Вам также может понравиться

- Exam 3 Review Sheet Summer 09Документ14 страницExam 3 Review Sheet Summer 09kpatel4uОценок пока нет

- CFE Certified Fraud Examiners Exam Practice Questions and DumpsДокумент12 страницCFE Certified Fraud Examiners Exam Practice Questions and Dumps20212111047 TEUKU MAULANA ARDIANSYAH100% (1)

- Audit evidence limitations for ZZZZ Best insurance contractsДокумент4 страницыAudit evidence limitations for ZZZZ Best insurance contractsNovah Mae Begaso SamarОценок пока нет

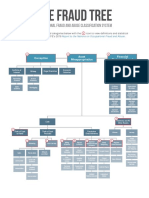

- The Fraud Tree: Occupational Fraud and Abuse Classification SystemДокумент1 страницаThe Fraud Tree: Occupational Fraud and Abuse Classification SystemZiyishi WangОценок пока нет

- Manual Journal Entry Testing: Data Analytics and The Risk of FraudДокумент14 страницManual Journal Entry Testing: Data Analytics and The Risk of FraudArtho KasihОценок пока нет

- Sarbanes Oxley Internal Controls A Complete Guide - 2021 EditionОт EverandSarbanes Oxley Internal Controls A Complete Guide - 2021 EditionОценок пока нет

- Out - 28 IT FraudДокумент41 страницаOut - 28 IT FraudNur P UtamiОценок пока нет

- Introduction, Conceptual Framework of The Study & Research DesignДокумент16 страницIntroduction, Conceptual Framework of The Study & Research DesignSтυριd・ 3尺ㄖ尺Оценок пока нет

- Case Study Opportunity FA PDFДокумент39 страницCase Study Opportunity FA PDFDiarany SucahyatiОценок пока нет

- Fraud Pentagon Theory Influences Detection of Financial Statement FraudДокумент14 страницFraud Pentagon Theory Influences Detection of Financial Statement FraudChill GouvtfrondОценок пока нет

- Internet Fraud 6monthreport 2000 AДокумент14 страницInternet Fraud 6monthreport 2000 AFlaviub23Оценок пока нет

- Motivation For FraudДокумент7 страницMotivation For FraudKatrina EustaceОценок пока нет

- Fraud Risk AssessmentДокумент32 страницыFraud Risk AssessmentArturoОценок пока нет

- Recognizing The Symptoms of FraudДокумент12 страницRecognizing The Symptoms of FraudlieselenaОценок пока нет

- Forensic Accounting NotesДокумент14 страницForensic Accounting NotesCaCs Piyush SarupriaОценок пока нет

- Managing Fraud Risks with the Fraud DiamondДокумент5 страницManaging Fraud Risks with the Fraud DiamondveranitaОценок пока нет

- Case 5.3Документ6 страницCase 5.3Annisa Kurnia0% (1)

- 04 - Fraud Risk Management A Guide To GOOD PRACTICEДокумент48 страниц04 - Fraud Risk Management A Guide To GOOD PRACTICEEd Gonzales GonzalesОценок пока нет

- Fraud Risk Management GuideДокумент2 страницыFraud Risk Management GuideClaudia LauraОценок пока нет

- Research PaperДокумент14 страницResearch PaperSoumya SaranjiОценок пока нет

- Fraud in AccountingДокумент10 страницFraud in AccountingDwi Putra Rachmad AbdillahОценок пока нет

- Continuous Fraud DetectionДокумент23 страницыContinuous Fraud Detectionbudi.hw748Оценок пока нет

- Fraud Definition Causes Impact IndicatorsДокумент35 страницFraud Definition Causes Impact IndicatorsMutabarKhanОценок пока нет

- Rais12 SM CH05Документ35 страницRais12 SM CH05Anton VitaliОценок пока нет

- Internal ControlsДокумент17 страницInternal ControlsSitti Najwa100% (1)

- ScandalДокумент83 страницыScandalForeclosure FraudОценок пока нет

- Fraud Risk MДокумент11 страницFraud Risk MEka Septariana PuspaОценок пока нет

- The Foreign Corrupt Practices Act BY Ca Vijay Kumar GargДокумент14 страницThe Foreign Corrupt Practices Act BY Ca Vijay Kumar GargVijay Garg100% (1)

- Fraud Audit - Kelompok 10 - Consumen Fraud - FinalДокумент56 страницFraud Audit - Kelompok 10 - Consumen Fraud - Finalmeilisa nugrahaОценок пока нет

