Вам также может понравиться

- PROBLEM 2 - Two Sole Proprietors Form A Partnership PROBLEM 2 - Two Sole Proprietors Form A PartnershipДокумент7 страницPROBLEM 2 - Two Sole Proprietors Form A Partnership PROBLEM 2 - Two Sole Proprietors Form A PartnershipRudy LugasОценок пока нет

- Business IA Sample HRДокумент18 страницBusiness IA Sample HRAzhari Ghaffar67% (3)

- AS 9706 Theory FINALДокумент11 страницAS 9706 Theory FINALNew Id0% (1)

- Financial Reporting Financial Statement Analysis and Valuation 8th Edition Wahlen Solutions Manual 1Документ37 страницFinancial Reporting Financial Statement Analysis and Valuation 8th Edition Wahlen Solutions Manual 1shaina100% (46)

- Chapter Contents: Measuring AND Controlling Assets EmployedДокумент10 страницChapter Contents: Measuring AND Controlling Assets EmployedNesru SirajОценок пока нет

- Relation Between Roi and Eva-1Документ11 страницRelation Between Roi and Eva-1Jasleen KaurОценок пока нет

- 07 - Measuring and Controlling Assets EmployedДокумент8 страниц07 - Measuring and Controlling Assets EmployedJason KurniawanОценок пока нет

- CH 7 SPMДокумент22 страницыCH 7 SPMmayliaОценок пока нет

- Investment CentreДокумент27 страницInvestment CentreSiddharth SapkaleОценок пока нет

- Segmented Reporting, Investment Center Evaluation, and Transfer PricingДокумент3 страницыSegmented Reporting, Investment Center Evaluation, and Transfer Pricingeskelapamudah enakОценок пока нет

- Eva Measurement FormulaДокумент14 страницEva Measurement Formulaparamarthasom1974Оценок пока нет

- Dinda Putri Novanti - Summary Measuring and Controlling Asset EmployedДокумент5 страницDinda Putri Novanti - Summary Measuring and Controlling Asset EmployedDinda Putri NovantiОценок пока нет

- Ellah F. Gedalanon BSA-IV: Return On Investment (ROI)Документ2 страницыEllah F. Gedalanon BSA-IV: Return On Investment (ROI)Ellah GedalanonОценок пока нет

- Summary PERFORMANCE MEASUREMENT IN DECENTRALIZED ORGANIZATIONSДокумент9 страницSummary PERFORMANCE MEASUREMENT IN DECENTRALIZED ORGANIZATIONSliaОценок пока нет

- Measure & Control Assets EmployedДокумент17 страницMeasure & Control Assets EmployedAshish Babariya100% (1)

- The EVA Concept of ProfitabilityДокумент9 страницThe EVA Concept of ProfitabilitySriharsha InalaОценок пока нет

- Return On Investment (ROI)Документ2 страницыReturn On Investment (ROI)Ellah GedalanonОценок пока нет

- ACF Long AnswersДокумент14 страницACF Long AnswersTwinkle ChettriОценок пока нет

- Economic Value AddedДокумент9 страницEconomic Value AddedLimisha ViswanathanОценок пока нет

- Measuring and Controlling Assets EmployedДокумент10 страницMeasuring and Controlling Assets EmployedSteffi FeValen's AprildaОценок пока нет

- What Is 'Economic Value Added - EVA'Документ7 страницWhat Is 'Economic Value Added - EVA'atif shaikhОценок пока нет

- Management Control System: Presentation TopicДокумент16 страницManagement Control System: Presentation TopicVj AutiОценок пока нет

- Industrial Products CorporationДокумент4 страницыIndustrial Products CorporationFahmi A. Mubarok100% (1)

- Responsibility AccountingДокумент20 страницResponsibility AccountingaddityarajОценок пока нет

- Chapter III Lecture NoteДокумент22 страницыChapter III Lecture NoteKalkidan NigussieОценок пока нет

- Task 3 - Investment AppraisalДокумент12 страницTask 3 - Investment AppraisalYashmi BhanderiОценок пока нет

- Management Control System: Presentation TopicДокумент14 страницManagement Control System: Presentation TopicRaju YadavОценок пока нет

- Economic Value Added Economic Value Added Is The FinancialДокумент9 страницEconomic Value Added Economic Value Added Is The FinancialKamlesh ChanchlaniОценок пока нет

- Resume Chapter 10Документ7 страницResume Chapter 10Safira KhairaniОценок пока нет

- Free Cash FlowДокумент31 страницаFree Cash FlowKaranvir GuptaОценок пока нет

- 09 Chapter 4Документ47 страниц09 Chapter 4sheetalОценок пока нет

- EVA-Equity Value AddedДокумент33 страницыEVA-Equity Value AddedRanjit SinghОценок пока нет

