Вам также может понравиться

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- Confidential Information Exchange AgreementДокумент6 страницConfidential Information Exchange AgreementRachelle Anne BillonesОценок пока нет

- M Taher & Co WorldECR Interview 01.04.19Документ4 страницыM Taher & Co WorldECR Interview 01.04.19sam ignarskiОценок пока нет

- The BlobДокумент3 страницыThe Blobsam ignarskiОценок пока нет

- A Tribute To John Banks: at A Golf Club in New MaldenДокумент3 страницыA Tribute To John Banks: at A Golf Club in New Maldensam ignarskiОценок пока нет

- Bill Birch Reynardson Obituary - The Daily Telegraph 16.8.2017Документ3 страницыBill Birch Reynardson Obituary - The Daily Telegraph 16.8.2017sam ignarskiОценок пока нет

- Mlaanz SMDG Event Sydney 2016Документ2 страницыMlaanz SMDG Event Sydney 2016sam ignarskiОценок пока нет

- Lmaa Seminar Singapore May 2016Документ2 страницыLmaa Seminar Singapore May 2016sam ignarskiОценок пока нет

- Shincho To KumoДокумент7 страницShincho To Kumosam ignarskiОценок пока нет

- Joe Hughes Speech 24MAY17Документ7 страницJoe Hughes Speech 24MAY17sam ignarskiОценок пока нет

- Happy HolidaysДокумент1 страницаHappy Holidayssam ignarskiОценок пока нет

- Moore & Co ComplaintДокумент50 страницMoore & Co Complaintsam ignarskiОценок пока нет

- Moore & Co ComplaintДокумент50 страницMoore & Co Complaintsam ignarskiОценок пока нет

- Moore and Co Precendential OpinionДокумент29 страницMoore and Co Precendential Opinionsam ignarskiОценок пока нет

- Wikborg Global Offshore Projects DEC15Документ13 страницWikborg Global Offshore Projects DEC15sam ignarskiОценок пока нет

- 2016 InterManager President New Year MessageДокумент3 страницы2016 InterManager President New Year Messagesam ignarskiОценок пока нет

- Nigerian National Petroleum Corporation July 2015 DirectiveДокумент7 страницNigerian National Petroleum Corporation July 2015 Directivesam ignarskiОценок пока нет

- PL Ferrari Newsletter 2-15Документ2 страницыPL Ferrari Newsletter 2-15sam ignarskiОценок пока нет

- ETL 2015 ProgramДокумент1 страницаETL 2015 Programsam ignarskiОценок пока нет

- Tysers P&I Report 2015Документ36 страницTysers P&I Report 2015sam ignarskiОценок пока нет

- AJG Marine P&I Commercial Market Review September 2015Документ94 страницыAJG Marine P&I Commercial Market Review September 2015sam ignarskiОценок пока нет

- Implications of Nigerian DirectiveДокумент4 страницыImplications of Nigerian Directivesam ignarskiОценок пока нет

- Row Around Singapore Island BrochureДокумент12 страницRow Around Singapore Island Brochuresam ignarskiОценок пока нет

- Michael DavarДокумент2 страницыMichael Davarsam ignarskiОценок пока нет

- The Clothes-Line RigДокумент5 страницThe Clothes-Line Rigsam ignarskiОценок пока нет

- Tysers P&I Update 08dec14Документ19 страницTysers P&I Update 08dec14sam ignarskiОценок пока нет

- George Grishin 30 Years in InsuranceДокумент18 страницGeorge Grishin 30 Years in Insurancesam ignarskiОценок пока нет

- New Year's Resolutions For The Transport Industry 2015Документ2 страницыNew Year's Resolutions For The Transport Industry 2015sam ignarskiОценок пока нет

- PLF Newsletter 08-14Документ2 страницыPLF Newsletter 08-14sam ignarskiОценок пока нет

- China Sample Pollution Response AgreementДокумент16 страницChina Sample Pollution Response Agreementsam ignarskiОценок пока нет

- Bow Wave Readers BreakdownДокумент6 страницBow Wave Readers Breakdownsam ignarskiОценок пока нет

- Lloyd's List Global Maritime Lawyer of The Year Acceptance Speech 30SEP14Документ2 страницыLloyd's List Global Maritime Lawyer of The Year Acceptance Speech 30SEP14sam ignarskiОценок пока нет