- Fraud-Tree SchemesДокумент13 страницFraud-Tree SchemessulthanhakimОценок пока нет

- US Internal Revenue Service: p4579Документ208 страницUS Internal Revenue Service: p4579IRSОценок пока нет

- AUD Demo CompanionДокумент35 страницAUD Demo Companionalik711698Оценок пока нет

- P - Fraud Risk InquiriesДокумент4 страницыP - Fraud Risk InquiriesHis HerОценок пока нет

- Ibm ReportДокумент7 страницIbm ReportleejolieОценок пока нет

- Generic Definition: ": Manufacturing Inventory: Besides Finished Goods, Also Includes Raw Materials Used inДокумент12 страницGeneric Definition: ": Manufacturing Inventory: Besides Finished Goods, Also Includes Raw Materials Used inRosita BarcaloungerОценок пока нет

- Ethics, Fraud Schemes, and Fraud DetectionДокумент41 страницаEthics, Fraud Schemes, and Fraud DetectionIzza Mae Rivera KarimОценок пока нет

- Fraud Examination Chapter 1: The Nature of FraudДокумент11 страницFraud Examination Chapter 1: The Nature of FraudAyi AbdurachimОценок пока нет

- Fraud Prevention and DetectionДокумент3 страницыFraud Prevention and DetectionTahir AbbasОценок пока нет

- Chapter 12Документ9 страницChapter 12EdrickLouise DimayugaОценок пока нет

- Research Paper (Comparative Analysis of Global Financial Laws)Документ17 страницResearch Paper (Comparative Analysis of Global Financial Laws)Soumya SaranjiОценок пока нет

- Forensic Accounting FinДокумент33 страницыForensic Accounting FinakanshagОценок пока нет

- Fraud Prevention & DetectionДокумент15 страницFraud Prevention & DetectionswathivishnuОценок пока нет

- Fraud Prevention PolicyДокумент2 страницыFraud Prevention PolicyAbhishek KumarОценок пока нет

- CFDG Fraud Policy PDFДокумент6 страницCFDG Fraud Policy PDFSanath FernandoОценок пока нет

- An Analysis of Fraud Triangle and Responsibilities of AuditorsДокумент8 страницAn Analysis of Fraud Triangle and Responsibilities of AuditorsPrihandani AntonОценок пока нет

- Fraud Triangle ExplainedДокумент3 страницыFraud Triangle Explainedcoleen paraynoОценок пока нет

- Internal Audit HospitalДокумент30 страницInternal Audit HospitalReddy Shekar PОценок пока нет

- Financial Statement Fraud DetectionДокумент5 страницFinancial Statement Fraud DetectionreyhnkОценок пока нет

- Fraud Examiners Manual (International Edition)Документ14 страницFraud Examiners Manual (International Edition)Alper Hücümenoğlu0% (3)

- Fraud IndicatorsДокумент26 страницFraud IndicatorsIena SharinaОценок пока нет

- Albrecht 4e Ch02 SolutionsДокумент17 страницAlbrecht 4e Ch02 SolutionsNana NurhayatiОценок пока нет

- Fi 10032020Документ46 страницFi 10032020CA. (Dr.) Rajkumar Satyanarayan AdukiaОценок пока нет

- Managing fraud risk at Summit ConsultingДокумент48 страницManaging fraud risk at Summit ConsultingMustapha MugisaОценок пока нет

- Chapter 17 - Occupational Fraud and Abuse - The Big Picture - Principles of Fraud Examination, 4th EditionДокумент11 страницChapter 17 - Occupational Fraud and Abuse - The Big Picture - Principles of Fraud Examination, 4th Editionscribd20014Оценок пока нет

- ACH Guides Managing Fraud RiskДокумент24 страницыACH Guides Managing Fraud RiskRafik BelkahlaОценок пока нет

- Corporate Accounting Fraud: A Case Study of Satyam Computers LimitedДокумент27 страницCorporate Accounting Fraud: A Case Study of Satyam Computers LimitedVenus AreolaОценок пока нет

- Fraud Schemes in The Banking Institutions: Prevention Measures To Avoid Severe Financial LossДокумент7 страницFraud Schemes in The Banking Institutions: Prevention Measures To Avoid Severe Financial LossBelaОценок пока нет

- Precis & Drafting Without BooksДокумент12 страницPrecis & Drafting Without BooksEr. VinodОценок пока нет

