Вам также может понравиться

- Chapter 1 Solutions Horngren Cost AccountingДокумент14 страницChapter 1 Solutions Horngren Cost AccountingAnik Kumar MallickОценок пока нет

- Decision MakingДокумент15 страницDecision MakingSiddhant SangalОценок пока нет

- Acca F5Документ133 страницыAcca F5Andin Lee67% (3)

- Responsibility Accounting Decision MakingДокумент32 страницыResponsibility Accounting Decision MakingChokie NavarroОценок пока нет

- U04 Cost Accumulation SystemДокумент30 страницU04 Cost Accumulation SystemIslam AhmedОценок пока нет

- Cost Accounting - Exercise 1Документ2 страницыCost Accounting - Exercise 1Anna MaglinteОценок пока нет

- M6 Short Run Decision Making Relevant CostingДокумент6 страницM6 Short Run Decision Making Relevant Costingwingsenigma 00Оценок пока нет

- Weygandt Managerial 6e SM Release To Printer Ch07 NДокумент58 страницWeygandt Managerial 6e SM Release To Printer Ch07 NNgàyMaiTrờiLạiSángОценок пока нет

- Session 7 & Ic - PGDM 2021 - 23Документ28 страницSession 7 & Ic - PGDM 2021 - 23Krishnapriya NairОценок пока нет

- Relevant Costing NotesДокумент27 страницRelevant Costing NotesAnru PienaarОценок пока нет

- MCQ 14Документ2 страницыMCQ 14Avishek BarmanОценок пока нет

- Cost Ii Chapter 5Документ13 страницCost Ii Chapter 5Biniyam TsegayeОценок пока нет

- Unit Five: Relevant Information and Decision MakingДокумент39 страницUnit Five: Relevant Information and Decision MakingEbsa AbdiОценок пока нет

- Cost AccountingДокумент40 страницCost AccountingJaypee FazoliОценок пока нет

- Chapter 5Документ37 страницChapter 5Korubel Asegdew YimenuОценок пока нет

- Cost and Management AccountДокумент7 страницCost and Management AccountMsKhan0078Оценок пока нет

- Marginal Costing: Definition: (CIMA London)Документ4 страницыMarginal Costing: Definition: (CIMA London)Pankaj2cОценок пока нет

- P1 Solution CMA June 2019Документ7 страницP1 Solution CMA June 2019Awal ShekОценок пока нет

- ACC102-Chapter10new 000Документ28 страницACC102-Chapter10new 000Mikee FactoresОценок пока нет

- CHAPTER FOUR Cost and MGMT ACCTДокумент12 страницCHAPTER FOUR Cost and MGMT ACCTFeleke TerefeОценок пока нет

- Q3Finance Notes BookДокумент13 страницQ3Finance Notes Booksebastian.vduurenОценок пока нет

- MG WE FNSACC517 Provide Management Accounting InformationДокумент9 страницMG WE FNSACC517 Provide Management Accounting InformationGurpreet KaurОценок пока нет

- CH 20 SMДокумент31 страницаCH 20 SMNafisah MambuayОценок пока нет

- CostingДокумент32 страницыCostingnidhiОценок пока нет

- Managerial Accounting by James JiambalvoДокумент52 страницыManagerial Accounting by James JiambalvoAhmed AliОценок пока нет

- Assignment 1Документ7 страницAssignment 1Ahmed SuhailОценок пока нет

- Pricing and Short Term Decision Making (Edited)Документ58 страницPricing and Short Term Decision Making (Edited)Vaibhav SuchdevaОценок пока нет

- P2 - Performance ManagementДокумент11 страницP2 - Performance ManagementWashington ShamuyariraОценок пока нет

- Chapter Five Decision Making and Relevant Information Information and The Decision ProcessДокумент10 страницChapter Five Decision Making and Relevant Information Information and The Decision ProcesskirosОценок пока нет

- CAT T7 Key NotesДокумент31 страницаCAT T7 Key NotesMariam NawazОценок пока нет

- Part1 SEC BДокумент135 страницPart1 SEC BKhel MatiasОценок пока нет

- Write Advantages and Disadvantages of Cost AccountingДокумент6 страницWrite Advantages and Disadvantages of Cost AccountingAditya ManglamОценок пока нет

- Unit 7 Cost Accumulation TechniquesДокумент21 страницаUnit 7 Cost Accumulation Techniquesestihdaf استهدافОценок пока нет

