Вам также может понравиться

- Supporting Inclusive GrowthОт EverandSupporting Inclusive GrowthОценок пока нет

- Need For Financial Inclusion and Challenges Ahead - An Indian PerspectiveДокумент4 страницыNeed For Financial Inclusion and Challenges Ahead - An Indian PerspectiveInternational Organization of Scientific Research (IOSR)Оценок пока нет

- Financial Inclusion From BIMSДокумент14 страницFinancial Inclusion From BIMSDeepu T MathewОценок пока нет

- Research Paper On Financial InclusionДокумент57 страницResearch Paper On Financial InclusionChilaka Pappala0% (1)

- Financial Inclusion in India: A Theoritical Assesment: ManagementДокумент6 страницFinancial Inclusion in India: A Theoritical Assesment: ManagementVidhi BansalОценок пока нет

- Complete ProjectДокумент72 страницыComplete ProjectKevin JacobОценок пока нет

- Financial InclusionДокумент15 страницFinancial InclusionNitin SharmaОценок пока нет

- Financial Inclusion in India - A Review of Initiatives and AchievementsДокумент10 страницFinancial Inclusion in India - A Review of Initiatives and AchievementsRidhiОценок пока нет

- Emerging Trends in Banking Sector - A Comparative Study From Financial Inclusion PerspectiveДокумент13 страницEmerging Trends in Banking Sector - A Comparative Study From Financial Inclusion PerspectiveIAEME PublicationОценок пока нет

- College Magazine Latest KrishnanДокумент6 страницCollege Magazine Latest KrishnanChalil KrishnanОценок пока нет

- Franklin D. RooseveltДокумент17 страницFranklin D. RooseveltRupali RamtekeОценок пока нет

- Financial Inclusion: Issues and Challenges: December 2013Документ7 страницFinancial Inclusion: Issues and Challenges: December 2013Rjendra LamsalОценок пока нет

- FinancialInclusion RecentInitiativesandAssessmentДокумент39 страницFinancialInclusion RecentInitiativesandAssessmentShaneel AnijwalОценок пока нет

- Chapter 1 .Документ10 страницChapter 1 .AP GREEN ENERGY CORPORATION LIMITEDОценок пока нет

- Revised ProposalДокумент12 страницRevised ProposalSumanОценок пока нет

- 09 - Chapter 1Документ24 страницы09 - Chapter 1shantishree04Оценок пока нет

- Financial InclusionДокумент90 страницFinancial InclusionRohan Mehra0% (1)

- Anshu Bansal GuptaДокумент32 страницыAnshu Bansal Guptasahu_krishna1995Оценок пока нет

- Kushagra Amrit 1882053Документ16 страницKushagra Amrit 1882053Kushagra AmritОценок пока нет

- Financial Inclusion in India - A Review of InitiatДокумент11 страницFinancial Inclusion in India - A Review of InitiatEshan BedagkarОценок пока нет

- Chapter 1: Financial Inclusion - Global PerspectiveДокумент74 страницыChapter 1: Financial Inclusion - Global PerspectivenitmemberОценок пока нет

- The Role of SHGS in Financial Inclusion. A Case Study: Uma .H.R, Rupa.K.NДокумент5 страницThe Role of SHGS in Financial Inclusion. A Case Study: Uma .H.R, Rupa.K.NDevikaОценок пока нет

- Financial Inclusion - RBI - S InitiativesДокумент12 страницFinancial Inclusion - RBI - S Initiativessahil_saini298Оценок пока нет

- TCS Government Whitepaper Financial Inclusion 09 2010Документ26 страницTCS Government Whitepaper Financial Inclusion 09 2010ankitrathod87Оценок пока нет

- Fs - Financial InclusionДокумент7 страницFs - Financial InclusionWasim SОценок пока нет

- (2013 - IJMSSR) Dangi&Kumar - Current Situation of Financial Incl. in India PDFДокумент12 страниц(2013 - IJMSSR) Dangi&Kumar - Current Situation of Financial Incl. in India PDFMarkus WidodoОценок пока нет

- On Financial Inclusion A Must For Growth of Indian Economy: Summer Training ReportДокумент44 страницыOn Financial Inclusion A Must For Growth of Indian Economy: Summer Training ReportMahey HarishОценок пока нет

- IIBF Sample BookletДокумент39 страницIIBF Sample BookletMeghalaya CSCОценок пока нет

- Financial Inclusion Introduction andДокумент32 страницыFinancial Inclusion Introduction andAstik TripathiОценок пока нет

- Research Paper On Financial InclusionДокумент36 страницResearch Paper On Financial Inclusionimsarfrazkhan96% (28)

- Financial Inclusion Through Microfinance Vineeta Agrawal: Applied Sciences Department, KIIT College of EngineeringДокумент8 страницFinancial Inclusion Through Microfinance Vineeta Agrawal: Applied Sciences Department, KIIT College of EngineeringVineeta AgrawalОценок пока нет