- Bringing Certainty to UncertaintyДокумент304 страницыBringing Certainty to UncertaintySezan Louis DofoОценок пока нет

- 59760ICAI Official Directory-2020-21bДокумент220 страниц59760ICAI Official Directory-2020-21bViratVermaОценок пока нет

- Final Order in Dalmia Industrial Development Limited MatterДокумент51 страницаFinal Order in Dalmia Industrial Development Limited MatterPratim MajumderОценок пока нет

- SP Pts CourseДокумент8 страницSP Pts Coursencguy001100% (1)

- Chapter-1 Introduction To Accounting and BusinessДокумент17 страницChapter-1 Introduction To Accounting and BusinessTsegaye Belay100% (1)

- Internal ControlДокумент13 страницInternal ControlOlabanjo Shefiu OlamijiОценок пока нет

- Auditing Expenditure Cycle Chapter 10Документ12 страницAuditing Expenditure Cycle Chapter 10Wendelyn TutorОценок пока нет

- Sanction For PGP BooksДокумент1 страницаSanction For PGP BooksJaya Simha ReddyОценок пока нет

- Chapter 17 Alternate Problems Problem 17.1A: Alternate Problems For Use With Financial and Managerial Accounting, 12eДокумент8 страницChapter 17 Alternate Problems Problem 17.1A: Alternate Problems For Use With Financial and Managerial Accounting, 12eSharadPanchalОценок пока нет

- PSA 100 Phil Framework For Assurance EngagementsДокумент4 страницыPSA 100 Phil Framework For Assurance EngagementsSkye LeeОценок пока нет

- Antifraud PlaybookДокумент60 страницAntifraud PlaybookDani UsmarОценок пока нет

- Forensic Accounting: in The Context of Banking Operations: October 2018Документ18 страницForensic Accounting: in The Context of Banking Operations: October 2018Shaina NavaОценок пока нет

- (Vacant) : Board of Directors Gujranwala Waste Management CompanyДокумент1 страница(Vacant) : Board of Directors Gujranwala Waste Management Companywaseemaslam_educationОценок пока нет

- SMChap008 PDFДокумент14 страницSMChap008 PDFShannon ElizaldeОценок пока нет

- Module 3 - Overview of NPOДокумент19 страницModule 3 - Overview of NPOJebong CaguitlaОценок пока нет

- 06 - (San Juan) Philippines - Fiscal InstitutionsДокумент20 страниц06 - (San Juan) Philippines - Fiscal InstitutionsSharmaine LopezОценок пока нет

- Internal Audit Planning and Scheduling Sample FormatДокумент3 страницыInternal Audit Planning and Scheduling Sample FormatAkasha KhanОценок пока нет

- Department of Education: Learner Activity Sheet/Worksheets in Fundamentals of Accountacy, Business and Management 1Документ6 страницDepartment of Education: Learner Activity Sheet/Worksheets in Fundamentals of Accountacy, Business and Management 1onelbabalconОценок пока нет

- Audit Checklist TemplateДокумент18 страницAudit Checklist TemplateDesi AgustiniОценок пока нет

- Accounting EstimatesДокумент6 страницAccounting EstimatesChinОценок пока нет

- The Institute of Internal Auditors - An International AssociationДокумент3 страницыThe Institute of Internal Auditors - An International AssociationOAIA Internal AuditorОценок пока нет

- The Role of An Auditor in The Achievement of Organisational ObjectivesДокумент68 страницThe Role of An Auditor in The Achievement of Organisational ObjectivesShuaib OLAJIREОценок пока нет

- Annexure V FDSSДокумент5 страницAnnexure V FDSSpmОценок пока нет

- Matriculation NoДокумент13 страницMatriculation NoKetz NKОценок пока нет

- Sept 19, CI Program Coaching - Batch 2Документ6 страницSept 19, CI Program Coaching - Batch 2Jesson AlbaranОценок пока нет

- SEBI Grade A Model Test Paper 2Документ32 страницыSEBI Grade A Model Test Paper 2Snehashree SahooОценок пока нет

- PG Auditing Liquidity Risk An OverviewДокумент28 страницPG Auditing Liquidity Risk An OverviewErikОценок пока нет

- Financial Due Diligence - ICAI - Oct 09 - PresentationДокумент32 страницыFinancial Due Diligence - ICAI - Oct 09 - PresentationSumitWatkar100% (2)

- Principles of Financial AccountingДокумент7 страницPrinciples of Financial Accountinghnoor94Оценок пока нет