Вам также может понравиться

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- TAX6148-Reviewer (Auto Recovered) TAX6148 - Reviewer (Auto Recovered)Документ31 страницаTAX6148-Reviewer (Auto Recovered) TAX6148 - Reviewer (Auto Recovered)lizelleОценок пока нет

- HDFC Compensation+Structure+ +Executive+TraineeДокумент1 страницаHDFC Compensation+Structure+ +Executive+TraineeOrange NoidaОценок пока нет

- CFPДокумент16 страницCFPOrange Noida100% (1)

- Portfolio Mgt11Документ15 страницPortfolio Mgt11Orange NoidaОценок пока нет

- BS 2 SyllabusДокумент2 страницыBS 2 SyllabusOrange NoidaОценок пока нет

- HDFC Compensation+Structure+ +Executive+TraineeДокумент1 страницаHDFC Compensation+Structure+ +Executive+TraineeOrange NoidaОценок пока нет

- JD ExevoДокумент3 страницыJD ExevoOrange NoidaОценок пока нет

- Mergers and Acquisition - Assignment 1Документ1 страницаMergers and Acquisition - Assignment 1Orange NoidaОценок пока нет

- Amity School of Business: Marketing Management - IIДокумент38 страницAmity School of Business: Marketing Management - IIOrange NoidaОценок пока нет

- 4d2a5tea ModelДокумент6 страниц4d2a5tea ModelOrange NoidaОценок пока нет

- My Project Report On Icici Bank FinalДокумент97 страницMy Project Report On Icici Bank Finalgauravshuklapgdm71% (28)

- Amity School of Business: BBA, Semester 3 Financial Management 1Документ44 страницыAmity School of Business: BBA, Semester 3 Financial Management 1Orange NoidaОценок пока нет

- Hand BookДокумент44 страницыHand BookRahul DurgiaОценок пока нет

- Revised Sch. VIДокумент48 страницRevised Sch. VIOrange Noida100% (1)

- HCL Info Annual Report 2008-09Документ162 страницыHCL Info Annual Report 2008-09Ankit Jain100% (1)

- Unearthingthepowerofibmrationalfunctionaltester7 0 RFT 090729230029 Phpapp02Документ2 страницыUnearthingthepowerofibmrationalfunctionaltester7 0 RFT 090729230029 Phpapp02Orange NoidaОценок пока нет

- 2011Документ136 страниц2011Orange Noida100% (1)

- Trading and Profit Loss AccountДокумент8 страницTrading and Profit Loss AccountOrange Noida100% (1)

- Howtopublishmaemo5applicationstoovistoregeorgekurtyka 091209092743 Phpapp01Документ6 страницHowtopublishmaemo5applicationstoovistoregeorgekurtyka 091209092743 Phpapp01Orange NoidaОценок пока нет

- HCL Comnet CPRДокумент5 страницHCL Comnet CPROrange NoidaОценок пока нет

- 2007-2008 Annual Report of HCLДокумент107 страниц2007-2008 Annual Report of HCLOrange Noida100% (1)

- Unearthingthepowerofibmrationalfunctionaltester7 0 RFT 090729230029 Phpapp02Документ2 страницыUnearthingthepowerofibmrationalfunctionaltester7 0 RFT 090729230029 Phpapp02Orange NoidaОценок пока нет

- HCL Comnet CPRДокумент5 страницHCL Comnet CPROrange NoidaОценок пока нет

- Digital Strategy and Social IntegrationДокумент34 страницыDigital Strategy and Social IntegrationsaumyavishОценок пока нет

- HCL Comnet CPRДокумент5 страницHCL Comnet CPROrange NoidaОценок пока нет

- HCL TechДокумент37 страницHCL TechOrange NoidaОценок пока нет

- Investor Presentation Jan 2013Документ25 страницInvestor Presentation Jan 2013Orange NoidaОценок пока нет

- HCL TechДокумент37 страницHCL TechOrange NoidaОценок пока нет

- HCL Comnet CPRДокумент5 страницHCL Comnet CPROrange NoidaОценок пока нет

- Investor Presentation Jan 2013Документ25 страницInvestor Presentation Jan 2013Orange NoidaОценок пока нет

- 2017 Sec 4E5N Prelim Paper 2 - AnsДокумент7 страниц2017 Sec 4E5N Prelim Paper 2 - AnsDamien SeowОценок пока нет

- Identify The Choice That Best Completes The Statement or Answers The QuestionДокумент20 страницIdentify The Choice That Best Completes The Statement or Answers The QuestionFebby Grace Villaceran Sabino0% (2)