- Financial Inclusion: Presented byДокумент20 страницFinancial Inclusion: Presented byjothiОценок пока нет

- Financial InclusionДокумент26 страницFinancial InclusionErick McdonaldОценок пока нет

- A Study On Awareness Towards Financial Inclusion Among Rural Areas With Special Reference To CoimbatoreДокумент27 страницA Study On Awareness Towards Financial Inclusion Among Rural Areas With Special Reference To CoimbatoreprathikshaОценок пока нет

- Financial Inclusion Literature Review PDFДокумент9 страницFinancial Inclusion Literature Review PDFaflsvwoeu100% (1)

- Financial Inclusion in India-13 PagesДокумент14 страницFinancial Inclusion in India-13 Pagessree anugraphicsОценок пока нет

- Rohit 500Документ6 страницRohit 500Shubham SainiОценок пока нет

- Project ReportДокумент79 страницProject ReportNigin K Abraham100% (1)

- Paper Presentation On Financial InclusionДокумент6 страницPaper Presentation On Financial InclusionaruvankaduОценок пока нет

- Financial Inclusion in IndiaДокумент20 страницFinancial Inclusion in IndiaSameer Singh FPM Student, Jaipuria LucknowОценок пока нет

- Financial Inclusion - Issues in Measurement and Analysis: M.ShahulhameeduДокумент9 страницFinancial Inclusion - Issues in Measurement and Analysis: M.ShahulhameeduKkkkОценок пока нет

- Growth Through Financial Inclusion in IndiaДокумент14 страницGrowth Through Financial Inclusion in IndiarmindraeОценок пока нет

- Financial InclusionДокумент96 страницFinancial InclusionIcaii Infotech100% (6)

- Dialnet RoleOfBanksInNancialInclusionInIndia 6030517Документ13 страницDialnet RoleOfBanksInNancialInclusionInIndia 6030517AnonymousОценок пока нет

- Financial InclusionДокумент6 страницFinancial InclusionRaja SekaranОценок пока нет

- Financial Inclusion African Finance Journal 14102010Документ22 страницыFinancial Inclusion African Finance Journal 14102010Mallikarjun DОценок пока нет

- Variation and Determinants of Financial Inclusion and Their - 2019 - IIMB ManagДокумент14 страницVariation and Determinants of Financial Inclusion and Their - 2019 - IIMB ManagWerdhi AriniОценок пока нет

- Micro-Finance in The India: The Changing Face of Micro-Credit SchemesДокумент11 страницMicro-Finance in The India: The Changing Face of Micro-Credit SchemesMahesh ChavanОценок пока нет

- Finacial Inclusion and ExclusionДокумент20 страницFinacial Inclusion and Exclusionbeena antuОценок пока нет

- "Microfinance in India An Indepth Study": Project Proposal TitledДокумент7 страниц"Microfinance in India An Indepth Study": Project Proposal TitledAnkush AgrawalОценок пока нет

- Financial Inclusion in India-An Overview: R. Kedaranatha SwamyДокумент6 страницFinancial Inclusion in India-An Overview: R. Kedaranatha SwamyTJPRC PublicationsОценок пока нет

- Financial Inclusion. 1Документ8 страницFinancial Inclusion. 1sbbhujbalОценок пока нет

- Concept of Financial InclusionДокумент12 страницConcept of Financial InclusionMohitAhujaОценок пока нет

- 4 Chapter-1Документ11 страниц4 Chapter-1Saransh MathurОценок пока нет

- Role of Microfinance in Financial Inclusion in Bihar-A Case StudyДокумент10 страницRole of Microfinance in Financial Inclusion in Bihar-A Case Studyfida mohammadОценок пока нет

- Fic Cir 14102011Документ12 страницFic Cir 14102011bindulijuОценок пока нет

- SH As TriДокумент5 страницSH As TriRaqueem KhanОценок пока нет

- In-Company Training Report ON "Financial Inclusion" Completed in "Financial Inclusion Network and Operation's LTD"Документ35 страницIn-Company Training Report ON "Financial Inclusion" Completed in "Financial Inclusion Network and Operation's LTD"Ashutosh TanejaОценок пока нет

- The Great Globalisation DebateДокумент7 страницThe Great Globalisation DebateVidhi BansalОценок пока нет

- Ashton Smith: Digital Experience DesignerДокумент10 страницAshton Smith: Digital Experience DesignerVidhi BansalОценок пока нет

- Forms of Social Life, InteractionДокумент27 страницForms of Social Life, InteractionVidhi BansalОценок пока нет

- Social Networks: Abhimanyu Dhamija Abhishek Kumar Munish Minia Priyank SharmaДокумент22 страницыSocial Networks: Abhimanyu Dhamija Abhishek Kumar Munish Minia Priyank SharmaDeep AroraОценок пока нет

