(3) CCEE Short-Term Market

12

Distribution

Net Revenue in 4Q07 totaled R$1,012.9 million, representing

a 17.6% decrease compared to the same period in 2006.

This result was primarily affected by the reconstitution of the

provisions related to the charge relative to the increase of

the COFINS rate from 2% to 3%, in the amount of R$163

million, together with the average negative 4.79%

adjustment for Lights end-consumers tariff in effect as from

November 2007. Net of the above-mentioned provision reconstitution, net revenue would have totaled

R$1,175.9 million, 4.3% lower than in 4Q06, as a result of the 4.79% tariff reduction approved in

November 2007. In addition, the revenue for network use has also decreased by 20.7%, as a result of

the R$23.4 million reversal in October, due to the discount to which self-generating customers are

entitled in their tariffs accumulated since the 2006 IRT (Tariff Adjustment Index).

Net revenue for distribution in 2007 totaled R$4,755.2 million, 0.3% higher than in 2006, as a result of

the stable behavior of the billed consumption in the captive market, coupled with the flat tariff change

in 2007 in relation to 2006, until the tariff adjustment in November 2007.

Generation

Net revenue in 4Q07 totaled R$74.3 million, equivalent to a 9.9% increase compared to the same

period in 2006.

Net revenue of electricity sold (free and regulated contracting environments) totaled R$72.3 million,

8.7% higher than in 4Q06, as a result of the adjustment in regulated contract prices, in addition to the

4.1% increase in the volume sold between the periods and the growth in the selling prices in the free

market (based on the price in the spot market).

In CCEEs Short-Term Market (Spot, MRE and others), net revenue in 4Q07 totaled R$0.6 million,

20.0% higher than in 4Q06 (R$0.5 million). This result arose from the average price in the spot market

this quarter (R$196.1/MWh); i.e., 153.1% higher than in 4Q06, more than offsetting the 22.7% drop in

the volume of electricity sold in relation to 4Q06.

Net revenue in 2007 totaled R$271.4 million, presenting a 9.0% increase in relation to 2006, as a

result of the 2.5% growth in the volume of electricity sold and of the 8.9% increase in the average sale

price.

Net revenue for generation (free and regulated contracting environments) in 2007 totaled R$261.1

million, 8.2% higher than the revenue in 2006 (R$241.1 million), as a result of the increase in the

Net Revenue by Class - Captive

R$ MM - 2007

Residential

46%

Industrial

9%

Commercial

34%

Others

11%

1,+61

+89

383

1,956

13

volume and in the selling price in the free contracting environment (bilateral agreements) by 58.5%

and 29.7%, respectively.

Year-to-date, CCEEs Short-Term Market (Spot, MRE and others) net revenue totaled R$5.2 million,

20.9% higher than in 2006. This increase is explained by the increase of electricity prices in the Spot

market. The average price in the spot market in 2007 was R$90.8/MWh, equivalent to a 31% growth

when compared to 2006, which had a positive impact on agreements entered into over this period.

Trading

Net revenue in 4Q07 totaled R$6.7 million, equivalent to

a 294.1% increase compared to 4Q06. In 2007, net

revenue amounted to R$30.8 million, equivalent to a

staggering 600.0% growth in relation to 2006. This

amazing rate of expansion was primarily due to the

beginning of the electricity reselling transactions in 2007,

which accounted for 75.4% of the Companys annual net

revenue.

Costs and Expenses

Consolidated

Consolidated Operating Costs and Expenses

In 4Q07, operating costs and expenses increased 8.0% compared to 4Q06. In 2007, there was a 7.0%

decrease in costs and expenses primarily due to the effect of non-recurring provisions posted in 3Q06,

which had a negative impact of R$338.5 million during that year. Net of these provisions, the costs in

2007 would have been in line with the 2006 costs, despite the non-recurring effects on personnel and

outsourced services, as detailed in the following table.

Net Revenue - Light Esco

2007

Services

24.6%

Energy Sales

75.4%

Operating Costs and

Expenses (R$ MM)

4T07 4T06 Var. % 2007 2006 Var. %

Distribution (1,056.1) (977.9) 8.0% (4,119.2) (4,438.9) -7.2%

Generation (34.0) (29.7) 14.8% (127.9) (127.3) 0.5%

Comercialization (5.8) (0.9) 556.5% (27.8) (3.0) 814.4%

Others and Eliminations 15.7 8.6 82.3% 59.5 35.3 68.6%

Consolidated (1,080.2) (999.9) 8.0% (4,215.4) (4,533.9) -7.0%

* Includes depreciation

14

Distribution

In 4Q07, Light SESA experienced a 8.0% increase in its costs and expenses, as a result of the 11.3%

growth in non-manageable costs and expenses. In 2007, there was a 7.2% decrease in total costs

primarily due to the effect of non-recurring provisions posted in 3Q06, with a negative impact of

R$338.5 million in that year. Net of these provisions, 2007 costs would have been in line with 2006

costs, totaling R$4,119.2 million.

Non-Manageable Costs and Expenses

In the fourth quarter of 2007, non-

manageable costs and expenses totaled

R$765.9 million, equivalent to an 11.3%

growth in relation to the same period of

2006.

Net of the CVA effect, purchased electricity

amounted to R$699.2 million in the fourth

quarter of 2007, up 3.1% year-on-year. This

increase is explained by the readjustment in

purchase agreements, based on the IPCA and the IGPM, which occurred together with the tariff

adjustment in November 2007, making the average electricity purchase cost in 4Q07 reach

R$90.1/MWh, up from R$87.1/MWh in 4Q06.

The electricity purchase CVA in 4Q07 was a negative R$63.0 million, against a negative result of R$6.0

million in 2006. This R$57.0 million expansion was a result of the recognition of a R$30.4 million

liability in October 2007, arising from the acquisition of surplus electricity related to the period from

November 2005 through October 2006, and another R$17.0 million liability related to provisions arising

from the acquisition of surplus electricity for the period between November 2006 through October

2007, to be ratified in the 2008 tariff review.

