Вам также может понравиться

- 1 Introduction To Financial AccountingДокумент66 страниц1 Introduction To Financial Accountingpeikee100% (1)

- 26.2.15 I Can Solve Problems Using Addition and A Number LineДокумент2 страницы26.2.15 I Can Solve Problems Using Addition and A Number LinepeikeeОценок пока нет

- Exercise 5 (Chap 5)Документ4 страницыExercise 5 (Chap 5)peikeeОценок пока нет

- IAS 17 - Tutorial QsДокумент2 страницыIAS 17 - Tutorial Qspeikee0% (1)

- STA222 Exercise 2 Probability QuestionsДокумент4 страницыSTA222 Exercise 2 Probability QuestionspeikeeОценок пока нет

- Exercise 4 (Chap 4)Документ12 страницExercise 4 (Chap 4)peikee100% (1)

- Exercise 3 (Chap 3)Документ2 страницыExercise 3 (Chap 3)peikeeОценок пока нет

- Exercise 1 (Chap 1)Документ8 страницExercise 1 (Chap 1)peikee0% (1)

- Foundations of Management Accounting ACC 223Документ9 страницFoundations of Management Accounting ACC 223peikeeОценок пока нет

- ACC304Документ2 страницыACC304peikeeОценок пока нет

- Fin328 - Ias17 Lease (Z)Документ9 страницFin328 - Ias17 Lease (Z)peikeeОценок пока нет

- Questions - BudgetingДокумент3 страницыQuestions - BudgetingpeikeeОценок пока нет

- ACC304 ACC324 StdCosting Topic 6Документ5 страницACC304 ACC324 StdCosting Topic 6peikeeОценок пока нет

- IAS 37 - Tutorial Qs - Part 2Документ2 страницыIAS 37 - Tutorial Qs - Part 2peikeeОценок пока нет

- Paragraph WritingДокумент2 страницыParagraph WritingpeikeeОценок пока нет

- Case Study FormatДокумент1 страницаCase Study FormatpeikeeОценок пока нет

- 9 Fixed Assets AccountingДокумент18 страниц9 Fixed Assets AccountingpeikeeОценок пока нет

- 2 Fundamental Accounting Concepts and PrinciplesДокумент35 страниц2 Fundamental Accounting Concepts and Principlespeikee100% (1)

- The Illustrative Essay: Exposing The ExamplesДокумент12 страницThe Illustrative Essay: Exposing The ExamplespeikeeОценок пока нет

- Oral Presentaion SkillsДокумент20 страницOral Presentaion SkillsDr. Wael El-Said100% (2)

- Complete Eco 204Документ17 страницComplete Eco 204peikeeОценок пока нет

- Examination Terminology Terms Used ExplanationДокумент1 страницаExamination Terminology Terms Used ExplanationpeikeeОценок пока нет

- 11 Financial Accounting For Sole TraderДокумент6 страниц11 Financial Accounting For Sole TraderpeikeeОценок пока нет

- VT ReviewДокумент44 страницыVT ReviewbeodethuongОценок пока нет

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5784)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (890)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (265)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (119)

- Idwest ICE Cream Company: A Case StudyДокумент10 страницIdwest ICE Cream Company: A Case StudyDixie Diana Viquiera FernandezОценок пока нет

- Taxes Are Obsolete by Beardsley Ruml, Former FED ChairmanДокумент5 страницTaxes Are Obsolete by Beardsley Ruml, Former FED ChairmanPatrick O'SheaОценок пока нет

- VN instant food industry overviewДокумент17 страницVN instant food industry overviewQuoc Minh TaiОценок пока нет

- 04-Calling The Tune in The Gold MarketДокумент4 страницы04-Calling The Tune in The Gold MarketlowtarhkОценок пока нет

- Benchmarking Project ManagementДокумент13 страницBenchmarking Project ManagementpparkerОценок пока нет

