Вам также может понравиться

- Abstract Ob After DoneДокумент6 страницAbstract Ob After DoneAditya ChauhanОценок пока нет

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- Abstract Ob After DoneДокумент6 страницAbstract Ob After DoneAditya ChauhanОценок пока нет

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- Bs PPT FulllДокумент8 страницBs PPT FulllAditya ChauhanОценок пока нет

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Project Report On HRM On HR Policies of Sbi BankДокумент57 страницProject Report On HRM On HR Policies of Sbi BankAditya Chauhan60% (10)

- SBI Report Banking Sector Report On HRДокумент66 страницSBI Report Banking Sector Report On HRAditya ChauhanОценок пока нет

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- Furnish Your Dream - Com: Plan Your Living RoomДокумент1 страницаFurnish Your Dream - Com: Plan Your Living RoomAditya ChauhanОценок пока нет

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Women EmpowerДокумент10 страницWomen EmpowerAditya ChauhanОценок пока нет

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- ITC Chairman SpeaksДокумент11 страницITC Chairman SpeaksAditya ChauhanОценок пока нет

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- Choco DayДокумент26 страницChoco DayAditya ChauhanОценок пока нет

- Chocoday 1Документ26 страницChocoday 1Aditya ChauhanОценок пока нет

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- Women EmpowerДокумент10 страницWomen EmpowerAditya ChauhanОценок пока нет

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

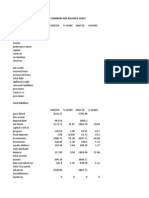

- Common Size Balance SheetДокумент9 страницCommon Size Balance SheetAditya ChauhanОценок пока нет

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- Muthoot Microfin Limited ChennaiДокумент79 страницMuthoot Microfin Limited ChennaivirtualatallОценок пока нет

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- 2011.06.30 ASX Annual ReportДокумент80 страниц2011.06.30 ASX Annual ReportKevin LinОценок пока нет

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (345)

- A STUDY On Financial Literacy Among Youths in MumbaiДокумент57 страницA STUDY On Financial Literacy Among Youths in Mumbaibhanushalidhruv59Оценок пока нет

- Root Capital: A Roadmap For ImpactДокумент32 страницыRoot Capital: A Roadmap For ImpactChris EngstromОценок пока нет

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- Financial Access and The Finance - Growth Nexus - Evidence From Developing Economies PDFДокумент16 страницFinancial Access and The Finance - Growth Nexus - Evidence From Developing Economies PDFSucatta IDОценок пока нет

- (Red Flags) Indicators of OID Source of Data: Over-Indebtedness Monitoring DashboardДокумент22 страницы(Red Flags) Indicators of OID Source of Data: Over-Indebtedness Monitoring DashboardKIMBERLY BALISACANОценок пока нет

- PNP Annual Report 2007-2008Документ8 страницPNP Annual Report 2007-2008partnersinprosperityОценок пока нет

- The Role of NGOs in Promoting EmpowermentДокумент8 страницThe Role of NGOs in Promoting EmpowermentpriyambansalОценок пока нет

- National Baseline Survey On Financial InclusionДокумент52 страницыNational Baseline Survey On Financial InclusionReal Ethan LopezОценок пока нет

- Feasibility ASKI Isabela PhilippinesДокумент96 страницFeasibility ASKI Isabela PhilippinesAyne Cabacungan50% (2)

- Tamansiswa Accounting Journal International Volume 8, No 1, January 2023Документ133 страницыTamansiswa Accounting Journal International Volume 8, No 1, January 2023suryaningОценок пока нет

- An Appraisal of Nigeria's Micro Small and Medium Enterprises MSMES Growth Challenges and Prospects.Документ15 страницAn Appraisal of Nigeria's Micro Small and Medium Enterprises MSMES Growth Challenges and Prospects.playcharles89Оценок пока нет

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- NGO List of PakistanДокумент168 страницNGO List of PakistanMansoor Siddique100% (1)

- Tigist BirhanuДокумент77 страницTigist Birhanuhabtamu100% (1)

- Strengthening Strategies of The Informal Sector in Traditional Market: An Institutional ApproachДокумент10 страницStrengthening Strategies of The Informal Sector in Traditional Market: An Institutional ApproachFirdaus DausОценок пока нет

- Arman Financial Services LTD (BSE Code 531179) - HBJ Capital's (MPS Unit) Business Insight Penny Stock Reco For June'10Документ52 страницыArman Financial Services LTD (BSE Code 531179) - HBJ Capital's (MPS Unit) Business Insight Penny Stock Reco For June'10sumansaha33Оценок пока нет

- VLOOKUPДокумент14 страницVLOOKUPJeetendra ShresthaОценок пока нет

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- Annual Report 2017Документ120 страницAnnual Report 2017mirzaОценок пока нет

- Final Presentation On Housing LoanДокумент40 страницFinal Presentation On Housing Loanadebo_yemiОценок пока нет

- Gbnews - Ch-Micro and Small Enterprises in Ethiopia Access To Credit Challenges and SolutionsДокумент6 страницGbnews - Ch-Micro and Small Enterprises in Ethiopia Access To Credit Challenges and Solutionsetebark h/michaleОценок пока нет

- The Definition of MicrofinanceДокумент6 страницThe Definition of MicrofinanceAyush BhavsarОценок пока нет

- SecuritizationДокумент10 страницSecuritizationSimon ChowОценок пока нет

- Financial InclusionДокумент25 страницFinancial InclusionSurbhi GuptaОценок пока нет

- Synopsis of MPhil PHD StudiesДокумент4 страницыSynopsis of MPhil PHD Studiestaiphi78Оценок пока нет

- A Study On The Performance of Microfinance InstituДокумент13 страницA Study On The Performance of Microfinance Institu娜奎Оценок пока нет

- Coop MGT - COOP - INSДокумент14 страницCoop MGT - COOP - INSJames ChuaОценок пока нет

- Frauds in Micro FinanceДокумент6 страницFrauds in Micro FinanceSyed MohammedОценок пока нет

- Microinsurance ProjectДокумент59 страницMicroinsurance Projectmayur9664501232Оценок пока нет

- Graduates of 2018/2019 AY: Eaching NstitutesДокумент256 страницGraduates of 2018/2019 AY: Eaching Nstitutesyimam seeidОценок пока нет

- Definition and Evolution of Microfinance PDFДокумент22 страницыDefinition and Evolution of Microfinance PDFKitt EmataОценок пока нет