Вам также может понравиться

- PKF-HR Hunter 2012Документ26 страницPKF-HR Hunter 2012danilo_papaleoОценок пока нет

- 6 Consumer Business Baasdasdsanking Investor Day FINALДокумент36 страниц6 Consumer Business Baasdasdsanking Investor Day FINALAfiq KhidhirОценок пока нет

- Fourth Quarter 2012: Office Market Dashboard - Greater Toronto AreaДокумент5 страницFourth Quarter 2012: Office Market Dashboard - Greater Toronto Areaapi-26443221Оценок пока нет

- Metro Forecast Jan 2012Документ5 страницMetro Forecast Jan 2012Anonymous Feglbx5Оценок пока нет

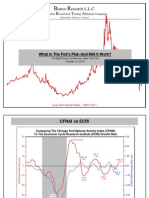

- Ianco Esearch L.L.C. A R T A: What Is The Fed's Plan and Will It Work?Документ44 страницыIanco Esearch L.L.C. A R T A: What Is The Fed's Plan and Will It Work?annawitkowski88Оценок пока нет

- M & A Fisrt DraftДокумент19 страницM & A Fisrt Draftrahul422Оценок пока нет

- The Mechanics of Finance: The Federal Reserve With Komal Sri - Kumar.Документ33 страницыThe Mechanics of Finance: The Federal Reserve With Komal Sri - Kumar.National Press FoundationОценок пока нет

- BNL Stores' Declining ProfitabilityДокумент16 страницBNL Stores' Declining ProfitabilityAMBWANI NAREN MAHESHОценок пока нет

- Dziczek DABE January 2012Документ30 страницDziczek DABE January 2012Carlos RamosОценок пока нет

- PWC Financial Institution Continuous Cost ManagementДокумент40 страницPWC Financial Institution Continuous Cost ManagementhellowodОценок пока нет

- IAB Internet Advertising Revenue Report: 2012 First Six Months' Results October 2012Документ25 страницIAB Internet Advertising Revenue Report: 2012 First Six Months' Results October 2012api-192935904Оценок пока нет

- Pitchbook-4Q 2012 VC Rundown FINALДокумент19 страницPitchbook-4Q 2012 VC Rundown FINALJohn CookОценок пока нет

- Prime Bank LTD: Dse: Primebank Bloomberg: PB:BDДокумент13 страницPrime Bank LTD: Dse: Primebank Bloomberg: PB:BDSajidHuqAmitОценок пока нет

- Retail Performance ReportДокумент91 страницаRetail Performance ReportanuttamanОценок пока нет

- Illinois Tool Works Inc. Valuation and RecommendationДокумент30 страницIllinois Tool Works Inc. Valuation and Recommendationgaru1991Оценок пока нет

- Lakewood - Budget Study Session 06-11-13Документ102 страницыLakewood - Budget Study Session 06-11-13Lakewood News ReporterОценок пока нет

- Net Leased Research ReportДокумент3 страницыNet Leased Research ReportnetleaseОценок пока нет

- Nielsen VN - Personal Finance Monitor Mid-Year 2010Документ42 страницыNielsen VN - Personal Finance Monitor Mid-Year 2010OscarKhuongОценок пока нет

- Employment Tracker December 2011Документ2 страницыEmployment Tracker December 2011William HarrisОценок пока нет

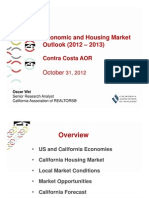

- 10-31-12 Contra Costa AORДокумент97 страниц10-31-12 Contra Costa AORjavthakОценок пока нет

- CBRE North America CapRate 2014H2 MasterДокумент51 страницаCBRE North America CapRate 2014H2 MasterAnonymous pWGhTF8eОценок пока нет

- Epartment OF Inance: 2014 C C B S 25, 2013Документ9 страницEpartment OF Inance: 2014 C C B S 25, 2013api-237071663Оценок пока нет

- ON SEMI Annual Shareholder Meeting Presentation - FINALДокумент22 страницыON SEMI Annual Shareholder Meeting Presentation - FINALbeneyuenОценок пока нет

- Final Review Session SPR12RปДокумент10 страницFinal Review Session SPR12RปFight FionaОценок пока нет

- Impact of Recession On Hotel IndustryДокумент22 страницыImpact of Recession On Hotel Industryarchanadandekar100% (1)

- HSON Investor Presentation - Baird - FinalДокумент17 страницHSON Investor Presentation - Baird - Finalbrlam10011021Оценок пока нет

- CIMA p1 March 2011 Post Exam GuideДокумент18 страницCIMA p1 March 2011 Post Exam GuidearkadiiОценок пока нет

- Impact of CDC Fund Investments 2004-12, Nov 2015Документ11 страницImpact of CDC Fund Investments 2004-12, Nov 2015Gavin McGillivrayОценок пока нет

- Turning The Corner, But No Material Pick-UpДокумент7 страницTurning The Corner, But No Material Pick-UpTaek-Geun KwonОценок пока нет