LIGHT SESA

Costs and Expenses (R$ MM) 4T07 4T06 (%) 2007 2006 Var. %

Non-Manageable Costs and Expenses (765.9) (688.3) 11.3% (2,951.2) (2,878.4) 2.5%

Purchased Energy (Includes CVA and others taxes) (762.2) (685.2) 11.2% (2,930.9) (2,866.9) 2.2%

Others (Mandatory Costs) (3.7) (3.2) 16.3% (20.3) (11.5) 76.3%

Manageable Costs and Expenses (290.2) (289.6) 0.2% (1,168.0) (1,560.4) -25.1%

PMSO (159.3) (131.8) 20.8% (567.4) (533.1) 6.4%

Personnel (62.6) (57.0) 9.7% (256.4) (223.4) 14.8%

Material (4.0) (5.3) -24.0% (14.7) (17.1) -13.9%

Outsourced Services (77.0) (57.5) 33.9% (257.4) (224.4) 14.7%

Others (15.7) (12.0) 30.9% (38.9) (68.3) -43.0%

Provisions (61.4) (84.9) -27.7% (298.8) (732.1) -59.2%

Depreciation (69.6) (72.9) -4.6% (301.8) (295.2) 2.3%

Total Costs and Expenses (1,056.1) (977.9) 8.0% (4,119.2) (4,438.9) -7.2%

Purchased Energy - R$ MM

4th Quarter

678

699

29% 28%

25% 25%

30% 29%

16%

18%

4T06 4T07

NORTE FLU ITAIPU AUCTIONS OTHERS

15

The breakdown of purchased electricity in 4Q07 was as follows: R$205.7 million from auctions in 2005,

2006 and 2007; R$196.6 million from UTE Norte Fluminense; R$172.9 million from Itaipu; and

R$123.9 million from others sources.

In 2007, electricity purchase (without CVA)

amounted to R$2,828.9 million, 7.7% higher

than in 2006, as a result of the 1.5%

increase in the volume of purchased energy

and the 6.6% expansion of the average price

of electricity mix. The increase in price of

this mix is explained by the inclusion of

electricity purchased in the 2007 auction,

which accounted for 3.9% of the mix, which

was more expensive than the energy purchased in the 2005 and 2006 auctions; and the 8.6% increase

in Itaipus electricity price, the devaluation of the US dollar in the period notwithstanding.

In 2007, the electricity purchase CVA was a negative R$98.5 million, against a negative result of

R$236.5 million in 2006. This R$138.0 million decrease was caused by lower non-manageable costs in

comparison to the recognition of same in the tariff adjustment of November 2006.

The breakdown of purchased electricity in 2007 was as follows: R$801.5 million from UTE Norte

Fluminense; R$795.6 million from auctions in 2005, 2006 and 2007; R$743.1 million from Itaipu; and

R$488.5 million from other sources.

Manageable Costs and Expenses

The Company's manageable costs and expenses, represented by costs and expenses with personnel,

materials, outsourced services, provisions, depreciation and other costs and expenses, reached

R$290.2 million in 4Q07, in line with 4Q06.

The Companys PMSO (personnel, materials, services and others) costs and expenses amounted to

R$159.3 million in 4Q07, 20.8% higher than the R$131.8 million posted in 4Q06. This R$27 million

difference was due to the following factors: (i) the recognition of R$6.8 million related to the initiatives

for preventing losses, previously allocated under Capex; (ii) the expansion of the anti-delinquency

program, which accounted for R$3.2 million; (iii) non-recurring environmental costs of R$3.2 million;

(iv) an organizational restructuring program, with a non-recurring impact equivalent to R$2.8 million;

(v) a R$5.2 million higher provisioning for the profit sharing scheme (PLR) as a result of the EBITDA

growth posted in the year; and (vi) a culture incentive program in the amount of R$1.7 million with tax

benefits through the Rouanet Act, offset by income tax payable in the same amount.

Purchased Energy - R$ MM

Year

28% 29%

26%

26%

28%

28%

17%

16%

2,829

2,626

2006 2007

NORTE FLU ITAIPU AUCTIONS OTHERS

16

Provisions

1

(PDD, Provision for Contingencies and Others) in 4Q07 presented a 27.7% reduction

compared to 4Q06 as a result of: (i) the reversal of provisions totaling R$86.9 million, related to the

debt balance of Supervia, based on the background of regular payments during the year; (ii) the

reversal of provisions amounting to R$49.0 million, in 4Q06, related to the debt balance of the CEDAE,

local government authorities and low-voltage customers; and (iii) the provisioning, in 4Q07, in the

amount of R$73.9 million, related to a non-recurring adjustment of the review of the delinquency of

installments negotiated by the Companys previous Management.

In 2007, manageable operating costs and expenses totaled R$1,168.0 million, a 25.1% drop when

compared to 2006, a major highlight of which was, once again, the strong decrease in delinquency

levels, which had a direct impact on the level of provisions.

Year-to-date, PMSO totaled R$567.4

2

million, 6.4% higher than in 2006. This increase was primarily

due to: (i) changes in the allocation criterion of some initiatives for preventing losses, which were

previously allocated under Capex, with an R$18.5 million impact on operating expenses with

outsourced services; (ii) the voluntary termination (PDV) and organizational restructuring program,

with a non-recurring impact equivalent to R$9.5 million; and (iii) the R$14.2 million increase in

provisioning for the PLR, as a result of a higher EBITDA. Net of these effects, the 2007 PMSO would

have been R$7.9 million lower than in 2006.

In 2007, there was a R$433.4 million decrease in the level of provisions in relation to 2006, as a result

of the posting in 2006 of non-recurring provisions that had a negative impact on the result of that

period in the amount of R$338.5 million, and of anti-delinquency initiatives, such as the negotiation of

debt installment payments for large debtors, improving the collection profile. Supervias PDD reversal -

in the amount of R$86.9 million, as a result of this customers background of payment performance

since the agreement for the payment in installments of the existing debt entered into in April 2007 -

also had a positive impact. Net of the non-recurring postings in 2006 (R$338.5 million and the PDD

reversal of R$49.0 million carried out in 4Q06), and also the non-recurring posting of PDD in 4Q07

(Supervias R$86.9 million and R$73.9 million related to debt installments carried out by the

Companys previous management), the provisions in 2007 were R$130.4 million lower than in 2006;

i.e., equivalent to a 29.5% reduction.