- Difference Between Absorption Costing and Marginal CostingДокумент4 страницыDifference Between Absorption Costing and Marginal CostingIndu GuptaОценок пока нет

- P2 - Performance ManagementДокумент11 страницP2 - Performance Managementmrshami7754Оценок пока нет

- Relevant Costing and Differential AnalysisДокумент32 страницыRelevant Costing and Differential AnalysisEj BalbzОценок пока нет

- Chap002 Cost TermsДокумент41 страницаChap002 Cost TermsNgái Ngủ100% (1)

- Cma Ii CH 1Документ18 страницCma Ii CH 1Mubarik HedrОценок пока нет

- Relevant Costs For Decision Making: Topic Six & SevenДокумент53 страницыRelevant Costs For Decision Making: Topic Six & Sevendanial haziqОценок пока нет

- Session 02 CostsДокумент28 страницSession 02 CostsReya ZeeОценок пока нет

- CAT T7 Key NotesДокумент30 страницCAT T7 Key NotesSeah Chooi KhengОценок пока нет

- Additional FINAL ReviewДокумент41 страницаAdditional FINAL ReviewMandeep SinghОценок пока нет

- Week 5 Lecture Handout - Sols TemplateДокумент3 страницыWeek 5 Lecture Handout - Sols TemplateRavinesh PrasadОценок пока нет

- Cost&Management Accounting Unit-2 PDFДокумент19 страницCost&Management Accounting Unit-2 PDFVishal RanjanОценок пока нет

- New CMA Part 1 Section BДокумент135 страницNew CMA Part 1 Section Bhmtairek85100% (1)

- Ma Revision Notes All Chapters Week 1 9Документ87 страницMa Revision Notes All Chapters Week 1 9fabianngxinlongОценок пока нет

- Summary and Reflection: Chapter 6: Cost-Volume-ProfitДокумент5 страницSummary and Reflection: Chapter 6: Cost-Volume-ProfitJohn Kenneth BoholОценок пока нет

- Chap. II - Relevant Information 2Документ28 страницChap. II - Relevant Information 2ybegduОценок пока нет

- Lecture Aid - Relevant Costing Sumr 15Документ2 страницыLecture Aid - Relevant Costing Sumr 15Jaira MoradaОценок пока нет

- Unit 3 Acct312-UnlockedДокумент21 страницаUnit 3 Acct312-UnlockedTilahun GirmaОценок пока нет

- MODULE 1.exercises - Answers OnlyДокумент6 страницMODULE 1.exercises - Answers OnlykonyatanОценок пока нет

- CA IPCC Cost Accounting Theory Notes On All Chapters by 4EG3XQ31Документ50 страницCA IPCC Cost Accounting Theory Notes On All Chapters by 4EG3XQ31Bala RanganathОценок пока нет

- Cost Accounitng NotesДокумент17 страницCost Accounitng NotesDarlene JoyceОценок пока нет

- Cost AccountingДокумент9 страницCost AccountingPuneet TandonОценок пока нет

- Chapter 3 AkmenДокумент28 страницChapter 3 AkmenRomi AlfikriОценок пока нет

- Q.9. Differentiate Direct Cost and Direct Costing?Документ10 страницQ.9. Differentiate Direct Cost and Direct Costing?Hami KhaNОценок пока нет

- MCC 202 Advanced Cost AccountingДокумент4 страницыMCC 202 Advanced Cost AccountingNeoHoodaОценок пока нет

- Management Accounting Strategy Study Resource for CIMA Students: CIMA Study ResourcesОт EverandManagement Accounting Strategy Study Resource for CIMA Students: CIMA Study ResourcesОценок пока нет

- Management Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageОт EverandManagement Accounting: Decision-Making by Numbers: Business Strategy & Competitive AdvantageРейтинг: 5 из 5 звезд5/5 (1)

- Manufacturing Wastes Stream: Toyota Production System Lean Principles and ValuesОт EverandManufacturing Wastes Stream: Toyota Production System Lean Principles and ValuesРейтинг: 4.5 из 5 звезд4.5/5 (3)

- Reviewer For PartnershipДокумент31 страницаReviewer For PartnershipJohn Michael BabasОценок пока нет

- Chapt-11 Income Tax - IndividualsДокумент10 страницChapt-11 Income Tax - Individualshumnarvios100% (4)

