Вам также может понравиться

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (894)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (119)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2219)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- Bobatrader: Guide To Consistent Daytrading: Wsodownloads - inДокумент33 страницыBobatrader: Guide To Consistent Daytrading: Wsodownloads - inram ramОценок пока нет

- General Training Writing Sample Task - Task 1Документ1 страницаGeneral Training Writing Sample Task - Task 1Phương MiОценок пока нет

- WBS StructureДокумент17 страницWBS StructureWickedadonis0% (1)

- Securities Trade Life CycleДокумент28 страницSecurities Trade Life CycleUmesh Bansode100% (4)

- BPO OperationsДокумент2 страницыBPO OperationsWickedadonisОценок пока нет

- SubPrime 1Документ45 страницSubPrime 1WickedadonisОценок пока нет

- BPO OperationsДокумент2 страницыBPO OperationsWickedadonisОценок пока нет

- SubPrime 1Документ45 страницSubPrime 1WickedadonisОценок пока нет

- Offshore Outsourcing Chapter OneДокумент15 страницOffshore Outsourcing Chapter OneWickedadonisОценок пока нет

- Economic StrategyДокумент84 страницыEconomic StrategyWickedadonisОценок пока нет

- Accounting GlossaryДокумент30 страницAccounting GlossaryGYANA RANJAN NAYAK100% (1)

- OPS2014Документ16 страницOPS2014WickedadonisОценок пока нет

- Fixed Income Made Simple - 30apr12 - FINAL (PRINT VERSIon)Документ36 страницFixed Income Made Simple - 30apr12 - FINAL (PRINT VERSIon)WickedadonisОценок пока нет

- KPOДокумент5 страницKPOWickedadonisОценок пока нет

- BPO OperationsДокумент2 страницыBPO OperationsWickedadonisОценок пока нет

- Aerohive Whitepaper Public or Private CloudДокумент8 страницAerohive Whitepaper Public or Private CloudAnuj AggarwalОценок пока нет

- G Shock Ga100a 7a Manual - UnlockedДокумент4 страницыG Shock Ga100a 7a Manual - UnlockedSuneo DeltaОценок пока нет

- IT Engagement ModelsДокумент16 страницIT Engagement ModelsWickedadonis100% (1)

- Andaz Apna Apna Teaches 15 Important Life LessonsДокумент16 страницAndaz Apna Apna Teaches 15 Important Life LessonsWickedadonisОценок пока нет

- Off ShoringДокумент5 страницOff ShoringWickedadonisОценок пока нет

- OutsourcingДокумент5 страницOutsourcingWickedadonisОценок пока нет

- BPO OperationsДокумент2 страницыBPO OperationsWickedadonisОценок пока нет

- Ops KPOДокумент5 страницOps KPOWickedadonisОценок пока нет

- How Dealers Conduct Foreign Exchange Operations: All About..Документ10 страницHow Dealers Conduct Foreign Exchange Operations: All About..WickedadonisОценок пока нет

- KPOДокумент5 страницKPOWickedadonisОценок пока нет

- BPO OperationsДокумент2 страницыBPO OperationsWickedadonisОценок пока нет

- The Story of Monetary PolicyДокумент24 страницыThe Story of Monetary Policy김남수Оценок пока нет

- BPO OpsДокумент4 страницыBPO OpsWickedadonisОценок пока нет

- Fed Reserve OMOs ExplainedДокумент4 страницыFed Reserve OMOs ExplainedWickedadonisОценок пока нет

- ChinaДокумент14 страницChinatong kok hooiОценок пока нет

- Money Supply - IndiaДокумент20 страницMoney Supply - IndiaShrey SampatОценок пока нет

- 1950Документ7 страниц1950Shital WaghmareОценок пока нет

- Patel Engineering AGM NoticeДокумент165 страницPatel Engineering AGM NoticeArunesh SinghОценок пока нет

- Morgart Presentation - Alternatives Harvard Bus School Pres FinalДокумент11 страницMorgart Presentation - Alternatives Harvard Bus School Pres FinalWilliam RichmondОценок пока нет

- Overview of Advanced Derivatives MarketsДокумент19 страницOverview of Advanced Derivatives MarketsAllene Leyba Sayas-TanОценок пока нет

- Binder 8Документ238 страницBinder 8Jose Garcia de la Torre100% (1)

- ABM - BF12 IIIb 8Документ4 страницыABM - BF12 IIIb 8Raffy Jade SalazarОценок пока нет

- 1 Financial MarketДокумент35 страниц1 Financial MarketSachinGoelОценок пока нет

- Account Transfer Form: Fax Cover SheetДокумент6 страницAccount Transfer Form: Fax Cover SheetJitendra SharmaОценок пока нет

- Chapter 7 Importance of Money and Capital MarketsДокумент9 страницChapter 7 Importance of Money and Capital MarketsSyrill CayetanoОценок пока нет

- Buyback and Delisting of SharesДокумент42 страницыBuyback and Delisting of SharesSahil SinglaОценок пока нет

- MAF653 TEST 1 NOV 2022 QuestionДокумент11 страницMAF653 TEST 1 NOV 2022 QuestionAyunieazahaОценок пока нет

- Astro EbooksДокумент4 страницыAstro Ebooksebook feeОценок пока нет

- Dan Zanger Trading Rules PDFДокумент4 страницыDan Zanger Trading Rules PDFljhreОценок пока нет

- Adani EnterprisesДокумент1 страницаAdani EnterprisesDebjit SenguptaОценок пока нет

- Capital Investment DecisionsДокумент20 страницCapital Investment Decisionsmubasheralijamro0% (1)

- Phase Test 2017 - 18Документ15 страницPhase Test 2017 - 18AKSHIT SHUKLAОценок пока нет

- Mid Term Exam MCQs For 5530Документ6 страницMid Term Exam MCQs For 5530Amy WangОценок пока нет

- INDIABULLS CoppanyДокумент101 страницаINDIABULLS CoppanyJasmandeep brarОценок пока нет

- 19-Article Text-27-1-10-20210124Документ14 страниц19-Article Text-27-1-10-20210124CindaОценок пока нет

- Corporate FinanceДокумент142 страницыCorporate FinancetagashiiОценок пока нет

- Financial Markets Meaning, Types and WorkingДокумент15 страницFinancial Markets Meaning, Types and WorkingRainman577100% (1)

- Regulatory On Derivatives (1) (From Shodhganga)Документ70 страницRegulatory On Derivatives (1) (From Shodhganga)sharathОценок пока нет

- Benefits of Adverse PossessionДокумент3 страницыBenefits of Adverse PossessionBob Hurt100% (3)

- Cbse Class 12 Sample Paper 2018 19 EntrepreneurshipДокумент6 страницCbse Class 12 Sample Paper 2018 19 Entrepreneurshipprasoon jhaОценок пока нет

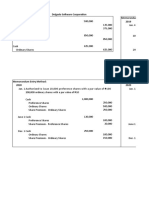

- Memorandum and Journal Entry Methods for Share Capital TransactionsДокумент3 страницыMemorandum and Journal Entry Methods for Share Capital TransactionsFeiya Liu100% (1)

- Comparing SBI Magnum and IDFC Mutual Fund RatiosДокумент4 страницыComparing SBI Magnum and IDFC Mutual Fund RatiosJenifer Chrisla TОценок пока нет

- Turpin BankruptcyДокумент83 страницыTurpin Bankruptcytom cleary100% (1)