1 As regards the provisions, it is important to note that the rate recognition is equivalent only to a small portion of the

actual amounts incurred by Light.

2

This value cannot be directly compared to the amount defined by ANEEL in the Rate Review process, under the item

Benchmark Company, as it does not include the remuneration and depreciation of non-electricity assets (commercial

and managerial buildings, vehicles, hardware, software, etc.

17

Generation

Light Energias costs and expenses totaled R$34.0 million in the quarter, comprising: purchased

electricity (33.9%), personnel (21.5%), materials and outsourced services (12.1%), others and

depreciation (33%). This quarter, generation costs increased by 14.8%. This expansion refers to the

higher provisioning for the PLR motivated by a higher consolidated EBITDA, as well as by the increase

in outsourced services.

Year-to-date, the costs and expenses with Generation amounted to R$127.9 million, in line with the

amount posted in 2006.

Trading

Light Escos operating costs and expenses totaled R$5.8 million in the quarter, 556.5% higher than in

4Q06. This increase was due to the startup of electricity trading in 2007, where there is a high

electricity purchase cost for resale, which in this quarter stood at R$4.5 million. Net of the electricity

purchase effect, due to the inexistence of such activity in 2006, the costs and expenses would have

been 39.2% higher, arising primarily from the expansion in costs with personnel, materials and

outsourced costs as a result of the increase in the scope of activities.

In 2007, operating costs and expenses amounted to R$27.8 million, 814.4% higher than in 2006. This

increase was once again a result of the beginning of the electricity reselling activities in 2007, which

accounted for 80% of the operating expenses for the year, net of the R$5.5 million extraordinary

expenses with the lease of generators for the local government of Rio de Janeiro during the Pan-

American Games, which had a corresponding revenue amount that took place in 3Q07.

Operating Costs and Expenses - R$ MM 4T07 4T06 (%) 2007 2006 Var. %

Personnel (7.3) (5.4) 34.4% (25.4) (23.4) 8.6%

Material and Outsourced Services (4.1) (3.2) 28.7% (14.1) (13.2) 7.0%

Purchased Energy (CUSD) (11.5) (10.5) 9.2% (42.9) (41.0) 4.6%

Depreciation (6.3) (6.2) 1.4% (25.3) (25.1) 0.6%

Others (includes provisions) (4.8) (4.3) 12.4% (20.2) (24.6) -17.8%

Total (34.0) (29.7) 14.8% (127.9) (127.3) 0.5%

Operating Costs and Expenses - R$ MM 4T07 4T06 (%) 2007 2006 Var. %

Personnel (0.5) (0.4) 22.7% (2.0) (1.1) 71.6%

Material and Outsourced Services (0.4) (0.2) 73.2% (1.2) (0.9) 32.4%

Purchased Energy (4.5) - - (17.9) - -

Depreciation (0.2) (0.2) 0.9% (0.8) (0.8) 7.4%

Others (includes provisions) (0.1) (0.0) 286.4% (5.9) (0.2) 2686.8%

Total (5.8) (0.9) 556.5% (27.8) (3.0) 814.4%

18

EBITDA

Consolidated

Consolidated EBITDA for the fourth quarter of 2007 amounted to R$73.0 million, with a 80.1%

decrease in relation to the same period of 2006, primarily as a result of the reconstitution of the

PIS/COFINS provision, in the amount of R$163.0 million, and the posting, this quarter, of R$47 million

liabilities related to the distributing companys acquisition of surplus electricity between November

2005 and October 2006 (R$30.4 million) and from November 2006 through October 2007 (R$17

million). Net of these effects, EBITDA in the 4

th

quarter of 2007 would have totaled R$283.4 million,

22.7% lower than EBITDA in the same period of 2006. The EBITDA margin in the quarter stood at

6.8% and cash EBITDA totaled R$170.5 million.

In 2007, consolidated EBITDA totaled R$1,105.0 million, equivalent to a

49.7% growth compared to the EBITDA recorded in 2006. In 2006, EBITDA

was impacted by the extraordinary, non-recurring provision of R$338.5

million. Net of this effect, 2007 EBITDA was 2.7% higher than in 2006.

Consolidated EBITDA margin in the year stood at 22.1% and cash EBITDA

totaled R$1,475.3 million.

EBITDA - 2007/2006 - R$ Million

-

1,076

738

1,105

(49)

(23)

338

101

EBITDA -

2006

Provisions -

Jul06

EBITDA -

2006 w/out

provisions

Net Revenue Manageable

Costs (PMSO)

Provisions EBITDA -

2007

EBITDA per segment*

2007

Distribution

84.5%

Generation

15.2%

Comercializ.

0.3%

*Does not consider eliminations

EBITDA Consolidado - R$ MM 4Q07 4Q06 Var.% 2007 2006 Var.%

Distribution 26.4 324.2 -91.9% 937.8 599.4 56.5%

Generation 46.5 44.2 5.4% 168.7 146.7 15.0%

Comercializ. 1.1 1.0 11.4% 3.9 2.2 77.3%

Outros e eliminaes (1.1) (3.2) -65.7% (5.4) (10.3) -47.6%

Total 73.0 366.2 -80.1% 1,105.0 737.9 49.7%

EBITDA Margin (%) 6.8% 28.5% - 22.1% 14.9% -

19

Distribution

The Distributing Companys EBITDA in the fourth quarter totaled R$26.4 million, 91.9% lower than the

amount posted year-on-year. This decrease was primarily due to: (i) reconstitution of the provision

related to the charge relative to the increase of the COFINS rate, carried out in June 2007, in the total

amount of R$163.0 million; (ii) the non-recurring adjustment, amounting to R$73.9 million, related to

the review of the delinquency of installments negotiated by the Companys previous Management; (iii)

the provision reversals carried out in 4Q06, amounting to R$49.0 million, related to the debt balance of

the CEDAE, local government authorities and low-voltage customers; (iv) the posting, this quarter, of

