Вам также может понравиться

- Market Outlook Report 18 March 2013Документ4 страницыMarket Outlook Report 18 March 2013zenergynzОценок пока нет

- Market Outlook Report 15 October 2012Документ4 страницыMarket Outlook Report 15 October 2012zenergynzОценок пока нет

- Market Outlook Report 20 August 2012Документ4 страницыMarket Outlook Report 20 August 2012zenergynzОценок пока нет

- Market Outlook Report 23 July 2012Документ4 страницыMarket Outlook Report 23 July 2012zenergynzОценок пока нет

- Market Outlook Report 17 September 2012Документ4 страницыMarket Outlook Report 17 September 2012zenergynzОценок пока нет

- Market Outlook Report 10 December 2012Документ4 страницыMarket Outlook Report 10 December 2012zenergynzОценок пока нет

- Market Outlook Report 12 November 2012Документ4 страницыMarket Outlook Report 12 November 2012zenergynzОценок пока нет

- Market Outlook Report 26 November 2012Документ4 страницыMarket Outlook Report 26 November 2012zenergynzОценок пока нет

- Energy Information Administration Latest Release: SourceДокумент6 страницEnergy Information Administration Latest Release: SourceSunil DarakОценок пока нет

- Sprott On Oil and Gold Where Do We Go From HereДокумент12 страницSprott On Oil and Gold Where Do We Go From HereCanadianValueОценок пока нет

- Weekly Investment Notes - 2015.10.09Документ20 страницWeekly Investment Notes - 2015.10.09jeet1970Оценок пока нет

- International Active Update: Fourth Quarter 2014Документ7 страницInternational Active Update: Fourth Quarter 2014CanadianValueОценок пока нет

- Weekly Market Commentary 3-5-2012Документ3 страницыWeekly Market Commentary 3-5-2012monarchadvisorygroupОценок пока нет

- Macroeconomic Factors Affecting USD INRДокумент16 страницMacroeconomic Factors Affecting USD INRtamanna210% (1)

- Daily CommentaryДокумент5 страницDaily Commentarysilviu_catrinaОценок пока нет

- MPC Statement November 20 FinalДокумент11 страницMPC Statement November 20 FinalMatthewLeCordeurОценок пока нет

- The Future of Commodity Markets in IndiaДокумент11 страницThe Future of Commodity Markets in Indiakumar vivekОценок пока нет

- Weekly Commodity Review - 7 - 11 May 2012Документ1 страницаWeekly Commodity Review - 7 - 11 May 2012gordjuОценок пока нет

- Beta Times Markets Edition11Документ4 страницыBeta Times Markets Edition11VALLIAPPAN.PОценок пока нет

- Viewpoint From Palladiem - January 2015: ValuationДокумент1 страницаViewpoint From Palladiem - January 2015: Valuationapi-275925231Оценок пока нет

- Q3 - 2015 Commentary: 5.1% and 10.3%, RespectivelyДокумент5 страницQ3 - 2015 Commentary: 5.1% and 10.3%, RespectivelyJohn MathiasОценок пока нет

- CommodityMonitor Monthly Aug2014Документ11 страницCommodityMonitor Monthly Aug2014krishnaОценок пока нет

- Chaanakya 5 - 10Документ22 страницыChaanakya 5 - 10Apoorv JhudeleyОценок пока нет

- Nedbank Se Rentekoers-Barometer November 2016Документ4 страницыNedbank Se Rentekoers-Barometer November 2016Netwerk24SakeОценок пока нет

- LINC Week 7Документ10 страницLINC Week 7TomasОценок пока нет

- RIG April 2013Документ40 страницRIG April 2013cuntingyouОценок пока нет

- Wisco Team: First QuarterДокумент4 страницыWisco Team: First QuarterGreg SchroederОценок пока нет

- Weekly Views From The Metro: HighlightsДокумент3 страницыWeekly Views From The Metro: HighlightsRobert RamirezОценок пока нет

- NAB Forecast (12 July 2011) : World Slows From Tsunami Disruptions and Tighter Policy.Документ18 страницNAB Forecast (12 July 2011) : World Slows From Tsunami Disruptions and Tighter Policy.International Business Times AUОценок пока нет

- Hadrian BriefДокумент11 страницHadrian Briefspace238Оценок пока нет

- Week 51: This Week's HeadlinesДокумент9 страницWeek 51: This Week's HeadlinesLINCОценок пока нет

- GX CB Global Power of Luxury WebДокумент52 страницыGX CB Global Power of Luxury WebFahad Al MuttairiОценок пока нет

- Commodities Letter December 2014Документ5 страницCommodities Letter December 2014Swedbank AB (publ)Оценок пока нет

- Buzz (Metal) Oct28 11Документ3 страницыBuzz (Metal) Oct28 11Mishra Anand PrakashОценок пока нет

- Weekly CommentaryДокумент4 страницыWeekly Commentaryapi-150779697Оценок пока нет

