Вам также может понравиться

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- CorruptionДокумент13 страницCorruptionJitin BhutaniОценок пока нет

- Vendor PlusДокумент24 страницыVendor PlusJitin BhutaniОценок пока нет

- MBA Sem-1st, 3rdДокумент1 страницаMBA Sem-1st, 3rdJitin BhutaniОценок пока нет

- Assignment: School of Management Studies Punjabi University PatialaДокумент10 страницAssignment: School of Management Studies Punjabi University PatialaJitin BhutaniОценок пока нет

- Presented by Roll Number - 6342Документ54 страницыPresented by Roll Number - 6342Jitin Bhutani100% (1)

- Assignment of Organizational DevelopmentДокумент3 страницыAssignment of Organizational DevelopmentJitin BhutaniОценок пока нет

- Ethics in Merger & AcquistiionДокумент44 страницыEthics in Merger & AcquistiionJitin BhutaniОценок пока нет

- An Experiential Approach To Organization Development 7 EditionДокумент39 страницAn Experiential Approach To Organization Development 7 EditionJitin BhutaniОценок пока нет

- Collective BargainingДокумент13 страницCollective BargainingAkash BafnaОценок пока нет

- Bharti Axa Life InsuranceДокумент81 страницаBharti Axa Life InsuranceJitin Bhutani100% (1)

- Accounting CycleДокумент39 страницAccounting CycleJitin Bhutani0% (1)

- Submitted By: Gurdev Singh Roll No. 120426366Документ16 страницSubmitted By: Gurdev Singh Roll No. 120426366Jitin BhutaniОценок пока нет

- 02working Capital Management - Navdeep Bajwa, SMS, Pbi Uni.Документ85 страниц02working Capital Management - Navdeep Bajwa, SMS, Pbi Uni.Jitin BhutaniОценок пока нет

- Human ProcessДокумент48 страницHuman ProcessJitin BhutaniОценок пока нет

- Entrepreneurial Quiz 2k13 Aptitude TestДокумент4 страницыEntrepreneurial Quiz 2k13 Aptitude TestJitin BhutaniОценок пока нет

- Introduction of Pnb,,,Improved FileДокумент10 страницIntroduction of Pnb,,,Improved FileJitin BhutaniОценок пока нет

- Introduction To Imf: International Monetary FundДокумент25 страницIntroduction To Imf: International Monetary FundJitin BhutaniОценок пока нет

- Brthdy 1225815250925041 9Документ11 страницBrthdy 1225815250925041 9Jitin BhutaniОценок пока нет

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- Final Zayredin AssignmentДокумент26 страницFinal Zayredin AssignmentAmanuelОценок пока нет

- Daniel F. Spulber - Global Competitive Strategy-Cambridge University Press (2007)Документ306 страницDaniel F. Spulber - Global Competitive Strategy-Cambridge University Press (2007)沈化文Оценок пока нет

- The Supply Chain Management Concept 1aДокумент20 страницThe Supply Chain Management Concept 1aMRK466100% (1)

- Oracle HCM On Cloud NotesДокумент9 страницOracle HCM On Cloud Notesckambara4362Оценок пока нет

- Personal Statement - ISEGДокумент2 страницыPersonal Statement - ISEGMirza Mohammad AliОценок пока нет

- Vijaychandran R 9629869676 Deputy Manager: May2019 - Aug 2019Документ2 страницыVijaychandran R 9629869676 Deputy Manager: May2019 - Aug 2019vijayfs2Оценок пока нет

- The Future of FinanceДокумент30 страницThe Future of FinanceRenuka SharmaОценок пока нет

- Quiz Stocks and Their ValuationДокумент3 страницыQuiz Stocks and Their ValuationBilly Vince AlquinoОценок пока нет

- Marketing Plan - ArongДокумент13 страницMarketing Plan - ArongMarshal Richard75% (4)

- Brush Up - Slide 1Документ1 страницаBrush Up - Slide 1Jasmine AlucimanОценок пока нет

- Details FM DATAДокумент212 страницDetails FM DATAAbhishek MishraОценок пока нет

- Automotive Industry OverviewДокумент3 страницыAutomotive Industry Overviewrumellemur59Оценок пока нет

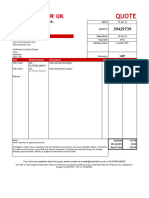

- Maximator Quote No 39429739Документ1 страницаMaximator Quote No 39429739William EvansОценок пока нет

- IBC Chap 2Документ28 страницIBC Chap 2Chilapalli SaikiranОценок пока нет

- Canara BankДокумент2 страницыCanara Banklinsonjohny34Оценок пока нет

- AS-18 ConceptДокумент5 страницAS-18 ConceptMohammad ArifОценок пока нет

- IMNU HimasnhuPatel Anand Rathi Internship ReportДокумент57 страницIMNU HimasnhuPatel Anand Rathi Internship ReportHimanshu Patel33% (3)

- HS ComProДокумент7 страницHS ComProgabrielОценок пока нет

- Blockholder Trading, Market E Ciency, and Managerial MyopiaДокумент35 страницBlockholder Trading, Market E Ciency, and Managerial MyopiamkatsotisОценок пока нет

- Customer Journey MappingДокумент1 страницаCustomer Journey MappingPriyanka RaniОценок пока нет

- Introduction To International Human Resource ManagementДокумент16 страницIntroduction To International Human Resource Managementashishapp88% (8)

- Business Hub: National Case Study Challenge 2021Документ13 страницBusiness Hub: National Case Study Challenge 2021HimansuRathiОценок пока нет

- Stock Control and InventoryДокумент8 страницStock Control and Inventoryadede2009Оценок пока нет

- BfinДокумент3 страницыBfinjonisugandaОценок пока нет

- A3 Problem-Solving: Title: A3 # Owner: TeamДокумент2 страницыA3 Problem-Solving: Title: A3 # Owner: TeamMayra HernándezОценок пока нет

- Risk Management For E-BusinessДокумент33 страницыRisk Management For E-BusinessDediNirtadinataAlQudsyОценок пока нет

- Department ProfileДокумент12 страницDepartment ProfileShambhavi JОценок пока нет

- Electives Term 5&6Документ28 страницElectives Term 5&6GaneshRathodОценок пока нет

- PPT, Final Report, Kshitij Negi, C-41Документ12 страницPPT, Final Report, Kshitij Negi, C-41Kshitij NegiОценок пока нет

- Annual Return of A Company (Other Than A Company Limited by Guarantee)Документ5 страницAnnual Return of A Company (Other Than A Company Limited by Guarantee)ramiduyasanОценок пока нет