- Business Proposal For Setting Up of A Jacket 2003Документ37 страницBusiness Proposal For Setting Up of A Jacket 2003Abhinav Akash SinghОценок пока нет

- TaxationДокумент33 страницыTaxationlordaiztrand100% (1)

- CHP 12 - Strategy, Balanced Scorecard, and Strategic Profitability (With Answers)Документ54 страницыCHP 12 - Strategy, Balanced Scorecard, and Strategic Profitability (With Answers)kenchong7150% (1)

- Nike, Inc. Strategic Analysis 2009: Jarryd Phillips, Jermaine West, Spencer Jacoby, Othniel Hyliger, Steven PelletierДокумент42 страницыNike, Inc. Strategic Analysis 2009: Jarryd Phillips, Jermaine West, Spencer Jacoby, Othniel Hyliger, Steven PelletierAnmol Jain100% (1)

- Sandpaper Project ProfileДокумент15 страницSandpaper Project ProfileTekeba Birhane100% (3)

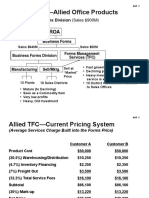

- ABC Costing Allied Office ProductsДокумент13 страницABC Costing Allied Office ProductsProfessorAsim Kumar Mishra100% (1)

- Readsoft Ir Presentation Year End 2013Документ21 страницаReadsoft Ir Presentation Year End 2013RockiОценок пока нет

- Chopra Scm5 Tif Ch13Документ23 страницыChopra Scm5 Tif Ch13Madyoka RaimbekОценок пока нет

- Report PDFДокумент19 страницReport PDFmaria saleem100% (1)

- Customer Value Management Concepts and Case Study: Sunil Thawani Adnoc DistributionДокумент38 страницCustomer Value Management Concepts and Case Study: Sunil Thawani Adnoc Distributionjitendrasutar1975Оценок пока нет

- 2011 Tutorial Letter 101Документ48 страниц2011 Tutorial Letter 101Heather SkorpenОценок пока нет

- All Project 3Документ108 страницAll Project 3Raju Sureliya100% (1)

- Sample Assignment On Marketing Planning of An OrganizationДокумент27 страницSample Assignment On Marketing Planning of An OrganizationInstant Assignment HelpОценок пока нет

- Internship ReportДокумент62 страницыInternship ReportShariful IslamОценок пока нет

- Syllabus of Shivaji University MBAДокумент24 страницыSyllabus of Shivaji University MBAmaheshlakade755Оценок пока нет

- United Grain Growers Limited (A) : Syndicate 5 (Ape Syndicate) Syndicate 5 (Ape Syndicate)Документ34 страницыUnited Grain Growers Limited (A) : Syndicate 5 (Ape Syndicate) Syndicate 5 (Ape Syndicate)Iqbal MohammadОценок пока нет

- FINANCE MANAGEMENT FIN420chp 1Документ10 страницFINANCE MANAGEMENT FIN420chp 1Yanty IbrahimОценок пока нет

- Cost of QualityДокумент65 страницCost of Qualityajayvmehta100% (6)

- Tank Irrigation Management SystemДокумент18 страницTank Irrigation Management SystemSanjeeva YedavalliОценок пока нет

- Financial Statement Analysis of Nandan Denim LtdДокумент70 страницFinancial Statement Analysis of Nandan Denim LtdsejalОценок пока нет

- Texana Petroleum Corporation HistoryДокумент9 страницTexana Petroleum Corporation HistoryDhyana Mohanty100% (1)

- Pitchbook on Jubilant FoodworksДокумент28 страницPitchbook on Jubilant FoodworksAtulSinghОценок пока нет

- Sample CEO ResumeДокумент3 страницыSample CEO ResumejstillwaОценок пока нет

- Customer and Product Profitability at BanksДокумент15 страницCustomer and Product Profitability at Banksmuhaayan87100% (1)

- Three Zone of Production FunctionДокумент5 страницThree Zone of Production FunctionNamdev Upadhyay71% (7)