- Fundamentals Dec 2014Документ40 страницFundamentals Dec 2014Yew Toh TatОценок пока нет

- 2015.10 Q3 CMC Efficient Frontier NewsletterДокумент8 страниц2015.10 Q3 CMC Efficient Frontier NewsletterJohn MathiasОценок пока нет

- Speak of The Week Aug 10-2012Документ3 страницыSpeak of The Week Aug 10-2012Bonthala BadrОценок пока нет

- BlackRock 2014 OutlookДокумент8 страницBlackRock 2014 OutlookMartinec TomášОценок пока нет

- FICC Times 22 Mar 2013Документ6 страницFICC Times 22 Mar 2013r_squareОценок пока нет

- Weekly Sentiment Paper: Distributed By: One Financial Written By: Andrei WogenДокумент14 страницWeekly Sentiment Paper: Distributed By: One Financial Written By: Andrei WogenAndrei Alexander WogenОценок пока нет

- Urrency Forecast: $ Continued To Weaken Vs Other Major CurrenciesДокумент4 страницыUrrency Forecast: $ Continued To Weaken Vs Other Major CurrenciesprinceasatiОценок пока нет

- Weekly OverviewДокумент4 страницыWeekly Overviewapi-150779697Оценок пока нет

- Winter 2016Документ3 страницыWinter 2016Amin KhakianiОценок пока нет

- Energy Sector Outlook: What We Are Watching: MarketДокумент5 страницEnergy Sector Outlook: What We Are Watching: MarketdpbasicОценок пока нет

- PHP HRty 8 RДокумент5 страницPHP HRty 8 Rfred607Оценок пока нет

- OPEC - Monthly Oil Market ReportДокумент75 страницOPEC - Monthly Oil Market Reportrryan123123Оценок пока нет

- MOMR January 2015Документ100 страницMOMR January 2015Raza SamiОценок пока нет

- Forex Round Up 06.12.09Документ11 страницForex Round Up 06.12.09Neha DhuriОценок пока нет

- RBI Monetary Policy - 03-02-2015Документ8 страницRBI Monetary Policy - 03-02-2015Pritam ChangkakotiОценок пока нет

- Ranges (Up Till 11.30am HKT) : Currency CurrencyДокумент3 страницыRanges (Up Till 11.30am HKT) : Currency Currencyapi-290371470Оценок пока нет

- Is The Tide Rising?: Figure 1. World Trade Volumes, Industrial Production and Manufacturing PMIДокумент3 страницыIs The Tide Rising?: Figure 1. World Trade Volumes, Industrial Production and Manufacturing PMIjdsolorОценок пока нет

- Slide in Oil PricesДокумент7 страницSlide in Oil PricesRituparna SamantarayОценок пока нет

- Minutes January 2008Документ10 страницMinutes January 2008alina.w.siddiquiОценок пока нет

- Crude OilДокумент12 страницCrude OilRanjithОценок пока нет

- The Commodity Investor S 102885050Документ33 страницыThe Commodity Investor S 102885050Parin Chawda100% (1)

- Oil Market Outlook 022013Документ9 страницOil Market Outlook 022013Venkatakrishnan IyerОценок пока нет

- Commodities Overview: Consolidating With China's HelpДокумент22 страницыCommodities Overview: Consolidating With China's HelpAlberto DelsoОценок пока нет

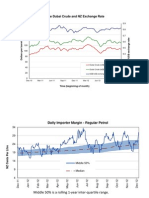

- Weekly Average Dubai Crude and NZ Exchange Rate: Time (Beginning of Month)Документ8 страницWeekly Average Dubai Crude and NZ Exchange Rate: Time (Beginning of Month)zenergynzОценок пока нет

- Market Outlook Report 10 December 2012Документ4 страницыMarket Outlook Report 10 December 2012zenergynzОценок пока нет

- Market Outlook Report 26 November 2012Документ4 страницыMarket Outlook Report 26 November 2012zenergynzОценок пока нет

- Market Outlook Report 12 November 2012Документ4 страницыMarket Outlook Report 12 November 2012zenergynzОценок пока нет

- The Energy Drop - May 12Документ4 страницыThe Energy Drop - May 12zenergynzОценок пока нет

- Regal Haulage Help Us Trial Our New Truck Stop Cardreaders: Z.co - NZДокумент4 страницыRegal Haulage Help Us Trial Our New Truck Stop Cardreaders: Z.co - NZzenergynzОценок пока нет

- The Energy Drop - July 12Документ4 страницыThe Energy Drop - July 12zenergynzОценок пока нет

- The Energy Drop - June 12Документ4 страницыThe Energy Drop - June 12zenergynzОценок пока нет

- The Energy Drop - April 12Документ4 страницыThe Energy Drop - April 12zenergynzОценок пока нет

- The Energy Drop - February 12Документ4 страницыThe Energy Drop - February 12zenergynzОценок пока нет

- The Energy Drop - January 12Документ4 страницыThe Energy Drop - January 12zenergynzОценок пока нет