- Revised Implementing Rules and Regulations (IRR)Документ12 страницRevised Implementing Rules and Regulations (IRR)Cez Yassan100% (1)

- Money - Time Relationships and Equivalence: Name of Student/s: Dickinson, Sigienel Gabriel, Neil Patrick AДокумент12 страницMoney - Time Relationships and Equivalence: Name of Student/s: Dickinson, Sigienel Gabriel, Neil Patrick ASasuke UchichaОценок пока нет

- Aga Mimeographing ServicesДокумент9 страницAga Mimeographing ServicesKeaith RoxannheОценок пока нет

- TAXATION001Документ31 страницаTAXATION001Boqorka AmericaОценок пока нет

- Bahan Ajar Intercompany InventoryДокумент16 страницBahan Ajar Intercompany InventoryZachra MeirizaОценок пока нет

- Income Tax II Illustration Clubbing of Incomes PDFДокумент1 страницаIncome Tax II Illustration Clubbing of Incomes PDFSubramanian SenthilОценок пока нет

- Stealth Income Strategies For InvestorsДокумент116 страницStealth Income Strategies For Investorsrypai50% (4)

- SHE IntaccДокумент5 страницSHE IntaccLavillaОценок пока нет

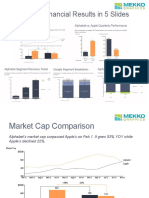

- Analysis of Financial Performance For AlphabetДокумент6 страницAnalysis of Financial Performance For AlphabetPham Ha AnОценок пока нет

- Accounts - Track 1B2 - Class Notes NovDec 2022Документ237 страницAccounts - Track 1B2 - Class Notes NovDec 2022chandsultana45690Оценок пока нет

- Cost Bookkeeping AnswersДокумент9 страницCost Bookkeeping AnswersMuhammad Hassan Uddin100% (1)

- A Beginners Guide To The Stock Market Everything You Need To Start Making Money Today by Kratter, Matthew R. (Kratter, Matthew R.)Документ70 страницA Beginners Guide To The Stock Market Everything You Need To Start Making Money Today by Kratter, Matthew R. (Kratter, Matthew R.)Simple ReaderОценок пока нет

- Acctg 205A Midterm Examinations Problem 1Документ1 страницаAcctg 205A Midterm Examinations Problem 1YameteKudasaiОценок пока нет

- Financial Management (Payongayong, 2nd Ed) - Chapter 1Документ10 страницFinancial Management (Payongayong, 2nd Ed) - Chapter 1Auie Eugene Frae Salamera0% (1)

- Problem SolvingДокумент32 страницыProblem SolvingJoanna Paula MagadiaОценок пока нет

- Estate Tax Activities (Questions)Документ4 страницыEstate Tax Activities (Questions)Christine Nathalie BalmesОценок пока нет

- Internals II - Managerial Accounting Question PaperДокумент3 страницыInternals II - Managerial Accounting Question PaperasdeОценок пока нет

- Bernas Karla Pauline 11 Bonifacio FABM1 Q4Документ45 страницBernas Karla Pauline 11 Bonifacio FABM1 Q4Karla pauline BernasОценок пока нет

- The Determinant of The Indonesia Composite Stock Price Index and Its Implication To Indonesia Foreign Direct Investment For Manufactur Sector PDFДокумент5 страницThe Determinant of The Indonesia Composite Stock Price Index and Its Implication To Indonesia Foreign Direct Investment For Manufactur Sector PDFRengki RamaОценок пока нет

- Accounting Standards (Satyanath Mohapatra)Документ39 страницAccounting Standards (Satyanath Mohapatra)smrutiranjan swain100% (1)

- Piling Works Tender For NrepДокумент10 страницPiling Works Tender For NrepPratik GuptaОценок пока нет

- CVP and Break-Even Analysis - RoqueДокумент33 страницыCVP and Break-Even Analysis - RoqueTrisha Mae AlburoОценок пока нет

- Acc101 Aug 2020 QNДокумент15 страницAcc101 Aug 2020 QNОзода АбдумуминоваОценок пока нет

- Trac Nghiem Tieng AnhДокумент4 страницыTrac Nghiem Tieng AnhHieu PhanОценок пока нет

- FFC vs. EngroДокумент36 страницFFC vs. EngroAnsaria100% (1)

- WCM - Unit 2 Cash ManagementДокумент51 страницаWCM - Unit 2 Cash ManagementkartikОценок пока нет

- ACCA F6UK December 2015 Notes PDFДокумент264 страницыACCA F6UK December 2015 Notes PDFopentuitionID100% (2)