Вам также может понравиться

- Ksa On Fdi in Retail 188Документ4 страницыKsa On Fdi in Retail 188Cuute PrinceszОценок пока нет

- Presentationonhaldiram 090813075702 Phpapp01Документ19 страницPresentationonhaldiram 090813075702 Phpapp01Yogesh SharmaОценок пока нет

- Student HandbookДокумент23 страницыStudent HandbookCuute PrinceszОценок пока нет

- Islamic Banking ProjectДокумент8 страницIslamic Banking ProjectUmarJavaid100% (1)

- Islamic BankingДокумент10 страницIslamic BankingCuute PrinceszОценок пока нет

- DeepikaДокумент71 страницаDeepikaSanjay DumbreОценок пока нет

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (890)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (265)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2219)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (119)

- InwaДокумент3 страницыInwadfgrtg454gОценок пока нет

- Salary Loan Application FormДокумент2 страницыSalary Loan Application FormRyan PangaluanОценок пока нет

- ELECTION LAW Case Doctrines PDFДокумент24 страницыELECTION LAW Case Doctrines PDFRio SanchezОценок пока нет

- Why Discovery Garden Is The Right Choice For Residence and InvestmentsДокумент3 страницыWhy Discovery Garden Is The Right Choice For Residence and InvestmentsAleem Ahmad RindekharabatОценок пока нет

- Itp Installation of 11kv HV Switchgear Rev.00Документ2 страницыItp Installation of 11kv HV Switchgear Rev.00syed fazluddin100% (1)

- DTCP DCR IiДокумент252 страницыDTCP DCR IiCharles Samuel100% (1)

- VDS 2095 Guidelines For Automatic Fire Detection and Fire Alarm Systems - Planning and InstallationДокумент76 страницVDS 2095 Guidelines For Automatic Fire Detection and Fire Alarm Systems - Planning and Installationjavikimi7901Оценок пока нет

- Soc Sci PT 3Документ6 страницSoc Sci PT 3Nickleson LabayОценок пока нет

- Kabul - GIZ Staff Member Killed in ExplosionДокумент2 страницыKabul - GIZ Staff Member Killed in Explosionlailuma dawoodiОценок пока нет

- Nuclear Non-Proliferation Treaty (NPT) : Why It MattersДокумент2 страницыNuclear Non-Proliferation Treaty (NPT) : Why It MattersUsama hameedОценок пока нет

- Legal Standoff Over Fine LiabilityДокумент1 страницаLegal Standoff Over Fine Liabilityrmaq100% (1)

- Caballes V CAДокумент2 страницыCaballes V CATintin CoОценок пока нет

- Standard Joist Load TablesДокумент122 страницыStandard Joist Load TablesNicolas Fuentes Von KieslingОценок пока нет

- Criminal Revision 11 of 2019Документ2 страницыCriminal Revision 11 of 2019wanyamaОценок пока нет

- Chapter 2 - National Difference in Political EconomyДокумент52 страницыChapter 2 - National Difference in Political EconomyTroll Nguyễn VănОценок пока нет

- Cat Come Back Stories - Pisi Vino InapoiДокумент20 страницCat Come Back Stories - Pisi Vino InapoiNicoletaОценок пока нет

- Disbursement VoucherДокумент5 страницDisbursement VoucherFonzy RoneОценок пока нет

- General and Subsidiary Ledgers ExplainedДокумент57 страницGeneral and Subsidiary Ledgers ExplainedSavage NicoОценок пока нет

- Gapol - Ro 03 The Tenses Present Perfect Simple Vs Past SimpleДокумент7 страницGapol - Ro 03 The Tenses Present Perfect Simple Vs Past SimpleDanielSimion100Оценок пока нет

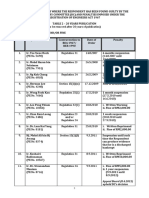

- LIST OF HEARING CASES WHERE THE RESPONDENT HAS BEEN FOUND GUILTYДокумент1 страницаLIST OF HEARING CASES WHERE THE RESPONDENT HAS BEEN FOUND GUILTYDarrenОценок пока нет

- The Statue of Liberty: Nonfiction Reading TestДокумент4 страницыThe Statue of Liberty: Nonfiction Reading TestMargarida RibeiroОценок пока нет

- Philippines Supreme Court Upholds Murder ConvictionДокумент4 страницыPhilippines Supreme Court Upholds Murder ConvictionJoy NavalesОценок пока нет

- Petitioners: La Bugal-B'Laan Tribal Association Inc, Rep. Chariman F'Long Miguel Lumayong Etc Respondent: Secretary Victor O. Ramos, DENR EtcДокумент2 страницыPetitioners: La Bugal-B'Laan Tribal Association Inc, Rep. Chariman F'Long Miguel Lumayong Etc Respondent: Secretary Victor O. Ramos, DENR EtcApple Gee Libo-onОценок пока нет

- Sing To The Dawn 2Документ4 страницыSing To The Dawn 2Nur Nabilah80% (5)

- MOA Establishes 50-Hectare Model Agroforestry FarmДокумент8 страницMOA Establishes 50-Hectare Model Agroforestry FarmENRO NRRGОценок пока нет

- Tax Invoice: State Name Delhi, Code 07Документ1 страницаTax Invoice: State Name Delhi, Code 07Ritesh pandeyОценок пока нет

- San Miguel CorpДокумент6 страницSan Miguel CorpMonster BebeОценок пока нет

- CHM580Документ7 страницCHM580Azreen AnisОценок пока нет

- VMware VSphere ICM 6.7 Lab ManualДокумент142 страницыVMware VSphere ICM 6.7 Lab Manualitnetman93% (29)

- AGAG v. Alpha FinancingДокумент5 страницAGAG v. Alpha Financinghermione_granger10Оценок пока нет