Вам также может понравиться

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5795)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (345)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1091)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- Sta A4187876 21425Документ2 страницыSta A4187876 21425doud98Оценок пока нет

- 12.6% P.A. Quarterly Conditional Coupon With Memory Effect - European Barrier at 60% - 1 Year and 3 Months - EURДокумент1 страница12.6% P.A. Quarterly Conditional Coupon With Memory Effect - European Barrier at 60% - 1 Year and 3 Months - EURapi-25889552Оценок пока нет

- ReviewerДокумент7 страницReviewerDiego RallaОценок пока нет

- Financing Africa Through The Crisis and Beyond PDFДокумент322 страницыFinancing Africa Through The Crisis and Beyond PDFEmeka NkemОценок пока нет

- Lessons From 1 000 Corporate Defaults 2011-11-30Документ7 страницLessons From 1 000 Corporate Defaults 2011-11-30louislu87Оценок пока нет

- Report On Non Performing Assets of BankДокумент53 страницыReport On Non Performing Assets of Bankhemali chovatiya75% (4)

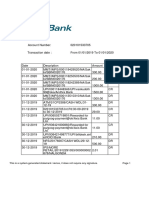

- This Is A System-Generated Statement. Hence, It Does Not Require Any SignatureДокумент16 страницThis Is A System-Generated Statement. Hence, It Does Not Require Any SignatureVinod DharavathОценок пока нет

- Laura M. Marnelego Vs Bangko Filipino Savings and Mortgage BankДокумент8 страницLaura M. Marnelego Vs Bangko Filipino Savings and Mortgage BankKay AvilesОценок пока нет

- Achukatla Baba FakruddinДокумент6 страницAchukatla Baba Fakruddinferoz acОценок пока нет

- Rrb-Vii Po Final Result-295 MarksДокумент6 страницRrb-Vii Po Final Result-295 MarksgyhgОценок пока нет

- Final Report: Internal Audit On Purchasing and Payments ATДокумент18 страницFinal Report: Internal Audit On Purchasing and Payments ATwiseguy4uОценок пока нет

- What Is Construction Cost in Pune - What Is Builders Profit Margin in Pune - Pune Property ManagementДокумент4 страницыWhat Is Construction Cost in Pune - What Is Builders Profit Margin in Pune - Pune Property ManagementamolkajalednyaОценок пока нет

- Videocon Annual Report CY 2015Документ124 страницыVideocon Annual Report CY 2015Chandrashekhar DigraskarОценок пока нет

- Idbi - Annexure IiiДокумент1 страницаIdbi - Annexure IiiVikash AgarwalОценок пока нет

- February 2020Документ35 страницFebruary 2020Ramesh Ku ArОценок пока нет

- Barings BankДокумент2 страницыBarings Bankaman_kshОценок пока нет

- Pilgrim Bank - AДокумент7 страницPilgrim Bank - ASaurabhОценок пока нет

- FM - Madhyasth Bank Amreli - 3Документ74 страницыFM - Madhyasth Bank Amreli - 3jagrutisolanki01Оценок пока нет

- Omkar Bro ProjectДокумент50 страницOmkar Bro ProjectG B Preethi100% (1)

- Assignment (ERD) : Cairo University Faculty of Computers and Information Information Systems Department Database Systems 1Документ4 страницыAssignment (ERD) : Cairo University Faculty of Computers and Information Information Systems Department Database Systems 1Apricot BlueberryОценок пока нет

- The Merger of Bank of Baroda, Vijaya Bank & Dena BankДокумент7 страницThe Merger of Bank of Baroda, Vijaya Bank & Dena BankkrishishettyОценок пока нет

- A STUDY ON Fixed Deposit ofДокумент4 страницыA STUDY ON Fixed Deposit ofMhn Budha KarnОценок пока нет

- Ucpdc 600 - Explanation On Various Articles - Part IДокумент9 страницUcpdc 600 - Explanation On Various Articles - Part IChinnu AnchuriОценок пока нет

- Blackrick Strategic FundsДокумент31 страницаBlackrick Strategic FundssmysonaОценок пока нет

- Difference Pledge MortgageДокумент6 страницDifference Pledge MortgageJeffrey Constantino Patacsil100% (1)

- Draft Pfcea New ProcedureДокумент21 страницаDraft Pfcea New Proceduredirector@bancofinancieroprivado100% (2)

- Choosing The Right Source of FinanceДокумент11 страницChoosing The Right Source of FinancemahezrulezОценок пока нет

- 351711588Документ3 страницы351711588vasu_msa123Оценок пока нет

- E-Commerce: Slide 1-1Документ12 страницE-Commerce: Slide 1-1haleemОценок пока нет

- Revenue Audit ProgrammeДокумент6 страницRevenue Audit ProgrammeDaniela BulardaОценок пока нет