R$47,4 million liabilities related to the acquisition of surplus electricity between November 2005 and

October 2007; (v) the reversal of R$23.4 million assets related to the discount to which self-generating

customers are entitled; and (vi) the provision, in the amount of R$20.0 million, related to the ANEELs

Notice of noncompliance with the classification criteria for low-income customers. Supervias PDD

reversal, in the amount of R$86.9 million, had a positive impact on the Companys EBITDA in the

quarter. Net of these non-recurring effects, recurring EBITDA in the quarter would have totaled

R$266.8 million, 3.1% lower than recurring EBITDA in 4Q06.

Cash EBITDA measured over the fourth quarter of 2007 totaled R$123.8 million, 74.3% lower than the

amount posted in the same period of the previous year. This result is explained by the same factors

described in the previous paragraph, in addition to a 16.3% reduction in regulatory assets between the

periods.

The distributing companys EBITDA in 2007 amounted to R$937.8 million, 56.5% higher than in 2006.

Net of the non-recurring adjustment in the amount of R$73.9 million, related to the review of the

delinquency of installments negotiated by the Companys previous Management, and the reversal of

the provision of debts related to Supervia, in the amount of R$86.9 million, the distributing companys

EBITDA in 2007, on a recurring basis, totaled R$924.8 million. This result was 4.0% higher than the

recurring EBITDA of R$888.9 million (adjusted by the reversal of provisions carried out in 4Q06, in the

amount of R$49.0 million) posted in 2006, primarily as a result of the improvement in the collection

profile.

The distributing company's cash EBITDA

3

, measured in 2007, totaled R$1,308.1 million, 10.0% higher

than the amount posted in the previous year.

3

Takes into account the cash effect of the change in the regulatory asset.

20

Generation

Light Energias EBITDA in 4Q07 amounted to R$46.5 million, up from the R$44.2 million recorded in

4Q06. This 5.4% growth is a result of the 9.8% addition in 4Q07 net revenue compared to 4Q06, which

was impacted by the 52.8% and 133.8% price increases in bilateral agreements (R$/MWh) and in the

selling price in the spot market, respectively. Costs have not kept up with this growth in absolute

terms, despite the 14.8% increase between the periods. Quarterly EBITDA margin stood at 62.6%, 2.7

p.p. lower than in 2Q06, as a result of the larger growth in net revenue than in EBITDA.

In 2007, generation-related EBITDA totaled R$168.7 million, 15% higher than in 2006, as a result of

the average 8.9% increase in auction, bilateral agreement and spot prices. The accumulated EBITDA

margin in 2007 stood at 62.2%, 3.3 p.p. higher than in 2006.

Trading

Light Escos EBITDA totaled R$1.1 million in 4Q07 compared to R$1.0 million recorded in 4Q06,

equivalent to an 11.4% increase. The EBITDA growth is largely due to the beginning of electricity sales

operations, which resulted in an incremental net revenue of R$4.8 million, tripling the business value of

the trading company. EBITDA margin in the quarter stood at 16.8%, 43.2 p.p. lower than in 4Q06. This

drop in the margin is typical of the brokerage activity, due to the inclusion of a service with higher

financial volume, but with a lower margin.

Accumulated EBITDA in 2007 totaled R$3.9 million, 77.3% higher than in 2006, once again as a result

of the beginning of electricity purchase and sale activities.

Consolidated Financial Results

Financial Result - R$ MM 4Q07 4Q06 (%) 2007 2006 (%)

Financial Revenues 60.0 93.4 -35.7% 247.6 415.8 -40.4%

Income - financial investments 10.8 16.4 -34.0% 43.4 65.3 -33.6%

Monetary and Exchange variation 33.4 44.8 -25.3% 128.8 205.9 -37.4%

Swap Operations 0.9 0.3 192.3% 15.5 21.8 -29.1%

Others Financial Revenues 14.9 31.9 -53.4% 60.0 122.8 -51.1%

Financial Expenses (159.5) (183.6) -13.1% (563.6) (741.1) -24.0%

Interest over loans and financing (56.2) (86.4) -34.9% (268.9) (394.9) -31.9%

Monetary and Exchange variation (25.3) (55.3) - (23.7) (140.3) -

Braslight (private pension fund) (39.1) (26.4) 48.0% (106.8) (80.0) 33.5%

Swap Operations (10.2) (8.1) 25.4% (95.9) (70.7) 35.6%

Others Financial Expenses (28.7) (7.4) 289.1% (68.2) (55.2) 23.5%

- - - -

Subtotal (99.5) (90.2) 10.2% (316.0) (325.3) -2.9%

- - - -

Reversal of PIS/COFINS Provision (239.3) - - -

- - - -

Total (338.8) (90.2) - (316.0) (325.3) -2.9%

21

Financial Results in the quarter amounted to a negative R$338.8 million, against a negative result of

R$90.2 million in the same period of 2006, as a result primarily of the reconstitution of the provision

related to the charge of taxes, in the amount of R$239.3 million. Net of this non-recurring effect, the

financial result was a negative R$99.5 million, 10.2% lower than the result in 4Q06.

In 2007, the financial result was a negative R$316.0, 2.9% lower than the expense recorded in 2006.

This improvement was due to the reduction in financial charges as a result of the smaller debt, the

reduction in the average cost of debt and the negative effect in 2006 of the 8.6% devaluation of the US

dollar over a R$1,374.6 million exposure (December 2006) in foreign-currency denominated debt.