- Oil Price Monitoring Graphs (MED)Документ8 страницOil Price Monitoring Graphs (MED)zenergynzОценок пока нет

- Cigarettes and AlcoholДокумент1 страницаCigarettes and AlcoholHye Jin KimОценок пока нет

- Versana Premier Transducer GuideДокумент4 страницыVersana Premier Transducer GuideDigo OtávioОценок пока нет

- Institute of Metallurgy and Materials Engineering Faculty of Chemical and Materials Engineering University of The Punjab LahoreДокумент10 страницInstitute of Metallurgy and Materials Engineering Faculty of Chemical and Materials Engineering University of The Punjab LahoreMUmairQrОценок пока нет

- 2nd Quarter - Summative Test in TleДокумент2 страницы2nd Quarter - Summative Test in TleRachelle Ann Dizon100% (1)

- Alzheimer's Disease Inhalational Alzheimer's Disease An UnrecognizedДокумент10 страницAlzheimer's Disease Inhalational Alzheimer's Disease An UnrecognizednikoknezОценок пока нет

- Https - Threejs - Org - Examples - Webgl - Fire - HTMLДокумент9 страницHttps - Threejs - Org - Examples - Webgl - Fire - HTMLMara NdirОценок пока нет

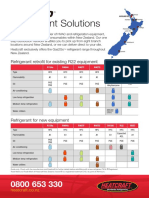

- Refrigerant Solutions: Refrigerant Retrofit For Existing R22 EquipmentДокумент2 страницыRefrigerant Solutions: Refrigerant Retrofit For Existing R22 EquipmentpriyoОценок пока нет

- Xu 2020Документ11 страницXu 2020Marco A. R. JimenesОценок пока нет

- Greyhound Free Patt.Документ14 страницGreyhound Free Patt.claire_garlandОценок пока нет

- Maharashtra Brochure (2023)Документ4 страницыMaharashtra Brochure (2023)assmexellenceОценок пока нет

- Surface & Subsurface Geotechnical InvestigationДокумент5 страницSurface & Subsurface Geotechnical InvestigationAshok Kumar SahaОценок пока нет

- Catalyst Worksheet - SHHSДокумент3 страницыCatalyst Worksheet - SHHSNerd 101Оценок пока нет

- Edrolo ch3Документ42 страницыEdrolo ch3YvonneОценок пока нет

- Moving Money Box: Pig (Assembly Instructions) : The Movements Work Better With Heavier CoinsДокумент6 страницMoving Money Box: Pig (Assembly Instructions) : The Movements Work Better With Heavier CoinsjuanОценок пока нет

- Welrod Silenced PistolДокумент2 страницыWelrod Silenced Pistolblowmeasshole1911Оценок пока нет

- NHouse SelfBuilder Brochure v2 Jan19 LowresДокумент56 страницNHouse SelfBuilder Brochure v2 Jan19 LowresAndrew Richard ThompsonОценок пока нет

- 240-Article Text-799-3-10-20190203Документ6 страниц240-Article Text-799-3-10-20190203EVANDRO FRANCO DA ROCHAОценок пока нет

- Servo Controlled FBW With Power Boost Control, Operations & Maint. ManualДокумент126 страницServo Controlled FBW With Power Boost Control, Operations & Maint. ManualKota NatarajanОценок пока нет

- HandbikeДокумент10 страницHandbikeLely JuniariОценок пока нет

- Computer From ScratchДокумент6 страницComputer From ScratchPaul NavedaОценок пока нет

- Photography Techniques (Intermediate)Документ43 страницыPhotography Techniques (Intermediate)Truc Nguyen100% (2)

- Chapter 1 Cumulative Review: Multiple ChoiceДокумент2 страницыChapter 1 Cumulative Review: Multiple ChoiceJ. LeeОценок пока нет

- 2011 33 MaintenanceДокумент16 страниц2011 33 MaintenanceKrishna Khandige100% (1)

- Unit-I: Digital Image Fundamentals & Image TransformsДокумент70 страницUnit-I: Digital Image Fundamentals & Image TransformsNuzhath FathimaОценок пока нет

- School: Grade Level: Teacher: Section Teaching Dates and Time: QuarterДокумент3 страницыSchool: Grade Level: Teacher: Section Teaching Dates and Time: QuarterZeny Aquino DomingoОценок пока нет

- Bio-Rad D-10 Dual ProgramДокумент15 страницBio-Rad D-10 Dual ProgramMeesam AliОценок пока нет

- Identifying - Explaining Brake System FunctionsДокумент39 страницIdentifying - Explaining Brake System FunctionsJestoni100% (1)

- Philips Family Lamp UV CДокумент4 страницыPhilips Family Lamp UV CmaterpcОценок пока нет

- Ddrive Transmission ReportДокумент43 страницыDdrive Transmission Reportelah150% (2)

- Static CMOS and Dynamic CircuitsДокумент19 страницStatic CMOS and Dynamic CircuitsAbhijna MaiyaОценок пока нет