- Gross Income: Income Taxation 5Th Edition (By: Valencia & Roxas) Suggested AnswersДокумент7 страницGross Income: Income Taxation 5Th Edition (By: Valencia & Roxas) Suggested AnswersAnonymous qpUaTkОценок пока нет

- Comple CДокумент1 страницаComple CPaula Cxerna GacisОценок пока нет

- Additional Chapter AssignmentДокумент4 страницыAdditional Chapter AssignmentM GualОценок пока нет

- Social Science and Philosophy BSMAДокумент5 страницSocial Science and Philosophy BSMAKia Kristine love SilverioОценок пока нет

- BMssДокумент152 страницыBMssCfhunSaatОценок пока нет

- Chapter 19 Applied ProblemДокумент5 страницChapter 19 Applied ProblemJarrett LindseyОценок пока нет

- Ba 115Документ36 страницBa 115Paul Rainer De VillaОценок пока нет

- CA. Naresh Aggarwal's Classes: Chapter-1 Basic Concepts of Cost AccountingДокумент8 страницCA. Naresh Aggarwal's Classes: Chapter-1 Basic Concepts of Cost AccountingNistha BishtОценок пока нет

- Cpa Review School of The Philippines Manila Management Advisory Services Relevant CostingДокумент27 страницCpa Review School of The Philippines Manila Management Advisory Services Relevant CostingJessaОценок пока нет

- Fundamentals of Accounting IiДокумент14 страницFundamentals of Accounting IiNo MoreОценок пока нет

- Management Advisory Services: BudgetedДокумент26 страницManagement Advisory Services: Budgetedi hate youtubersОценок пока нет

- Cost Volume Profit Analysis SolutionsДокумент8 страницCost Volume Profit Analysis SolutionsIce Voltaire Buban GuiangОценок пока нет

- Variable Costing and Segment Reporting: Tools For Management Reporting: Tools For ManagementДокумент14 страницVariable Costing and Segment Reporting: Tools For Management Reporting: Tools For Managementemadhamdy2002Оценок пока нет

- Relevant Costs For Decision Making: Exercise 13-1 (15 Minutes)Документ18 страницRelevant Costs For Decision Making: Exercise 13-1 (15 Minutes)YHОценок пока нет

- Acn 3Документ5 страницAcn 3Navidul IslamОценок пока нет

- Akuntansi Manajemen Lanjutan: Job Order Costing Dan Process CostingДокумент16 страницAkuntansi Manajemen Lanjutan: Job Order Costing Dan Process Costingsilvia gynaОценок пока нет

- CVPДокумент2 страницыCVPDan RyanОценок пока нет

- ACCA F2 Course NotesДокумент494 страницыACCA F2 Course NotesТурал Мансумов100% (4)

- M5Документ1 страницаM5Kendrew SujideОценок пока нет

- Fnu Fee StructureДокумент83 страницыFnu Fee StructurenicksneelОценок пока нет

- Manufacturing Cost Data For Copa Company: Case A Case B Case CДокумент5 страницManufacturing Cost Data For Copa Company: Case A Case B Case Cyogi fetriansyahОценок пока нет

- UGBA 102B Section02 - Handout - SolutionsДокумент11 страницUGBA 102B Section02 - Handout - SolutionsGwendolyn Chloe PurnamaОценок пока нет

- E-Book Chapter 1Документ56 страницE-Book Chapter 1jovanaОценок пока нет

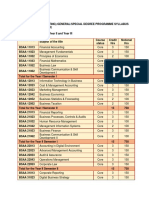

- BSC Applied Accounting Degree Programme Syllabus Programme StructureДокумент2 страницыBSC Applied Accounting Degree Programme Syllabus Programme StructureNaveen Pragash100% (1)

- Act512 - Assignment Chapter - 06Документ9 страницAct512 - Assignment Chapter - 06Rafin MahmudОценок пока нет

- MAS 9204 Product Costing Activity-Based Costing (ABC)Документ19 страницMAS 9204 Product Costing Activity-Based Costing (ABC)Mila Casandra CastañedaОценок пока нет

- Management Accounting Study NotesДокумент39 страницManagement Accounting Study NotesAlexander TrovatoОценок пока нет

- Methods InventoryДокумент12 страницMethods InventoryJocelyn LimaОценок пока нет

- Book1 Group Act5110Документ9 страницBook1 Group Act5110SAMОценок пока нет