Вам также может понравиться

- Pricing of CommoditiesДокумент3 страницыPricing of CommoditiesMostafizul HaqueОценок пока нет

- F&B Cost Controller NotesДокумент4 страницыF&B Cost Controller NotesAtif SheikhОценок пока нет

- How Much Is That Hoagie in The Window?Документ41 страницаHow Much Is That Hoagie in The Window?PraveenОценок пока нет

- Food and Beverage Chapter 4Документ8 страницFood and Beverage Chapter 4GraceCayabyabNiduazaОценок пока нет

- Chapter 9 Monitoring Foodservice Operations II Daily Food CostДокумент14 страницChapter 9 Monitoring Foodservice Operations II Daily Food CostArifin FuОценок пока нет

- Food Costing NotesДокумент8 страницFood Costing NotesSunil SharmaОценок пока нет

- Food Control CycleДокумент13 страницFood Control CycleNikki Mae PalanasОценок пока нет

- F&B Management ComoletДокумент31 страницаF&B Management ComoletMudassir Ahsan AnsariОценок пока нет

- Food Cost ControlДокумент7 страницFood Cost ControlAtul Mishra100% (1)

- Chapter 1-Cost and Sales ConceptДокумент10 страницChapter 1-Cost and Sales ConceptFshahirah JelaniОценок пока нет

- Food Cost ControlДокумент5 страницFood Cost ControlPraveenОценок пока нет

- Storing DHMControlДокумент11 страницStoring DHMControlOm SinghОценок пока нет

- Managing Cost ControlДокумент44 страницыManaging Cost Controlنايف العتيبي100% (1)

- Stragetic Cost ReductionДокумент4 страницыStragetic Cost ReductionmariyaОценок пока нет

- The Control ProcessДокумент45 страницThe Control Processmareng susanОценок пока нет

- F&B MGTДокумент54 страницыF&B MGTdenilgeorgeОценок пока нет

- Abstract:: How To Control Food Costing and Management Costing in Hospitality Industry 1. AuthorДокумент8 страницAbstract:: How To Control Food Costing and Management Costing in Hospitality Industry 1. AuthorDenray RespondeОценок пока нет

- Presentation On:-: Kitchen Cost ControlДокумент56 страницPresentation On:-: Kitchen Cost ControlSa SugarОценок пока нет

- Cost ControlДокумент11 страницCost ControlOm Singh100% (11)

- F&B Management Notes at 3rd SemДокумент236 страницF&B Management Notes at 3rd SemJoseph Kiran ReddyОценок пока нет

- Chapter-1 Food Cost ControlДокумент9 страницChapter-1 Food Cost ControlJaved Mokashi100% (1)

- Food & Beverage Cost Control FunctionsДокумент8 страницFood & Beverage Cost Control Functionslananh12345100% (5)

- Introduction To Food Cost ControlДокумент6 страницIntroduction To Food Cost ControldarshОценок пока нет

- CACS Restaurant Operation: Cost Control, Inventory Management and FraudДокумент20 страницCACS Restaurant Operation: Cost Control, Inventory Management and FraudTesda CACSОценок пока нет

- Food and BeverageДокумент35 страницFood and BeverageLyn Escano50% (2)

- Standard RecipeДокумент5 страницStandard Reciperahulnavet75% (12)

- Issued: Oct 10 Hotel Accounting & Operation Manual Policies & Procedures Food & Beverage Cost Control Index N V-1Документ8 страницIssued: Oct 10 Hotel Accounting & Operation Manual Policies & Procedures Food & Beverage Cost Control Index N V-1mrshami7754Оценок пока нет

- Control Process PresentationДокумент47 страницControl Process PresentationReymart de SilvaОценок пока нет

- F&B StandardsДокумент5 страницF&B StandardsDeepak BillaОценок пока нет

- FNB Cost Control - Study Guide 3Документ10 страницFNB Cost Control - Study Guide 3mareng susanОценок пока нет

- 987 Food Cost ControlДокумент8 страниц987 Food Cost Controlalapanbanerjee132Оценок пока нет

- F&B ControlsДокумент23 страницыF&B Controlsdafni fernandesОценок пока нет

- Ashutosh Barman, 31284921010,6TH SEM, FOOD PRODUCTIONДокумент6 страницAshutosh Barman, 31284921010,6TH SEM, FOOD PRODUCTIONAshutosh BarmanОценок пока нет

