Вам также может понравиться

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (119)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2219)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- Blades in The Dark - Doskvol Maps PDFДокумент3 страницыBlades in The Dark - Doskvol Maps PDFRobert Rome20% (5)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (890)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Briefcase On Company Law Briefcase SeriesДокумент180 страницBriefcase On Company Law Briefcase SeriesAminath ShahulaОценок пока нет

- TCC Midc Company ListДокумент4 страницыTCC Midc Company ListAbhishek SinghОценок пока нет

- Cost Accounting Course GuideДокумент10 страницCost Accounting Course GuidePatrick VoiceОценок пока нет

- MineДокумент6 страницMinePatrick VoiceОценок пока нет

- Paper 2Документ1 страницаPaper 2Patrick VoiceОценок пока нет

- Job Order Vs Process Costing: Transparency Master 2-1Документ14 страницJob Order Vs Process Costing: Transparency Master 2-1Patrick VoiceОценок пока нет

- 12 4Документ2 страницы12 4Patrick VoiceОценок пока нет

- Mcom Cbcs LatestДокумент45 страницMcom Cbcs Latestanoopsingh19992010Оценок пока нет

- Ride Details Bill Details: Thanks For Travelling With Us, KarthickДокумент3 страницыRide Details Bill Details: Thanks For Travelling With Us, KarthickKarthick P100% (1)

- Perfect Substitutes and Perfect ComplementsДокумент2 страницыPerfect Substitutes and Perfect ComplementsVijayalaxmi DhakaОценок пока нет

- PUGEL 'Scale Economies Imperfect Competition and Trade' INTERNATIONAL ECONOMICS 6ED - Thomas Pugel - 001 PDFДокумент29 страницPUGEL 'Scale Economies Imperfect Competition and Trade' INTERNATIONAL ECONOMICS 6ED - Thomas Pugel - 001 PDFPraba Vettrivelu100% (1)

- Five Forces Analysis TemplateДокумент2 страницыFive Forces Analysis TemplateKedar JoshiОценок пока нет

- Five Key Sources of Critical Success FactorsДокумент2 страницыFive Key Sources of Critical Success FactorsHanako ChinatsuОценок пока нет

- Prime HR & Security Solutions PVT LTD: SUB: Appointment As HR ExecutiveДокумент3 страницыPrime HR & Security Solutions PVT LTD: SUB: Appointment As HR ExecutivesayalikОценок пока нет

- Book Building Process and Types ExplainedДокумент15 страницBook Building Process and Types ExplainedPoojaDesaiОценок пока нет

- Second Reading of Ordinance State Housing Law 01-05-16Документ16 страницSecond Reading of Ordinance State Housing Law 01-05-16L. A. PatersonОценок пока нет

- Mineral and Energy ResourcesДокумент4 страницыMineral and Energy ResourcesJoseph ZotooОценок пока нет

- Economics TopicsДокумент2 страницыEconomics Topicsatif_ausaf100% (1)

- FAR1 ASN01 Balance Sheet and Income Statement PDFДокумент1 страницаFAR1 ASN01 Balance Sheet and Income Statement PDFira concepcionОценок пока нет

- Reflections Fall 2010Документ84 страницыReflections Fall 2010campbell_harmon6178Оценок пока нет

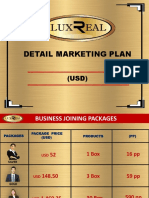

- Luxreal Detail Marketing Plan (2019) UsdДокумент32 страницыLuxreal Detail Marketing Plan (2019) UsdTawanda Tirivangani100% (2)

- 12 Jun 2019 PDFДокумент12 страниц12 Jun 2019 PDFAnonymous dy7g4jzo7Оценок пока нет

- IBM - Multiple Choice Questions PDFДокумент15 страницIBM - Multiple Choice Questions PDFsachsanjuОценок пока нет

- Stericycle Hazardous Waste LocationsДокумент2 страницыStericycle Hazardous Waste LocationsStericycleОценок пока нет

- Bank of IndiaДокумент3 страницыBank of IndiaRajesh Kumar SamalОценок пока нет

- Chapter Six: Designing Organizations For The International EnvironmentДокумент17 страницChapter Six: Designing Organizations For The International EnvironmentMohammed AlhashdiОценок пока нет

- 10.18.2017 LiabiltiesДокумент4 страницы10.18.2017 LiabiltiesPatOcampoОценок пока нет

- Blue Chip Stocks List: 3%+ Yields & 100+ Year HistoriesДокумент55 страницBlue Chip Stocks List: 3%+ Yields & 100+ Year HistoriesSonny JimОценок пока нет

- 10 Activity 1 MRLFJRDДокумент1 страница10 Activity 1 MRLFJRDMurielle FajardoОценок пока нет

- Survey highlights deficits facing India's minority districtsДокумент75 страницSurvey highlights deficits facing India's minority districtsAnonymous yCpjZF1rFОценок пока нет

- IRCTCs e-Ticketing Service DetailsДокумент2 страницыIRCTCs e-Ticketing Service DetailsOPrakash RОценок пока нет

- PRC Ready ReckonerДокумент2 страницыPRC Ready Reckonersparthan300Оценок пока нет

- 10th March: by Dr. Gaurav GargДокумент2 страницы10th March: by Dr. Gaurav GarganupamОценок пока нет

- Use The Following Information in Answering Questions 130 and 131Документ1 страницаUse The Following Information in Answering Questions 130 and 131Joanne FernandezОценок пока нет