Вам также может понравиться

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- Testing Your Trading PlanДокумент10 страницTesting Your Trading PlanTyler K. Moore100% (3)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- Small Business Bibliography PDFДокумент56 страницSmall Business Bibliography PDFOlaru LorenaОценок пока нет

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

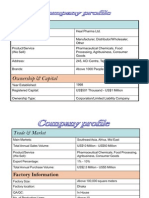

- Company ProfileДокумент29 страницCompany ProfileMohammad Farhan ImtiazОценок пока нет

- Bar Questions - Obligations and ContractsДокумент6 страницBar Questions - Obligations and ContractsPriscilla Dawn100% (9)

- Chapter 8Документ8 страницChapter 8Kurt dela Torre100% (1)

- RBS ReportДокумент27 страницRBS ReportElmira GamaОценок пока нет

- LAW 20013 Law On Obligations and Contracts Midterm ReviewДокумент14 страницLAW 20013 Law On Obligations and Contracts Midterm ReviewNila Francia100% (1)

- 5 - Allied Thread v. City of Manila G.R. No. L-40296 November 21, 1984Документ1 страница5 - Allied Thread v. City of Manila G.R. No. L-40296 November 21, 1984Pam Otic-ReyesОценок пока нет

- BrokersДокумент47 страницBrokersManjunath ShettigarОценок пока нет

- Hoisington Q3Документ6 страницHoisington Q3ZerohedgeОценок пока нет

- BMWДокумент9 страницBMWgulzaaressopОценок пока нет

- International Finance ReportДокумент13 страницInternational Finance ReportMohammad Farhan ImtiazОценок пока нет

- FalklandsДокумент1 страницаFalklandsMohammad Farhan ImtiazОценок пока нет

- GVC Part 2Документ1 страницаGVC Part 2Mohammad Farhan ImtiazОценок пока нет

- Neha Maheshwari AU Bank Sip ReportДокумент49 страницNeha Maheshwari AU Bank Sip ReportAbhishek ShrivastavaОценок пока нет

- FINE 6200 F, Winter 2016, TuesdayДокумент9 страницFINE 6200 F, Winter 2016, TuesdayAlex PoonОценок пока нет

- Bill Ackman's Letter On General GrowthДокумент8 страницBill Ackman's Letter On General GrowthZoe GallandОценок пока нет

- KSPI FY24 Guidance For 2024Q2Документ8 страницKSPI FY24 Guidance For 2024Q2brianlam205Оценок пока нет

- New Account Data SheetДокумент1 страницаNew Account Data SheetpicfixerОценок пока нет

- The Merchant of Venice - Themes and Symbols FILAДокумент3 страницыThe Merchant of Venice - Themes and Symbols FILAboudjellalkhawla70Оценок пока нет

- Assignment On Financial StatementДокумент11 страницAssignment On Financial StatementHamza IqbalОценок пока нет

- FINANCIAL MANAGEMENT (MBA234) - 1568644543445.htmlДокумент2 страницыFINANCIAL MANAGEMENT (MBA234) - 1568644543445.htmlJeswin BennyОценок пока нет

- A CASE STUDY OF EVEREST BANK LIMITED Mbs ThesisДокумент74 страницыA CASE STUDY OF EVEREST BANK LIMITED Mbs Thesisशिवम कर्ण100% (1)

- Community and Management Skills TrainingДокумент42 страницыCommunity and Management Skills TrainingAdnan AkramОценок пока нет

- ICBC Presentation 09Документ24 страницыICBC Presentation 09AhmadОценок пока нет

- International Financial Management: Jeff Madura 7 EditionДокумент38 страницInternational Financial Management: Jeff Madura 7 EditionBilal sattiОценок пока нет

- Reading 32 Introduction To Commodities and Commodity DerivativesДокумент5 страницReading 32 Introduction To Commodities and Commodity Derivativestristan.riolsОценок пока нет

- United States v. Smith, 1st Cir. (1995)Документ67 страницUnited States v. Smith, 1st Cir. (1995)Scribd Government DocsОценок пока нет

- Mine Evaluation and Investment Analysis and Mine Development and Exploitation-1Документ5 страницMine Evaluation and Investment Analysis and Mine Development and Exploitation-1nadieОценок пока нет

- The Yukii Community Token (YCT)Документ15 страницThe Yukii Community Token (YCT)Sopso TkoОценок пока нет

- LTD Offer 2019 EurДокумент2 страницыLTD Offer 2019 EurkatariamanojОценок пока нет

- CFAДокумент79 страницCFATuan TrinhОценок пока нет

- Brief Curriculum Vitae: Specialisation: (P Ea 1. 2. 3. Statistical AnalysisДокумент67 страницBrief Curriculum Vitae: Specialisation: (P Ea 1. 2. 3. Statistical Analysisanon_136103548Оценок пока нет

- CH01Документ41 страницаCH01ahmad_habibi_70% (1)

- Elizabeth Del Carmen Vs Spouses Restituto Sabordo and Mima Mahilim-SabordoДокумент6 страницElizabeth Del Carmen Vs Spouses Restituto Sabordo and Mima Mahilim-SabordoChoi ChoiОценок пока нет