- Calculate Free Cash Flow using formulas and financial dataДокумент3 страницыCalculate Free Cash Flow using formulas and financial datadoan nguyenОценок пока нет

- Recent Challenges in Monetary Policy Design in India: Mridul SaggarДокумент38 страницRecent Challenges in Monetary Policy Design in India: Mridul SaggarbafnajayeshОценок пока нет

- CDS Spread To Default RiskДокумент22 страницыCDS Spread To Default Riskpriak11Оценок пока нет

- BarCap Credit Research 110312Документ32 страницыBarCap Credit Research 110312Henry WangОценок пока нет

- Market Outlook Market Outlook: Dealer's DiaryДокумент12 страницMarket Outlook Market Outlook: Dealer's DiaryAngel BrokingОценок пока нет

- Discounted Cash Flow (DCF) Model Tutorial and Dell Inc. Case StudyДокумент18 страницDiscounted Cash Flow (DCF) Model Tutorial and Dell Inc. Case StudySanket AdvilkarОценок пока нет

- Austin Realty Stats April 2012Документ12 страницAustin Realty Stats April 2012Romeo ManzanillaОценок пока нет

- FY 2014 Budget Status Final CorrectedДокумент74 страницыFY 2014 Budget Status Final Correctedted_nesiОценок пока нет

- Salary Survey MelbourneДокумент8 страницSalary Survey MelbournenikhilindiaОценок пока нет

- Investment Decisions and Capital Budgeting AnalysisДокумент9 страницInvestment Decisions and Capital Budgeting Analysisjamn1979Оценок пока нет

- Paradigm Real Estate PresentationДокумент15 страницParadigm Real Estate PresentationSumeet Mehta100% (1)

- A01150768 Problemascapitulos5y6 Tarea2 3 FinCorpAvДокумент5 страницA01150768 Problemascapitulos5y6 Tarea2 3 FinCorpAvAndrés Emmanuel NuñezОценок пока нет

- Forecast 12.09.11Документ1 страницаForecast 12.09.11Pensford FinancialОценок пока нет

- Local Youth Group: ? HEJ HI? /?IJ HIE #H 7J H I7F 7A 2008-2012Документ19 страницLocal Youth Group: ? HEJ HI? /?IJ HIE #H 7J H I7F 7A 2008-2012Rushbh PatilОценок пока нет

- Stock Research Report For HBC As of 8/17/11 - Chaikin Power ToolsДокумент4 страницыStock Research Report For HBC As of 8/17/11 - Chaikin Power ToolsChaikin Analytics, LLCОценок пока нет

- Q3 Travel Whitepaper UK Destination AnalysisДокумент19 страницQ3 Travel Whitepaper UK Destination Analysisyh76Оценок пока нет

- Thomson Reuters Company in Context Report: Bank of America Corporation (Bac-N)Документ6 страницThomson Reuters Company in Context Report: Bank of America Corporation (Bac-N)sinnlosОценок пока нет

- Responsive Document - CREW: Department of Education: Regarding For-Profit Education: 8/16/2011 - OUS 11-00026 - 2Документ750 страницResponsive Document - CREW: Department of Education: Regarding For-Profit Education: 8/16/2011 - OUS 11-00026 - 2CREWОценок пока нет

- Bus-530, Economic Conditions Analysis: Course Teacher: Dr. Tamgid Ahmed Chowdhury Associate Professor, SbeДокумент40 страницBus-530, Economic Conditions Analysis: Course Teacher: Dr. Tamgid Ahmed Chowdhury Associate Professor, SbeAfiqul IslamОценок пока нет

- Analyze Capital Projects Using NPV, IRR, Payback for Highest ReturnДокумент10 страницAnalyze Capital Projects Using NPV, IRR, Payback for Highest Returnwiwoaprilia100% (1)

- Madhucon Projects: Performance HighlightsДокумент13 страницMadhucon Projects: Performance HighlightsAngel BrokingОценок пока нет

- Test 2 Review QuestionsДокумент11 страницTest 2 Review QuestionsMae Justine Joy TajoneraОценок пока нет

- The Leads360 Lead Industry Report - 2010Документ26 страницThe Leads360 Lead Industry Report - 2010charger1234Оценок пока нет

- The Real Returns Report, Feb 13 2012Документ9 страницThe Real Returns Report, Feb 13 2012The Real Returns ReportОценок пока нет

- Enabling Customer Relationships: ExceptionalДокумент35 страницEnabling Customer Relationships: ExceptionaljatindbОценок пока нет

- Macroeconomic Relationships and Investment DecisionsДокумент3 страницыMacroeconomic Relationships and Investment DecisionsShuhada ShamsuddinОценок пока нет

- Federal Bank: Performance HighlightsДокумент11 страницFederal Bank: Performance HighlightsAngel BrokingОценок пока нет

- Larsen & ToubroДокумент15 страницLarsen & ToubroAngel BrokingОценок пока нет

- Final Valuation Report GSДокумент8 страницFinal Valuation Report GSGennadiy SverzhinskiyОценок пока нет