- Knowledge Requirement 52Документ10 страницKnowledge Requirement 52sher_a_punjab5783Оценок пока нет

- Methods of PurchasingДокумент21 страницаMethods of PurchasingAnyango OburaОценок пока нет

- Food Cost ManualДокумент105 страницFood Cost Manualcucucucucu72Оценок пока нет

- Group2 reportingRMДокумент14 страницGroup2 reportingRMMarlo CondeОценок пока нет

- Kitchen Semester 1 Lecture 9Документ3 страницыKitchen Semester 1 Lecture 9Mehran GhafoorОценок пока нет

- F&B Cost ControlДокумент4 страницыF&B Cost Controlzuldvsb100% (1)

- F & B ManagementДокумент26 страницF & B ManagementAman KapurОценок пока нет

- Methods of Food PurchasingДокумент10 страницMethods of Food Purchasingrizzwan khanОценок пока нет

- Restaurant Accounting: For Profit's Sake - Inventory Your Beverage CostДокумент15 страницRestaurant Accounting: For Profit's Sake - Inventory Your Beverage CostronmoanaОценок пока нет

- Chapter 1: The Problem: Rationale and BackgroundДокумент21 страницаChapter 1: The Problem: Rationale and BackgroundadorableperezОценок пока нет

- F & B Notes For 8 TH SemДокумент15 страницF & B Notes For 8 TH SemTarun DagarОценок пока нет

- Audit Program: Food & Beverage Cost Control: Contributed January 30, 2002 by Sivanesan SivakaruniamДокумент4 страницыAudit Program: Food & Beverage Cost Control: Contributed January 30, 2002 by Sivanesan SivakaruniamAshraf HerzallaОценок пока нет

- LCCM Research Digest (November-December 2006)Документ8 страницLCCM Research Digest (November-December 2006)mis_administratorОценок пока нет

- Supply ChainДокумент3 страницыSupply ChainAli LamaaОценок пока нет

- COST CONTROL FOOD PRODUCTION CONTROL ModuleДокумент11 страницCOST CONTROL FOOD PRODUCTION CONTROL ModuleAndy Porcalla Aguanta100% (1)

- COST CONTROL FOOD PRODCUTION CONTROL ModuleДокумент11 страницCOST CONTROL FOOD PRODCUTION CONTROL ModuleLevirolfDeJesusОценок пока нет

- Lesson 4 Food and Beverage Cost ControlДокумент33 страницыLesson 4 Food and Beverage Cost ControlCindy SorianoОценок пока нет

- Cost Controlling in RestaurantsДокумент4 страницыCost Controlling in RestaurantsJenny Bautista100% (1)

- Food & Beverage Control NotesДокумент28 страницFood & Beverage Control NotesDr-Vaibhav Bhatt79% (98)

- LCCM Research Digest (November-December 2007 Ed.)Документ4 страницыLCCM Research Digest (November-December 2007 Ed.)mis_administratorОценок пока нет

- Serial Griller: ObjectivesДокумент4 страницыSerial Griller: ObjectivesBinsu DanielОценок пока нет

- 272 Food Cost ControlДокумент8 страниц272 Food Cost ControlProbaron BaruahОценок пока нет

- Kpis in WellnessДокумент5 страницKpis in WellnessAisha BarbieОценок пока нет

- 4.food and Beverage ControlДокумент9 страниц4.food and Beverage ControlsarathОценок пока нет

- Food Purchasing and Receiving Control - Food ControlДокумент24 страницыFood Purchasing and Receiving Control - Food ControlYatin BhatnagarОценок пока нет

- P1.T3. Financial Markets & Products Robert Mcdonald, Derivatives Markets, 3Rd Edition Bionic Turtle FRM Study Notes Reading 20Документ18 страницP1.T3. Financial Markets & Products Robert Mcdonald, Derivatives Markets, 3Rd Edition Bionic Turtle FRM Study Notes Reading 20Garima GulatiОценок пока нет

- Chapter 1 - Mercantilism: A) Meaning and Definition of MercantilismДокумент7 страницChapter 1 - Mercantilism: A) Meaning and Definition of MercantilismHasnath AhmedОценок пока нет