- A Journey Through The Human HeartДокумент14 страницA Journey Through The Human HeartVidhi BansalОценок пока нет

- Changing Landscape of Finance in India During Last Decade: Finance and The EconomyДокумент9 страницChanging Landscape of Finance in India During Last Decade: Finance and The EconomyVidhi BansalОценок пока нет

- % Program Loadflow - NR % This Is The Newton-Raphson Power Flow ProgramДокумент4 страницы% Program Loadflow - NR % This Is The Newton-Raphson Power Flow ProgramVidhi BansalОценок пока нет

- % Program Loadflow - Gs % This Is A Gauss-Seidel Power Flow ProgramДокумент5 страниц% Program Loadflow - Gs % This Is A Gauss-Seidel Power Flow ProgramVidhi BansalОценок пока нет

- Business Contacts OctoberДокумент15 страницBusiness Contacts OctoberDurban Chamber of Commerce and IndustryОценок пока нет

- Project by Vidhi Seth and Nandini KediaДокумент19 страницProject by Vidhi Seth and Nandini KediavidhisethОценок пока нет

- Forensic Accounting Cheat SheetДокумент2 страницыForensic Accounting Cheat SheetLong SuccessОценок пока нет

- Kuwait - Mohamed IqbalДокумент18 страницKuwait - Mohamed IqbalAsian Development Bank50% (2)

- Insurance Broking BusinessДокумент56 страницInsurance Broking Businesshardikpawar100% (4)

- Mortgages 2019Документ60 страницMortgages 2019Ivana JayОценок пока нет

- How To Read Your MT4 Trading StatementДокумент7 страницHow To Read Your MT4 Trading StatementwanfaroukОценок пока нет

- Aus Tin 20105575Документ120 страницAus Tin 20105575beawinkОценок пока нет

- What Is Credit AppraisalДокумент8 страницWhat Is Credit AppraisalAshwin Sajan VargheseОценок пока нет

- Introduction of Financial InstitutionДокумент12 страницIntroduction of Financial InstitutionGanesh Kumar100% (2)

- Tcs Project ReportДокумент52 страницыTcs Project Reportfaheem munim0% (2)

- Power of AttorneyДокумент5 страницPower of AttorneyAshokОценок пока нет

- Bank ReconДокумент5 страницBank ReconHannah Jane Umbay67% (3)

- Detailed Lesson Plan in ABMДокумент5 страницDetailed Lesson Plan in ABMAnonymous QZsOxQsJОценок пока нет

- AICPA - Develops Standards For Audits ofДокумент3 страницыAICPA - Develops Standards For Audits ofAngela PaduaОценок пока нет

- Credit Annual STMTДокумент8 страницCredit Annual STMTallinoneetmtОценок пока нет

- Bank Reconciliation StatementДокумент40 страницBank Reconciliation StatementPrashant100% (1)

- Ixambee Monthly December CapsuleДокумент48 страницIxambee Monthly December CapsulejoydsОценок пока нет

- STARTRADE RO - Comisioane Si Taxe STARTRADE RO - Fees and CommissionsДокумент3 страницыSTARTRADE RO - Comisioane Si Taxe STARTRADE RO - Fees and CommissionsAzi NuОценок пока нет

- TciДокумент53 страницыTciarunzmr007Оценок пока нет

- Dresdner Struct Products Vicious CircleДокумент8 страницDresdner Struct Products Vicious CircleBoris MangalОценок пока нет

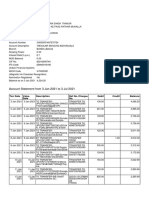

- Account Statement From 3 Jan 2021 To 3 Jul 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceДокумент8 страницAccount Statement From 3 Jan 2021 To 3 Jul 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceSanatan ThakurОценок пока нет

- CorrespondenceДокумент5 страницCorrespondenceUsakikamiОценок пока нет

- Procedure For Private Placement and AllotmentДокумент2 страницыProcedure For Private Placement and AllotmentNithya GaneshОценок пока нет

- Family Roster As of 8.31.22Документ12 страницFamily Roster As of 8.31.22San Simon PantawidОценок пока нет

- PAT Agency Digest3Документ6 страницPAT Agency Digest3bcarОценок пока нет

- Audit For Purchase CycleДокумент2 страницыAudit For Purchase CycleSarlamSaleh100% (1)

- Demat Acount TradebullsДокумент23 страницыDemat Acount TradebullsMihir SenОценок пока нет

- Industry Profile: Banking Sector in IndiaДокумент15 страницIndustry Profile: Banking Sector in Indiasri1031Оценок пока нет

- Customers' Perceptions Towards E-Banking Services - A Study of Select Public Sector Banks in Rayalaseema Region of Andhra PradeshДокумент11 страницCustomers' Perceptions Towards E-Banking Services - A Study of Select Public Sector Banks in Rayalaseema Region of Andhra Pradesharcherselevators100% (1)