Вам также может понравиться

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Apple V Samsung Jury Verdict 112113Документ2 страницыApple V Samsung Jury Verdict 112113techledesОценок пока нет

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5795)

- Opening Statement in US v. AppleДокумент81 страницаOpening Statement in US v. ApplequartznewsОценок пока нет

- Intertrust's Complaint For Patent InfringementДокумент44 страницыIntertrust's Complaint For Patent InfringementCNET NewsОценок пока нет

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- Apple AwardДокумент27 страницApple Awarderiq_gardner6833Оценок пока нет

- Apple Denied Motion For Permanent InjunctionДокумент23 страницыApple Denied Motion For Permanent InjunctionMikey CampbellОценок пока нет

- IA3 Mod 4 REДокумент12 страницIA3 Mod 4 REjulia4razoОценок пока нет

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Review of WACCДокумент37 страницReview of WACCBen SimsuangcoОценок пока нет

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- Chapter 16 Corporate ReportsДокумент25 страницChapter 16 Corporate ReportsRasool Bux KhaskheliОценок пока нет

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- PSABДокумент3 страницыPSABHotman JeffersonОценок пока нет

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- Prelim Examination 2021-2022Документ29 страницPrelim Examination 2021-2022Jenny Rose M. YocteОценок пока нет

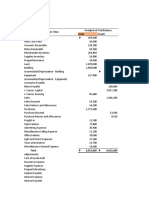

- Trial Balance-ROEMY BAKERYДокумент2 страницыTrial Balance-ROEMY BAKERYNurqomariyahОценок пока нет

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (345)

- Process of MergerДокумент7 страницProcess of MergerSankalp RajОценок пока нет

- Foundations in Accountancy FFA/ACCA FДокумент45 страницFoundations in Accountancy FFA/ACCA FTuyết Anh ĐồngОценок пока нет

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- Notes To Financial Statements - TheoryДокумент5 страницNotes To Financial Statements - Theoryricamae saladagaОценок пока нет

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- Annual ReportДокумент180 страницAnnual ReportParehjuiОценок пока нет

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- Audprob Final Exam 1Документ26 страницAudprob Final Exam 1Joody CatacutanОценок пока нет

- Kashato-Shirts MerchandisingДокумент3 страницыKashato-Shirts MerchandisingFred Wilson100% (1)

- Managerial Investment Decisions: Tools and AnalysisДокумент40 страницManagerial Investment Decisions: Tools and AnalysisRОценок пока нет

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- AUDITINGДокумент20 страницAUDITINGAngelieОценок пока нет

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Capital BudgetingДокумент52 страницыCapital BudgetingAbhimanyu ArjunОценок пока нет

- ClarksnexДокумент3 страницыClarksnexJoan MaduОценок пока нет

- Instructions: (2) Make Amortization Schedule For 3 YearsДокумент2 страницыInstructions: (2) Make Amortization Schedule For 3 YearsPatar ElmausОценок пока нет

- Assignment On Ratio AnalysisДокумент6 страницAssignment On Ratio AnalysisSurbhî GuptaОценок пока нет

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- RATIOS MEANING A Ratio Shows The Relationship Between Two Numbers.Документ15 страницRATIOS MEANING A Ratio Shows The Relationship Between Two Numbers.shru44Оценок пока нет

- Financial Statements AnalysisДокумент49 страницFinancial Statements AnalysisBilal MustafaОценок пока нет

- Guide To Accounting For Income Taxes NewДокумент620 страницGuide To Accounting For Income Taxes NewRahul Modi100% (1)

- Business Plan Chapter 6Документ4 страницыBusiness Plan Chapter 6charlottefrancesbagaoisanОценок пока нет

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- Sounak - OPCДокумент25 страницSounak - OPCSounak VermaОценок пока нет

- Procter and Gamble: Cost of CapitalДокумент64 страницыProcter and Gamble: Cost of CapitalShriniwas NeheteОценок пока нет

- Akuntansi BiayaДокумент41 страницаAkuntansi BiayaReyhan PratamaОценок пока нет

- Triple - M-Trading - SARAYДокумент10 страницTriple - M-Trading - SARAYLaiza Cristella SarayОценок пока нет

- Germany BranchДокумент2 страницыGermany BranchparuОценок пока нет

- Types of Companies Based On Number of Members:: 1. Private CompanyДокумент3 страницыTypes of Companies Based On Number of Members:: 1. Private CompanyNanee DОценок пока нет

- Sejarah Dan Misteri Gelombang Merger: Sebuah Perspektif Amerika Dan Inggris SuharyonoДокумент28 страницSejarah Dan Misteri Gelombang Merger: Sebuah Perspektif Amerika Dan Inggris SuharyonoAli SyabanaОценок пока нет

- Shivani Corporate Finance 8thДокумент15 страницShivani Corporate Finance 8thShivani Singh ChandelОценок пока нет