Indebtedness

The Companys gross debt presented a 9.9% increase in relation to the end of September, equivalent

to R$176.2 million, primarily due to the raising of funds in the quarter from Bradesco and the BNDES,

in the amount of R$450.0 million and R$242.6 million, respectively, the former with the purpose of

settling the debt with Deutsche Bank (Credit Linked Notes) and strengthening the cash position, and

the latter for financing CAPEX projects. On the other hand, the settlement of the debt with Deutsche

Bank, the conversion of debentures from the 4

th

issuance, the reduction of the swap operations (due to

the smaller debt in foreign currency), and the amortization of the margin recovery line with the BNDES

(RTE) resulted in the reduction of debt by R$306.9 million, R$82.5 million, R$45.8 million and R$71.1

million, respectively.

R$ MM Short Term % Long Term % Total %

Brazilian Currency 103.7 5.3% 1,691.4 63.1% 1,795.2 92.0%

Debenture 1st Issue 17.2 0.9% 23.0 1.2% 40.2 2.1%

Debenture 4th Issue 5.6 0.3% 5.6 0.3%

BNDES Rationing 243.5 12.5% 243.5 12.5%

Debenture 5th. Issue 72.7 3.7% 950.0 48.7% 1022.7 52.4%

CCB Bradesco 460.6 460.6 23.6%

Financial operations "Swap" 8.6 0.4% 1.6 0.1% 10.1 0.5%

Others 5.3 0.3% 7.1 0.4% 12.4 0.6%

Foreing Currency 23.5 1.2% 133.2 6.8% 156.8 8.0%

National Treasury 17.0 0.9% 125.1 6.4% 142.1 7.3%

Import Financing 5.2 0.3% 6.4 0.3% 11.6 0.6%

BNDES Import Fin. 1.4 0.1% 1.8 0.1% 3.1 0.2%

Gross Debt 127.3 6.5% 1,824.7 93.5% 1,951.9 100.0%

Cash 490.2

Net Debt 127.3 1,824.7 1,461.7

Braslight (pension fund) 891.9 891.9

Gross Debt + Braslight 127.3 2,716.6 2,843.8

22

Net Debt (ex-Braslight)

(R$ million)

2,540

1,217

1,462

4Q06 3Q07 4Q07

-42,4%

Net debt presented a 20.0% increase in the quarter when compared to September 2007. In relation to

the end of 4Q06, net debt presented a significant 42.4% reduction as a result of the conversion of

debentures from the 4

th

issuance, with the equivalent R$800 million decrease in gross debt, in addition

to the strong cash generation, which was partially used for amortizing debts.

The average maturity of the debt was also benefited by the

renegotiation of short-term debts, being extended from

4.66 years to 4.77 years. The average cost stood at

12.17% (a 0.23 p.p. reduction in relation to September

2007) for debt denominated in local currency and at 6.51%

(a 2.06 p.p. reduction) in US dollars for debt denominated

in foreign currency. The exposure to debt in foreign

currency was also substantially reduced during the year, from 42.5% to 8.1% of the total, with the

payment in January of R$1,466.0 million of the debts related to the "Credit Agreement in Brazilian

Reals and the "Amended and Restated Indenture and in October of R$306.9 million of the debt with

Deutsche Bank.

Light adopts a hedging policy based on disbursement

cash flow over 24 months. Based on this policy, the

exposure in foreign currency decreased from 8.1% to

5.6% of the total debt on December 31, 2007.

Net Income

Light posted a net income of R$229.2 million in this quarter, equivalent to a 144.1% increase when

compared to 4Q06, as a result of the non-recurring effect of the recognition of the accumulated

deferred tax credits, in the amount of R$523.6 million, despite the reconstitution, in this quarter, of the

provisions related to the increase in the calculation basis of said taxes and to the growth of the COFINS

rate from 2% to 3%, totaling R$402.3 million (R$239.3 million posted in Financial Result and R$163.0

million recorded under Gross Revenue Deductions), generating a net tax effect of R$265.5 million.

Net income in 2007 totaled R$1,077.2 million, partially due to the recognition of accumulated deferred

tax credits in the amount of R$851.2 million, after a long period of accounting and tax losses (the

Company accrued taxable income over a period of three (3) years, and is again recognizing deferred

taxable credits on provisions, usually referred to by tax experts as "temporary differences). Net of

these non-recurring effects, net income would have been R$226.0 million compared to R$150.5 million

in 2006. Still net of the effect of the provisions carried out in July 2006, which had a negative R$292.8

million impact on income that year, income on a recurring basis in 2007 would have been 58.8%

higher.

Indebtness

(Brazilian Currency x Foreign)

57.5%

72.7%

92.0%

42.5%

27.3%

8.0%

4Q 2006 3Q 2007 4Q 2007

Brazilian Currency Foreign Currency

23

Investments

Up to December 2007, R$354.7 million were invested in

capital expenditures and improvements. In distribution,

the main highlights were investments in the development

of distribution networks, primarily involving new

connections, capacity increases and corrective

maintenance, totaling R$233.6 million; quality

improvement (structure optimization and preventive

maintenance) in the amount of R$30 million; and

initiatives for preventing losses with CAPEX totaling R$48 million. In the area of generation, there were

investments amounting to R$18.3 million in transmission network development and quality

improvement.

New Projects in Generation

PCH Paracambi: small hydroelectric power plant, with 25 MW of installed capacity, 20.4 average-

MW of physical guarantee, located at the Ribeiro das Lajes river, in the municipality of Paracambi

(state of Rio of Janeiro), downstream from the Lajes Complex. The project is currently in the process of

obtaining the Installation License, and measures are being taken to engage the EPC in the construction

of the power plant. In addition, there are ongoing activities for the acquisition of lands necessary to

build the reservoir. Works are expected to begin in the first half of 2008, and plant startup is expected

to take place in 2010, with a construction term of 24 months and an estimated cost of R$100 million.

The Project was qualified by the BNDES in the second half of 2007. The trading of this power plant is

being carried out by Light Esco.