- Bcog-171 DoneДокумент4 страницыBcog-171 Donevaishnav v kunnathОценок пока нет

- Partido State University: Republic of The PhilippinesДокумент5 страницPartido State University: Republic of The PhilippinesEmmanuel GarciaОценок пока нет

- LME Monthly Overview March 2021Документ20 страницLME Monthly Overview March 2021Tram Le ThuyОценок пока нет

- Kuhn Trading With The Cup With HandleДокумент7 страницKuhn Trading With The Cup With HandlebengaltigerОценок пока нет

- Market Order Vs Limit OrderДокумент15 страницMarket Order Vs Limit OrderJeemol RajiОценок пока нет

- Pepperstone Reviewwbfvb PDFДокумент24 страницыPepperstone Reviewwbfvb PDFeventbelief8Оценок пока нет

- Producer and Optimal Production ChoiceДокумент20 страницProducer and Optimal Production ChoiceSangram sahooОценок пока нет

- Equity Futures - Margin Calculator - Alice Blue - Lowest Brokerage Online Trading Account in India PDFДокумент16 страницEquity Futures - Margin Calculator - Alice Blue - Lowest Brokerage Online Trading Account in India PDFsusman paulОценок пока нет

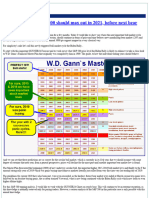

- Neil A Costa. W.D. Gann - Market MasterДокумент6 страницNeil A Costa. W.D. Gann - Market MasterAzariahJohn100% (1)

- The Cardinal and Ordinal Utility Theories of ConsumptionДокумент8 страницThe Cardinal and Ordinal Utility Theories of ConsumptionTaniya SinhaОценок пока нет

- LVL 1 Frostglade Tundra - The HomebreweryДокумент29 страницLVL 1 Frostglade Tundra - The HomebreweryLeandro ChavezОценок пока нет

- DerivativesДокумент10 страницDerivativesPARASОценок пока нет

- RMD New SyllabusДокумент4 страницыRMD New SyllabusRancho RanchoОценок пока нет

- LME Steel Scrap FactsheetДокумент2 страницыLME Steel Scrap FactsheetMark D.Оценок пока нет

- CH 2Документ14 страницCH 2SITI NABILAH OTHMANОценок пока нет

- JFC Indicator Package Users Manual 1Документ20 страницJFC Indicator Package Users Manual 1trinugroho100% (1)

- Commodity Trading StrategiesДокумент28 страницCommodity Trading StrategiesSatha Sivam0% (1)

- Vikram Commerce Academy: Class - 11 (Micro Econoomics)Документ21 страницаVikram Commerce Academy: Class - 11 (Micro Econoomics)CAVikramPratapSinghОценок пока нет

- Demand PDFДокумент15 страницDemand PDFHasan RabyОценок пока нет

- Varian - Chapter06 - Demand - Properties of Demand FunctionsДокумент14 страницVarian - Chapter06 - Demand - Properties of Demand FunctionsBella NovitasariОценок пока нет

- Trailblazers Leading The Way in The Near Future ReportДокумент2 страницыTrailblazers Leading The Way in The Near Future Reports1yksdc700Оценок пока нет

- Introduction To Financial Derivatives: Presented by Arjun Parthasarathy 28 June 2006Документ39 страницIntroduction To Financial Derivatives: Presented by Arjun Parthasarathy 28 June 2006Harsh ShahОценок пока нет

- Derivative Strategies: Research Paper OnДокумент13 страницDerivative Strategies: Research Paper OnSapna KesurОценок пока нет

- UntitledДокумент30 страницUntitledTaukirОценок пока нет

- IAS 2 SummaryДокумент3 страницыIAS 2 SummaryusmanameerОценок пока нет

- 19 HPLC Drain Bottles Caps - End UserДокумент3 страницы19 HPLC Drain Bottles Caps - End Userapi-220622714Оценок пока нет

- Gunner Newsletter On YEars Prediction in Stock MKTДокумент7 страницGunner Newsletter On YEars Prediction in Stock MKTPasupathi SОценок пока нет

- Instructions / Checklist For Filling KYC FormДокумент13 страницInstructions / Checklist For Filling KYC Formsuraj rautОценок пока нет