- Econ 101E (Hand-Out 2) 2019-Money-Time RelationshipДокумент13 страницEcon 101E (Hand-Out 2) 2019-Money-Time RelationshipFrancisco CarbonОценок пока нет

- Part 10 - Aleatory Contracts, Compromise, and Arbitration PDFДокумент7 страницPart 10 - Aleatory Contracts, Compromise, and Arbitration PDFalex_ang_6Оценок пока нет

- DasdasДокумент194 страницыDasdasHoriaОценок пока нет

- Digitally Signed by Reliance General Insurance Company Limited Date: 2023.02.23Документ7 страницDigitally Signed by Reliance General Insurance Company Limited Date: 2023.02.23mahakarthicОценок пока нет

- Huum - Info Shriram Life Insurance Company Wiki PRДокумент2 страницыHuum - Info Shriram Life Insurance Company Wiki PRRitik JainОценок пока нет

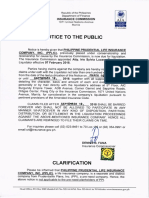

- Notice To The Public PPLIC Placed Under Liquidation Effective 07 Feb 2018Документ1 страницаNotice To The Public PPLIC Placed Under Liquidation Effective 07 Feb 2018Jerry MisterinoОценок пока нет

- General Condition of Contract PDFДокумент22 страницыGeneral Condition of Contract PDFErik SorianoОценок пока нет

- Ce 1402 Estimation and Quantity SurveyingДокумент26 страницCe 1402 Estimation and Quantity SurveyingNagaraja Prasanna RassОценок пока нет

- Utmost Good FaithДокумент219 страницUtmost Good FaithVikram Fernandez100% (1)

- Feb2019Документ3 страницыFeb2019జెల్ల ఉమేష్ అను నేనుОценок пока нет

- Actarial Risk TheoryДокумент2 страницыActarial Risk TheoryEtkin HasgülОценок пока нет

- IntroductionДокумент2 страницыIntroductionRukhsar Abbas Ali .Оценок пока нет

- Capital InsuranceДокумент8 страницCapital InsuranceLyn AvestruzОценок пока нет

- INSURANCE - Delsan Transport Line, Inc. - V - CaДокумент3 страницыINSURANCE - Delsan Transport Line, Inc. - V - Camichelle zatarainОценок пока нет

- Customer StatementДокумент18 страницCustomer Statementmuhyideen6abdulganiyОценок пока нет

- Blawreg 1Документ5 страницBlawreg 1Sammylyn Dela CruzОценок пока нет

- DBP Citizen'S CharterДокумент38 страницDBP Citizen'S CharterBien Bowie A. CortezОценок пока нет

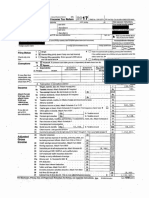

- Sanders IRS Filing 2017Документ21 страницаSanders IRS Filing 2017Stephanie Dube DwilsonОценок пока нет

- Atok Finance Corporation VsДокумент2 страницыAtok Finance Corporation VsTen LaplanaОценок пока нет

- Economic Analysis of Banking Regulation: © 2005 Pearson Education Canada IncДокумент15 страницEconomic Analysis of Banking Regulation: © 2005 Pearson Education Canada IncMuntazir HussainОценок пока нет

- 10.3 Term Sheet For Equity InvestmentДокумент12 страниц10.3 Term Sheet For Equity InvestmentMarius AngaraОценок пока нет

- Armchair EconomistДокумент17 страницArmchair EconomistSyam ThomasОценок пока нет

- Rcef SeedДокумент26 страницRcef Seedkuya ian0% (1)

- Pce Sample Questions 2016 - EngДокумент39 страницPce Sample Questions 2016 - EngImran Azman100% (1)

- Labor Panic Booklet2Документ107 страницLabor Panic Booklet2ulticonОценок пока нет

- Final-Activity 1 q2Документ2 страницыFinal-Activity 1 q2Hairoden MauntolОценок пока нет

- Anjali Final ReportДокумент51 страницаAnjali Final Reportpioneer professionalsОценок пока нет

- Role of Insurable Interest in Contingency Insurance and Indemnity InsuranceДокумент3 страницыRole of Insurable Interest in Contingency Insurance and Indemnity InsuranceKenneth CJ KemeОценок пока нет

- Canada-Ontario Affordable Housing Program: Rental and Supportive Program GuidelinesДокумент45 страницCanada-Ontario Affordable Housing Program: Rental and Supportive Program GuidelinesarthurmathieuОценок пока нет