PCH Lajes: small hydroelectric power plant, with 17 MW of installed capacity, whose physical

guarantee is currently being defined. The PCH is located at the Lajes Complex, using the structure of

the idle Fontes Velha Plant. The Basic Project of the power plant has been submitted to the approval of

ANEEL. The environmental license process with FEEMA was initiated in 2007. We estimate that the

required environmental licenses may be obtained within a short period in view of the particular features

of this project, since a new reservoir will not be built. The estimated date for the beginning of

operations is in 2010, with an expected cost of R$56 million, which includes the construction of Tunnel

2 connecting the Lajes Reservoir to the Valve House.

- UHE Itaocara: hydroelectric power plant with 195 MW of installed capacity and 110 average-MW of

guaranteed energy, located at the Paraba do Sul river, in Itaocara, in the state of Rio de Janeiro, near

Lights concession area. The estimated date for the beginning of operations is in 2012, with a

construction period of 36 months and an estimated cost in the amount of R$700 million, as a result of

Investiment in Aquisitions & Improvements

on Fixed Assets (R$ MM)

230.0

267.3

66.0

322.2

354.7

63.7 19.1

22.3 7.1

1.3

2006 2007

Distribution Administration Generation Commercialization

24

the revaluation, carried out in 2007, of the engineering project and environmental costs of the UHE

Itaocara. Recently, the environmental license process with IBAMA resumed with its request to issue a

Statement of Reference for the studies.

Cash Flow

In 2007, Light presented a negative cash flow amounting to R$204.9 million, primarily due to:

- the amortization of R$753.7 million of loans and financing payments; and

- the increase in the level of investments made.

These effects were offset by the higher cash generation from operations, amounting to R$232.5 million,

arising from the reduction in the level of provisions, in addition to the increase in net income and in

assets.

R$ MM 2006 4Q07 2007

Cash in the beginning of the period 413.6 55S.5 695.1

Cash from operating activities 1,29S.2 450.7 1,530.7

Net income (150.5) 229.2 1,077.2

Provision for Delinquency 296.8 (12.7) 171.5

Depreciation and Amortization 321.1 76.0 328.0

Assets (increase) decrease 149.7 73.8 230.2

Liabilities increase (decrease) (319.9) 143.8 128.9

Others 1,001.1 (59.5) (405.0)

Financing Activities {650.9) {320.S) {1,271.7)

Dividens payment - (518.0) (518.0)

Capital !ncrease - - -

Finance Obtained 9.1 692.5 1,693.6

Debt Service and Amortization (660.1) (495.3) (2,447.3)

Investiment Activities {365.7) (198.2) (463.9)

Share participations - - 28.0

Concession !nvestiments (376.7) (201.8) (488.3)

Special Obligations - Consumer's Contributions 11.0 3.6 (3.6)

Cash in the end of the period 695.1 490.2 490.2

25

Corporate Governance and Capital Markets

The capital stock of Light S.A. comprises 203,462,739 common shares, with no par value. The

controlling group, Rio Minas Energia (RME), holds 52.2% of the capital stock, with the remaining shares

outstanding, in accordance with the following shareholding structure:

The Company's shares have been listed on Bovespa's Novo Mercado since July 2005, granting special

rights to minority shareholders, based on the best corporate governance practices and on transparency

and equity principles, important milestones for the relationship with the capital markets.

The Companys Extraordinary General Meeting held on October 19, 2007 approved the reverse split of

all shares representing the Companys capital stock, at the ratio of one thousand (1,000) shares for

one (1) share. As of December 3, 2007, the shares began to be traded at a unit price and with a

standard lot of 100 shares. The remaining fractions of shares from the reverse split process were sold

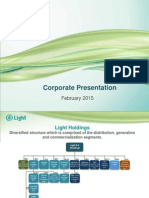

at an auction held on December 14, with a price set to R$26.30 per share.

On November 21, 2007, in compliance with its dividends policy, Light paid R$518 million in dividends

related to the results assessed in the first half of the year to the shareholders of record on October 26,

2007. The amount distributed was equivalent to R$2.54 per lot of 1,000 shares on that date.

AGC

Andrade Gutierrez

Concesses

LUCE

LUCE do Brasil

Fundo de Investimento

em Participaes

PCP

PCP Energia

Participaes

RME

Rio Minas Energia

Participaes S.A.

LIGHT S.A.

Countrys

biggest

individual

electricity

distributor.

Andrade Gutierrez

Groups division

that invests in

public services

concessions.

Brazilian private

investors group

(includes

Braslight).

Private Equity

Fund that

invests

in the Brazilian

electric sector.

25% 25% 25% 25%

52.2%

BNDESPAR

MARKET

33.7%

14.1%

Free Float: 47.8%

CEMIG

Companhia Energtica

de Minas Gerais

26

In the quarter, Lights shares remained in line with both the closing price of the third quarter of the

year and with the 0.6% appreciation recorded by the electric power index (IEE). Ibovespa showed a

growth of 5.7%, even with the market fluctuations that occurred during the quarter. Average daily

volume traded this quarter amounted to R$8.4 million, 13.5% higher than the amount traded in the

previous quarter.

In 2007, Lights shares appreciated 34.0%, showing the perception, by the market, of the

improvement in the Companys management after the entry of the new controlling group in the second

half of 2006. This rate was higher than the 24.0% presented by IEE; however, it was lower than the

44.0% appreciation of Ibovespa. In 2007, average daily volume traded amounted to R$8.3 million,

39.4% higher than the volume traded in 2006.

The following chart presents the evolution of Lights shares in 2007.