- Difference Between EVA and ROIДокумент6 страницDifference Between EVA and ROINik PatelОценок пока нет

- Economic Value Added Analysis (EVA)Документ15 страницEconomic Value Added Analysis (EVA)moras99Оценок пока нет

- Sonraj PartДокумент3 страницыSonraj Partmaddy_rocksОценок пока нет

- Business ValuationДокумент8 страницBusiness ValuationKomalОценок пока нет

- MADERAZO, Dheine Louise - Quiz Responsibility - COSTRAMДокумент3 страницыMADERAZO, Dheine Louise - Quiz Responsibility - COSTRAMDheine MaderazoОценок пока нет

- Guese Christian Nicolas A. FM 2-3 Review Question FinalsДокумент6 страницGuese Christian Nicolas A. FM 2-3 Review Question FinalsGuese, Christian Nicolas AОценок пока нет

- Group 6 - Management Control System of Measurement and Control of Managed AssetsДокумент25 страницGroup 6 - Management Control System of Measurement and Control of Managed AssetsHernawatiОценок пока нет

- Economic Value AddedДокумент26 страницEconomic Value Addedshagunpal22Оценок пока нет

- FinalДокумент32 страницыFinalreegup0% (1)

- ROI, EVA and MVA IntroductionДокумент4 страницыROI, EVA and MVA IntroductionkeyurОценок пока нет

- Calculation of EVAДокумент5 страницCalculation of EVAnp_navinpoddarОценок пока нет

- Return On Capital EmployedДокумент6 страницReturn On Capital EmployedFrankie LamОценок пока нет

- Mcs AssignmentДокумент14 страницMcs Assignmentyadavmihir63Оценок пока нет

- Decentralization in Operation and Segment ReportingДокумент5 страницDecentralization in Operation and Segment ReportingMon RamОценок пока нет

- Topic 6 (PMS 1)Документ40 страницTopic 6 (PMS 1)Thiba 2772Оценок пока нет

- Financial Reporting Financial Statement Analysis and Valuation 8th Edition Wahlen Solutions Manual 1Документ36 страницFinancial Reporting Financial Statement Analysis and Valuation 8th Edition Wahlen Solutions Manual 1ericsuttonybmqwiorsa100% (24)

- FM - Eva MvaДокумент14 страницFM - Eva MvaKowsik RajendranОценок пока нет

- ROIC Greenblatt and Fool ArticlesДокумент11 страницROIC Greenblatt and Fool Articlesjcv2010100% (1)

- Financial Goal Setting-12012013 - FinalДокумент51 страницаFinancial Goal Setting-12012013 - FinalJaie SurveОценок пока нет

- Return On Investment (ROI) Method For Measuring Managerial PerformanceДокумент1 страницаReturn On Investment (ROI) Method For Measuring Managerial PerformanceAtik AlawiahОценок пока нет

- Measuring and Controlling Assets Employed + DELL Case StudyДокумент34 страницыMeasuring and Controlling Assets Employed + DELL Case Studykid.hahn100% (1)

- ABC&EVAДокумент20 страницABC&EVAArjun SubhashОценок пока нет

- Return On Investment: Assignment-2Документ7 страницReturn On Investment: Assignment-2Vineet AgrawalОценок пока нет

- Pros and Cons of EVA 013-08Документ6 страницPros and Cons of EVA 013-08apluОценок пока нет

- Responsibility CentreДокумент5 страницResponsibility CentreataulbariОценок пока нет

- Eva & MvaДокумент5 страницEva & MvaVineet ChouhanОценок пока нет

- Divisional MeasurementДокумент29 страницDivisional MeasurementNagaraj UpparОценок пока нет

- Chapter 1 Answers To Discussion QuestionsДокумент9 страницChapter 1 Answers To Discussion QuestionsTiaradipa Amanda100% (1)

- Chapter 19 Audit of Acquisition and Payment CycleДокумент21 страницаChapter 19 Audit of Acquisition and Payment Cycle0601084730% (1)

- International Economic Linkages and Balance of PaymentsДокумент4 страницыInternational Economic Linkages and Balance of PaymentsTiaradipa AmandaОценок пока нет

- Installment Acquisitions of SubsidiaryДокумент4 страницыInstallment Acquisitions of SubsidiaryTiaradipa AmandaОценок пока нет

- SAP Analisys Financial ReportДокумент4 страницыSAP Analisys Financial ReportTiaradipa AmandaОценок пока нет

- Installment Acquisitions of SubsidiaryДокумент4 страницыInstallment Acquisitions of SubsidiaryTiaradipa AmandaОценок пока нет