- Econ 299: Quantitative Methods in Economics CourseДокумент107 страницEcon 299: Quantitative Methods in Economics CourseElon MuskОценок пока нет

- Cocktail Investing: Distilling Everyday Noise into Clear Investment Signals for Better ReturnsОт EverandCocktail Investing: Distilling Everyday Noise into Clear Investment Signals for Better ReturnsОценок пока нет

- Investment Preferences of Government EmployeesДокумент8 страницInvestment Preferences of Government EmployeesSophia Delos SantosОценок пока нет

- Com Ad Module 2Документ10 страницCom Ad Module 2Gary AlaurinОценок пока нет

- The Clap Switch:: "T - W, LED - LED - LED - 100 - "Документ6 страницThe Clap Switch:: "T - W, LED - LED - LED - 100 - "ahsana29Оценок пока нет

- MGT602 Technical Article Theme 11aДокумент6 страницMGT602 Technical Article Theme 11aMujtaba AhmadОценок пока нет

- N MV Post Processor Manual EngДокумент36 страницN MV Post Processor Manual EnglastowlОценок пока нет

- in Re Guardianship of The Minors Tamboco, 36 Phil 939Документ4 страницыin Re Guardianship of The Minors Tamboco, 36 Phil 939Luigi JaroОценок пока нет

- Nu-Calgon Application BulletinДокумент4 страницыNu-Calgon Application BulletinJoe HollandОценок пока нет

- M1 PPT 1CДокумент35 страницM1 PPT 1CMarvin CincoОценок пока нет

- AIIMS Gorakhpur Patient Diet Services TenderДокумент36 страницAIIMS Gorakhpur Patient Diet Services TenderSumeet TripathiОценок пока нет

- Eterset Range Products CatalogueДокумент18 страницEterset Range Products CatalogueM Taufik WijayaОценок пока нет

- OptumG2: Examples of Optum Computational Engineering SoftwareДокумент262 страницыOptumG2: Examples of Optum Computational Engineering Softwaremed AmineОценок пока нет

- Vaishnavi Rayani: Career ObjectiveДокумент2 страницыVaishnavi Rayani: Career Objectiveruff stuffОценок пока нет

- Dicks Sporting GoodsДокумент6 страницDicks Sporting GoodsAnonymous 57oCRhtОценок пока нет

- File DisclosureДокумент465 страницFile DisclosureYaazziillatun NadhiyahОценок пока нет

- Design-of-2-MW-HYDRO POWER PLANT JETHRO GANELOДокумент8 страницDesign-of-2-MW-HYDRO POWER PLANT JETHRO GANELOjethro ganeloОценок пока нет

- 10 Constrcution Company-Bm2-Assingment-NocheДокумент16 страниц10 Constrcution Company-Bm2-Assingment-NocheJerick NocheОценок пока нет

- Enterovirus: From Wikipedia, The Free Encyclopedia Dari Wikipedia, Ensiklopedia BebasДокумент10 страницEnterovirus: From Wikipedia, The Free Encyclopedia Dari Wikipedia, Ensiklopedia BebasSri Lestary RamdhaniОценок пока нет

- Site Plan Vigyan BhawanДокумент8 страницSite Plan Vigyan BhawanWahab Hussain100% (1)

- Surface Vehicle Recommended PracticeДокумент5 страницSurface Vehicle Recommended Practicewilian_coelho3309Оценок пока нет

- 7 and 8Документ1 страница7 and 8Lionel Dsa0% (1)

- Investment BrokerageДокумент4 страницыInvestment BrokerageFileSharingОценок пока нет

- Stdplan Iae-M Ws 2017Документ37 страницStdplan Iae-M Ws 2017mehdiqОценок пока нет

- Silicon NPN Power Transistor: DescriptionДокумент2 страницыSilicon NPN Power Transistor: DescriptionBarry LeppanОценок пока нет

- Chemical cleaning reduces refinery downtimeДокумент4 страницыChemical cleaning reduces refinery downtimeWilfred OzerecОценок пока нет

- Mitsukuri 2014Документ13 страницMitsukuri 2014Ravi KankaleОценок пока нет

- ASTM D7015 - 07, Obtaining Intact Block (Cubical and Cylindrical) Samples of SoilsДокумент6 страницASTM D7015 - 07, Obtaining Intact Block (Cubical and Cylindrical) Samples of SoilsBárbara RodríguezОценок пока нет

- IMS Unision 4th Nat. Moot Memo (Respondent)Документ30 страницIMS Unision 4th Nat. Moot Memo (Respondent)Aman Uniyal100% (2)

- Apple Case StudyДокумент67 страницApple Case StudyCris Ezechial100% (2)

- Cathelco Evac ICPP ManualДокумент85 страницCathelco Evac ICPP ManualВладимир ПетрукОценок пока нет

- Speed Control of BLDC Motor For Electric PDFДокумент6 страницSpeed Control of BLDC Motor For Electric PDFtarnaОценок пока нет