BOVESPA (spot market) - LIGT3

Daily Average 4Q07 3Q07 2Q07 1Q07 4Q06

Number of shares traded (Million) 274.41 263.26 294.15 388.13 303.77

Number of Transactions 463 340 360 479 429

Traded Volume (R$ Million) $8.4 $7.4 $8.4 $9.3 $6.1

Quotation per lot of 1000 shares: $28.65 $28.52 28.61 22.76 21.37

Share Valuing 0.5% -0.3% 25.7% 6.5% 45.6%

IEE Valuing 0.6% -3.2% 26.7% 0.2% 16.9%

Ibovespa Valuing

5.7% 11.2% 18.7% 3.0%

22.0%

Light x Ibovespa x IEE

Jan/07 = 100 until 12/28/07

60

80

100

120

140

160

180

D

e

c

-

0

6

J

a

n

-

0

7

F

e

b

-

0

7

M

a

r

-

0

7

A

p

r

-

0

7

M

a

y

-

0

7

J

u

n

-

0

7

J

u

l

-

0

7

A

u

g

-

0

7

S

e

p

-

0

7

O

c

t

-

0

7

N

o

v

-

0

7

D

e

c

-

0

7

Light

34%

Ibovespa

44%

IEE

24%

R$/stock

01/01/07 21,37

12/28/07 28,65

27

Recent Events

Change of one of the controlling shareholders: On February 12, 2008, the Extraordinary

General Meeting of Equatorial Energia S.A. approved the merger of PCP Energia, a company that

holds 13.06% of Lights shares through RME, into the Equatorial group. As from this moment,

Equatorial is part of the controlling group of Light - RME. Said merger does not represent a

transfer of control since both companies, PCP and Equatorial, belong to the same controlling

company.

Dividend Proposal: On February 13, 2008, the Companys Board of Directors approved the

proposal of dividend payments in the amount of R$721,463 thousand, to be confirmed by the

Annual General Meeting, to be held on March 17, 2008. It is important to note that the proposed

value includes dividends amounting to R$518 million voted on September 28, 2007 and paid on

November 21, 2007, by way of prepayments on the results for the period ended December 31,

2007. The distribution of dividends is equivalent to 67.0% of the net income posted in the year.

Reverse Share Split: In order to continue carrying out the reverse split of the Companys

shares, the respective selling values of the fractions of shares auctioned on December 14 (price

fixed at R$26.30 per share) were credited in the checking accounts of fraction shareholders on

January 4, 2008, according to the Notice to Shareholders dated January 3, 2008.

Corporate Sustainability Index (ISE): The Company was selected to take part in Bovespas

Corporate Sustainability Index (ISE) portfolio, with a period of effectiveness from December 2007

through November 2008. The ISE is an index created by the Bovespa which is aimed at

identifying the companies with the best social and environmental responsibility and corporate

sustainability in the market.

6

th

Issuance of Debentures: In order to reduce the cost of the debt arising from the 5th

issuance of debentures, Light's Board of Directors approved, in a meeting held on December 21,

2007, the issuance of R$400 million in debentures non-convertible into shares aimed at carrying

out the prepayment of part of the issuance of R$1 billion in debentures from the 5th issuance.

The coordinator of the operation will be the syndicate comprising the banks Ita BBA, Bradesco,

Unibanco, Citibank and BNP Paribas.

The remaining R$600 million from the 5

th

issuance of debentures will have its cost reduced, from

the CDI + 1.50% p.a. to CDI + 1.35% p.a.

28

Automatic Debit Campaign: In order to improve the collection and the predictability of bill

payments and to decrease banking costs, Light created the campaign "Dbito Automtico Light -

SORTE DE QUEM TEM (Lights Automatic Debit - THE LUCK OF THOSE WHO HAVE IT), which will

raffle notebooks and LCD TVs to customers joining the automatic debit system. The promotion

will last four months (up to March 2008).

Disclosure Program

Forward-looking Statements

The information on the Companys operations and its Managements expectations regarding its future performance was not

reviewed by independent auditors.

Statements about future events are subject to risks and uncertainties. These statements are based on beliefs and assumptions of

our Management, and on information currently available to the Company. Statements about future events include information

about our intentions, beliefs or current expectations, as well as of the Company's Board of Directors and Officers. Exceptions

related to statements and information about the future also include information about operating results, likely or presumed, as

well as statements that are preceded by, followed by, or including words such as "believes", "might", "will", "continues",

"expects", "estimates", "intends", "anticipates", or similar expressions. Statements and information about the future are not a

guarantee of performance. They involve risks, uncertainties and assumptions because they refer to future events, thus

depending on circumstances that might or might not occur. Future results and creation of value to shareholders might

significantly differ from the ones expressed or suggested by forward-looking statements. Many of the factors that will determine

these results and values are beyond LIGHT S.A.'s control or forecast capacity.

Teleconference

Brazil: (55) 11 - 4688-6301

USA: +1(888)700 0802

Other countries: +1 (786) 924-8430

Access code: Light

1st Light and Investor Meeting

Lajes Complex - Rio de Janeiro

Schedule

Date:03/18/2007, tuesday

Time: 09:00 a.m. to 06:00 p.m.

Address:Lajes Complex - Barra do Pira - RJ

02/15/2008, friday, at 02:30 p.m. (Braslia) and at 11:30 a.m. (Eastern time),

with simultaneous translation to English

Webcast: link on site www.light.com.br (portuguese and english)

Access conditions:

Conference Call - Dial number:

