Вам также может понравиться

- Identification of Equipment For MaintenanceДокумент14 страницIdentification of Equipment For MaintenanceAZDOLMANОценок пока нет

- IP 570-2009 RR Research ReportДокумент30 страницIP 570-2009 RR Research Reportkrunalb@inОценок пока нет

- Chevron RichmondДокумент55 страницChevron RichmondAZDOLMANОценок пока нет

- Chevron RichmondДокумент4 страницыChevron RichmondAZDOLMANОценок пока нет

- Building World Class LNG Operations: Chevron AustraliaДокумент8 страницBuilding World Class LNG Operations: Chevron AustraliaAZDOLMANОценок пока нет

- 06 Hydraulic PumpingДокумент71 страница06 Hydraulic PumpingAZDOLMANОценок пока нет

- 20 Gas Properties and CorrelationsДокумент18 страниц20 Gas Properties and CorrelationsAZDOLMANОценок пока нет

- 11 Oil StorageДокумент14 страниц11 Oil StorageAZDOLMANОценок пока нет

- Reliability Availability and Maintainability RAMДокумент20 страницReliability Availability and Maintainability RAMShawqi MohammedОценок пока нет

- Top 10 CareerДокумент3 страницыTop 10 CareerAZDOLMANОценок пока нет

- Refining Human FactorsДокумент6 страницRefining Human FactorsAZDOLMANОценок пока нет

- Est TK EmissДокумент2 страницыEst TK EmissAZDOLMANОценок пока нет

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5795)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (345)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1091)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- Pipeline Engineering (Module 1)Документ39 страницPipeline Engineering (Module 1)Het Patel100% (2)

- PlasticsEurope Eco-Profile BTX 2013-02Документ46 страницPlasticsEurope Eco-Profile BTX 2013-02judithОценок пока нет

- Unit Conversion Factors - RakeshRRДокумент4 страницыUnit Conversion Factors - RakeshRRRakesh Roshan RanaОценок пока нет

- Term Paper - Modular Refining in Nigeria.Документ2 страницыTerm Paper - Modular Refining in Nigeria.Isesele victorОценок пока нет

- 02a. Level of Petroleum InvestigationДокумент28 страниц02a. Level of Petroleum Investigationdina mutia sariОценок пока нет

- UOP Solutions To Process MazutДокумент12 страницUOP Solutions To Process MazutTomasz OleckiОценок пока нет

- 01 Rig List January 2016Документ17 страниц01 Rig List January 2016ifebrianОценок пока нет

- IoclДокумент25 страницIoclShubham JainОценок пока нет

- Ecuación de AntoineДокумент35 страницEcuación de AntoineRuben PachecoОценок пока нет

- Oil & Gas Resources of Aus 2003Документ260 страницOil & Gas Resources of Aus 2003smashfacemcgeeОценок пока нет

- Uganda Oil Wells Factsheet May 2012Документ4 страницыUganda Oil Wells Factsheet May 2012African Centre for Media ExcellenceОценок пока нет

- Budget Preparation For Fuel SubsidyДокумент25 страницBudget Preparation For Fuel SubsidyOswar MungkasaОценок пока нет

- On CGD PDFДокумент13 страницOn CGD PDFVaishnavi SinghОценок пока нет

- Heavy Niques: Oil Recovery TechДокумент31 страницаHeavy Niques: Oil Recovery TechNagalakshmi ThirunavukkarasuОценок пока нет

- 19 AlvheimДокумент3 страницы19 AlvheimLem Fei-BronjulОценок пока нет

- Database Documentation: Natural Gas Information 2021 EDITIONДокумент54 страницыDatabase Documentation: Natural Gas Information 2021 EDITIONphaniraj_cОценок пока нет

- Contactos Arg-ColombiaДокумент40 страницContactos Arg-ColombiaJuan Angel Gonzalez CamposОценок пока нет

- ASTM D7504: Impurities in Monocyclic Aromatic Hydrocarbons On StabilwaxДокумент1 страницаASTM D7504: Impurities in Monocyclic Aromatic Hydrocarbons On StabilwaxformoviejuneОценок пока нет

- Lecture 0 Rule and SylabusДокумент13 страницLecture 0 Rule and SylabusStyОценок пока нет

- Restrictions:: Cas N°: Empirical FormulaДокумент2 страницыRestrictions:: Cas N°: Empirical FormulaPaul KilerОценок пока нет

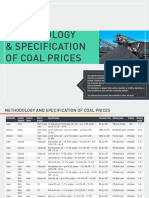

- Metal Expert: Methodology & Specification of Coal PricesДокумент8 страницMetal Expert: Methodology & Specification of Coal PricesOperation TewehОценок пока нет

- Ecopetrol Vasconia Blend VSM-01Документ4 страницыEcopetrol Vasconia Blend VSM-01SalazarJohnFОценок пока нет

- PT Berlian Laju Tanker TBK: Tank Cleaning GuideДокумент66 страницPT Berlian Laju Tanker TBK: Tank Cleaning Guideandri wirawan100% (1)

- 1-Petroleum Geology CourseДокумент36 страниц1-Petroleum Geology CourseAlameen GandelaОценок пока нет

- 50 Oraciones de Ingles 1!Документ3 страницы50 Oraciones de Ingles 1!WJ-nimodo QuispeОценок пока нет

- Petro Bowl Example QuestionsДокумент6 страницPetro Bowl Example QuestionsAndre Atanova100% (4)

- Brian Roberts +33 1 47 78 25 37 +44 7710 54 92 39 Jim O'Sullivan +1 281 249 7511Документ16 страницBrian Roberts +33 1 47 78 25 37 +44 7710 54 92 39 Jim O'Sullivan +1 281 249 7511Phillip FriedmanОценок пока нет

- LNG BasicsДокумент14 страницLNG BasicsAnil Kumar MohapatraОценок пока нет

- Fork Oils - Comparitive WeightsДокумент2 страницыFork Oils - Comparitive WeightsGustavo MazzottaОценок пока нет

- 0 0 24 Dec 2014 1536306771Annexure-Pre-feasibilityReportДокумент342 страницы0 0 24 Dec 2014 1536306771Annexure-Pre-feasibilityReportSiddharth JainОценок пока нет