- Pricing Corporate ServiceДокумент8 страницPricing Corporate ServiceTiaradipa AmandaОценок пока нет

- Analyzing Financial Performance ReportДокумент3 страницыAnalyzing Financial Performance ReportTiaradipa Amanda100% (1)

- Hire Purchase Law RevisedДокумент46 страницHire Purchase Law RevisedBilliee ButccherОценок пока нет

- Valiant Organics ET (Q4-FY 22)Документ20 страницValiant Organics ET (Q4-FY 22)beza manojОценок пока нет

- Case 2 Group 2 BUS 520 MDS Section1Документ6 страницCase 2 Group 2 BUS 520 MDS Section1Saief AhmadОценок пока нет

- Larry Williams Accumulation DistributionДокумент22 страницыLarry Williams Accumulation DistributionLupistrikis hernandezОценок пока нет

- How To Test Banking Domain Applications: A Complete BFSI Testing GuideДокумент52 страницыHow To Test Banking Domain Applications: A Complete BFSI Testing GuideMamatha K NОценок пока нет

- Presentation Slides November 2022 - AIQSДокумент27 страницPresentation Slides November 2022 - AIQSSham GeorgeОценок пока нет

- eBayReturnLabel 5135454522 PDFДокумент2 страницыeBayReturnLabel 5135454522 PDFsherry webberОценок пока нет

- Properties of Stock OptionsДокумент20 страницProperties of Stock OptionsShashank TyagiОценок пока нет

- MIS Practical FileДокумент27 страницMIS Practical FileSukhdeep SinghОценок пока нет

- Internal Factor Evaluation: Strengths Weight Rating (3-4) Weighte D AverageДокумент3 страницыInternal Factor Evaluation: Strengths Weight Rating (3-4) Weighte D AverageHira NazОценок пока нет

- Ms Thesis Last Final FinalДокумент54 страницыMs Thesis Last Final FinalgizaskenОценок пока нет

- Automobile Corporation of Goa LTD: Federal-Mogul Goetze (India) LTDДокумент4 страницыAutomobile Corporation of Goa LTD: Federal-Mogul Goetze (India) LTDShashikant VaidyanathanОценок пока нет

- Mineral Resources PDFДокумент15 страницMineral Resources PDFrohin haroonОценок пока нет

- Antoine Touzé: Profile SummaryДокумент1 страницаAntoine Touzé: Profile SummaryAnonymous g9jqvalhGОценок пока нет

- COBIT 2019 Foundation ExamДокумент28 страницCOBIT 2019 Foundation ExamVitor Suzarte100% (1)

- 08 - Barretto Vs Santa MarinaДокумент1 страница08 - Barretto Vs Santa MarinaRia GabsОценок пока нет

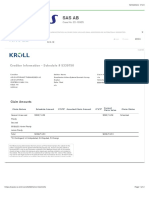

- Kroll Restructuring AdministrationДокумент2 страницыKroll Restructuring AdministrationMarОценок пока нет

- Rivera Vs EspirituДокумент4 страницыRivera Vs EspirituChingОценок пока нет

- MGT602 Final Subjective by USMAN ATTARIДокумент12 страницMGT602 Final Subjective by USMAN ATTARImaryamОценок пока нет

- Muhammad Shahid Bhatti S/O Abdul Ghafoor H No 8 ST No 50 Nadeem Shaheed RDДокумент1 страницаMuhammad Shahid Bhatti S/O Abdul Ghafoor H No 8 ST No 50 Nadeem Shaheed RDkhawar mukhtarОценок пока нет

- POs Pre Joining Study Material PDFДокумент152 страницыPOs Pre Joining Study Material PDFKushagra Pratap SinghОценок пока нет

- Data Tables Foxia - Responsive Bootstrap 5 Admin DashboardДокумент2 страницыData Tables Foxia - Responsive Bootstrap 5 Admin DashboardnaimahadouОценок пока нет

- Job Description - Ops StratДокумент3 страницыJob Description - Ops StratchengadОценок пока нет

- Variador de Frecuencia RA - STR - MHCДокумент60 страницVariador de Frecuencia RA - STR - MHCPatricia PainemánОценок пока нет

- 202221040Документ5 страниц202221040R A.Оценок пока нет

- Foreign Literature Customer Satisfaction Through Online PaymentsДокумент9 страницForeign Literature Customer Satisfaction Through Online PaymentsJonathanОценок пока нет

- mgt613 Mega Files of McqsssДокумент203 страницыmgt613 Mega Files of McqsssSalman SikandarОценок пока нет

- Strategy - Chapter 5: Basing Strategy On Resources and CapabilitiesДокумент8 страницStrategy - Chapter 5: Basing Strategy On Resources and CapabilitiesTang WillyОценок пока нет