29

EXHIBIT I

Income Statement per Company - R$ million

LIGHT SESA 4Q07 4Q06 %

Operating Revenue 1,900.9 2,002.8 -5%

Deductions from the operating revenue (888.0) (773.6) 15%

Net operating revenue 1,012.9 1,229.2 -18%

Operating expense (1,056.1) (977.9) 8%

Operating result (43.2) 251.3 -117%

EBITDA 26.4 324.2 -92%

Equity equivalence (13.3) 22.3 -

Financial Result (314.4) (104.6) -

Non operating result 4.4 (0.6) -

Result before taxes and interest (366.4) 168.4 -318%

Net Income 210.7 69.5 203%

EBITDA Margin

2.6% 26.4% -

LIGHT ENERGIA 4Q07 4Q06

%

Operating Revenue 86.3 73.2 18%

Deductions from the operating revenue (12.0) (5.5) 116%

Net operating revenue 74.3 67.7 10%

Operating expense (34.0) (29.7) 15%

Operating result 40.3 38.0 6%

EBITDA 46.5 44.2 5%

Equity equivalence - - -

Financial Result (9.2) (8.2) -13%

Non operating result 0.2 - -

Result before taxes and interest 31.3 29.8 5%

Net Income 20.8 26.8 -22%

EBITDA Margin

62.6% 65.3% -

LIGHT ESCO 4Q07 4Q06

%

Operating Revenue 8.1 1.9 316%

Deductions from the operating revenue (1.4) (0.3) 437%

Net operating revenue 6.7 1.7 297%

Operating expense (5.8) (0.9) 557%

Operating result 0.9 0.8 14%

EBITDA 1.1 1.0 11%

Equity equivalence - - -

Financial Result 0.1 0.1 34%

Non operating result - - -

Result before taxes and interest 1.0 0.9 16%

Net Income 0.8 0.6 19%

EBITDA Margin

16.8% 60.0% -

30

EXHIBIT II

Consolidated Income Statement

Consolidated - R$ MM 2Q07 2Q06 9M07 9M06

OPERATING REVENUE 1,978.5 2,066.2 8,138.4 7,997.2

DEDUCTIONS FROM THE REVENUE (901.3) (779.4) (3,146.0) (3,046.5)

NET OPERATING REVENUE 1,077.1 1,286.8 4,992.4 4,950.7

OPERATING EXPENSE (1,080.2) (999.9) (4,215.4) (4,533.9)

Personnel (70.8) (65.6) (286.8) (256.9)

Material (4.2) (5.7) (15.6) (18.5)

Outsourced Services (81.5) (60.8) (273.2) (238.3)

Purchased Energy (762.0) (684.0) (2,927.4) (2,862.6)

Depreciation (76.0) (79.3) (328.0) (321.1)

Provisions (61.4) (84.9) (298.8) (738.1)

Others (24.3) (19.5) (85.7) (98.6)

OPERATING RESULT() (3.1) 286.9 777.0 416.8

EBITDA () 73.0 366.2 1,105.0 737.9

EQUITY EQUIVALENCE 0.0 0.0 (0.0) (1.5)

FINANCIAL RESULT

(338.8) (90.2) (316.0) (325.3)

Financial Income 60.0 93.4 247.6 415.8

Financial Expenses (398.8) (183.6) (563.6) (741.1)

NON OPERATIONAL RESULT

4.6 (0.6) 11.3 8.6

Non-Operating Income 10.1 2.0 17.9 4.9

Non-Operating Expenses (5.5) (2.6) (6.6) 3.7

RESULT BEFORE TAXES AND INTEREST (337.2) 196.1 472.4 98.5

SOCIAL CONTRIBUTIONS & INCOME TAX 566.4 (102.2) 607.7 (249.0)

DEFERRED INCOME TAX 0.0 0.0 (2.9) 0.0

NET PROFIT/LOSS 229.2 93.9 1,077.2 (150.5)

() Operation Result, Administration vision = Operating Result, accounting norms (Item 1.9.7 of Notice CVM -

01/2007) + financials (net financial expenses + equity pick-up)

() EBITDA = Operating Result, Administration vision + depreciation and amortization. Not reviewable by the

external audit

31

EXHIBIT III

Consolidated Balance Sheet

Balance Sheet Consolidated - R$ MM

ASSETS 12/31/2007 9/30/2007

Circulating 2,918.3 2,597.0

Cash & Cash Equivalents 490.2 558.5

Credits 2,103.2 1,787.4

Inventories 13.3 15.9

Others 311.7 235.1

Realizable in the Long Term 1,978.7 1,737.6

Miscellaneous Credits 1,556.4 1,200.5

Others 422.4 537.2

Permanent 4,039.6 3,971.5

Investments 13.2 13.3

Net Fixed Assets 3,702.1 3,604.2

Deferred Charges 53.3 165.6

Intangible 271.1 188.4

Total Assets 8,936.6 8,306.1

LIABILITIES 12/31/2007 9/30/2007

Circulating 1,737.1 2,080.2

Loans and Financing 27.4 98.9

Debentures 65.3 52.8

Suppliers 488.4 550.0

Taxes, Fees and Contributions 305.6 262.7

Dividends to pay 203.5 518.0

Provisions 169.5 177.6

Others 477.5 420.1

Long-Term Liabilities 4,528.1 3,779.2

Loans and Financing 831.4 450.4

Debentures 978.6 1,072.9

Provisions 1,361.7 876.6

Others 1,356.4 1,379.3

Future Fiscal Year Results 3.2 3.1

Net Assets 2,668.3 2,443.7

Realized Joint Stock 2,220.4 2,138.5

Capital Reserves 53.9 -

Accumulated Profit/Loss (683.1) -542.9

Accumulated Profit/Loss of Exercise 1,077.2

Total Liabilities

8,936.6 8,306.1

32

EXHIBIT IV

Regulatory Assets and Liabilities

Light in Numbers

OPERATING INDICATORS 12/31/2007 12/31/2006 Var. %

N of Consumers (thousands) 3,881 3,802 2.1

N of Employees 3,907 4,152 -5.9

Average provision tariff - R$/MWh 409.8 414.3 -1.1

Average provision tariff - R$/MWh (w/out taxes) 279.1 279.4 -0.1

Average energy purchase cost R$/MWh* 88.0 87.8 0.2

Generation Capacity (MW) 855 855 -

Assured Energy (MW) 537 537 -

Generation (GWh) 1,046 1,271 -17.7

Charge Factor 66.6% 65.4% -

* Includes net energy purchase/sell in the spot market

REGULATORY ASSETSR$ MM

12/31/2007 12/31/2006 12/31/2007 12/31/2006

Customers, Concessionaires and Permissionaires 95,114 248,124 - 128,087

Extraordinary Tariff Recomposition 37,866 152,260 - 98,318

Free energy 16,354 67,914 - 29,769

Tariff Readjustment 28,862 20,350 - -

Tariff Readjustment - TUSD 12,032 7,600 - -

Despesas Pagas Antecipadamente 273,640 234,298 137,988 315,959

CVA 45,909 127,562 1,898 12,615

PISande COFINS 6,079 68,618 - -