Вам также может понравиться

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- Nilson 1183 PDF Way2pay 99 07 15Документ16 страницNilson 1183 PDF Way2pay 99 07 15Elena Elena100% (1)

- Graphic Designer (6 Months)Документ41 страницаGraphic Designer (6 Months)Sh Mati Elahi100% (1)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- CBM Individual Credit Report (Sample)Документ7 страницCBM Individual Credit Report (Sample)BotaОценок пока нет

- Picture Characters CHINESE PDFДокумент225 страницPicture Characters CHINESE PDFElisabeth KristinaОценок пока нет

- 2 (A) Case Study-Istisna NewДокумент20 страниц2 (A) Case Study-Istisna Newafshi1850% (2)

- Managers Who Make A Difference PDFДокумент44 страницыManagers Who Make A Difference PDFkamalkantmbbs100% (3)

- Application Form FOR THE SESSION 2016-2017 (Use Capital Letters)Документ4 страницыApplication Form FOR THE SESSION 2016-2017 (Use Capital Letters)Sh Mati ElahiОценок пока нет

- Barrier Films: Product CategoriesДокумент3 страницыBarrier Films: Product CategoriesSh Mati ElahiОценок пока нет

- Chinar Bagh Payment PlanДокумент1 страницаChinar Bagh Payment PlanSh Mati ElahiОценок пока нет

- Goal Ranges For People Without Diabetes Goal Ranges For People With DiabetesДокумент1 страницаGoal Ranges For People Without Diabetes Goal Ranges For People With DiabetesSh Mati ElahiОценок пока нет

- Morning Before Meal/ Fasting: Shahida Mahboob 1 2 3 4 5 6 7 8Документ4 страницыMorning Before Meal/ Fasting: Shahida Mahboob 1 2 3 4 5 6 7 8Sh Mati ElahiОценок пока нет

- Barrier Films: Product CategoriesДокумент3 страницыBarrier Films: Product CategoriesSh Mati ElahiОценок пока нет

- Insulated Insoline Zoltar: Shahida MahboobДокумент4 страницыInsulated Insoline Zoltar: Shahida MahboobSh Mati ElahiОценок пока нет

- CCTV Technician (3-Months)Документ12 страницCCTV Technician (3-Months)Sh Mati ElahiОценок пока нет

- Application Form FOR THE SESSION 2016-2017 (Use Capital Letters)Документ4 страницыApplication Form FOR THE SESSION 2016-2017 (Use Capital Letters)Sh Mati ElahiОценок пока нет

- David's Super Sale: Get 25% Discount On Any Order With Coupon: SuperДокумент27 страницDavid's Super Sale: Get 25% Discount On Any Order With Coupon: SuperSh Mati ElahiОценок пока нет

- Computer Hardware Technician (6 Months)Документ39 страницComputer Hardware Technician (6 Months)Sh Mati ElahiОценок пока нет

- Computer Business Management IT Office Assistant (6 Months)Документ82 страницыComputer Business Management IT Office Assistant (6 Months)Sh Mati Elahi100% (1)

- Graph Theory Seminars Feb-Marc-2016Документ1 страницаGraph Theory Seminars Feb-Marc-2016Sh Mati ElahiОценок пока нет

- Ÿ Ÿ Ÿ Ÿllll Ò Ò Ò Ò Åååå " " " ": (Polyanthes (Ammaryllidaceae)Документ3 страницыŸ Ÿ Ÿ Ÿllll Ò Ò Ò Ò Åååå " " " ": (Polyanthes (Ammaryllidaceae)Sh Mati ElahiОценок пока нет

- Car Wash Service Station Rs. 4.09 Million Jun 2015Документ18 страницCar Wash Service Station Rs. 4.09 Million Jun 2015Sh Mati ElahiОценок пока нет

- CCTV Technician (3-Months)Документ12 страницCCTV Technician (3-Months)Sh Mati ElahiОценок пока нет

- Application Form For Membership: Personal DetailsДокумент2 страницыApplication Form For Membership: Personal DetailsnalakasaОценок пока нет

- Essay Fintech Vs Traditional Tech - Angela Putri KeziaДокумент4 страницыEssay Fintech Vs Traditional Tech - Angela Putri KeziaAngela KeziaОценок пока нет

- Internship Report On at Siddhart Bank Limited JanakpurdhamДокумент39 страницInternship Report On at Siddhart Bank Limited JanakpurdhamAshish Kumar100% (1)

- Accounting Ratios PDFДокумент56 страницAccounting Ratios PDFdavid100% (1)

- F12BBДокумент2 страницыF12BBAkshay PagariyaОценок пока нет

- SBP Market OperationsДокумент26 страницSBP Market OperationsAnas JameelОценок пока нет

- Commerce EM PDFДокумент344 страницыCommerce EM PDFkarthik_be_eeeОценок пока нет

- Priya KapilДокумент93 страницыPriya KapilaamritaaОценок пока нет

- Credit Manual: United Bank LimitedДокумент120 страницCredit Manual: United Bank LimitedAsif RafiОценок пока нет

- Format For Company Bank Account OpeningДокумент2 страницыFormat For Company Bank Account OpeningLeo PrabhuОценок пока нет

- Future Value ProblemsДокумент2 страницыFuture Value Problemsrohitrgt4uОценок пока нет

- Letter of CreditДокумент4 страницыLetter of CreditRahul Mehrotra67% (3)

- KeemekДокумент3 страницыKeemekAshwani KhandelwalОценок пока нет

- MitonOptimal Group FinalДокумент33 страницыMitonOptimal Group FinalRonald YeoОценок пока нет

- Arms Length Transaction - 633873359516238640Документ4 страницыArms Length Transaction - 633873359516238640Fred ShocknessОценок пока нет

- Sbi Corporate Credit CardДокумент9 страницSbi Corporate Credit CardArvindОценок пока нет

- CG Alias - AnswДокумент2 страницыCG Alias - AnswMohamad YusofОценок пока нет

- Accounting Systems For Thrift Co-Operatives Promoted by Co-OperativeДокумент42 страницыAccounting Systems For Thrift Co-Operatives Promoted by Co-OperativemadhanagopalОценок пока нет

- ShortTerm Rental Agreement TEMPLATEДокумент5 страницShortTerm Rental Agreement TEMPLATELodgix.comОценок пока нет

- OtceiДокумент18 страницOtceirthi04Оценок пока нет

- Bismillah Group ScandalДокумент3 страницыBismillah Group ScandalAhmad HОценок пока нет

- First National Bank - Google SearchДокумент1 страницаFirst National Bank - Google SearchNiaaries JimОценок пока нет

- Statement 20190105044590Документ3 страницыStatement 20190105044590DanielОценок пока нет

- Banking Careers Guide 09 2022Документ117 страницBanking Careers Guide 09 2022李深淼Оценок пока нет

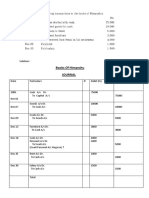

- Books of Himanshu JournalДокумент4 страницыBooks of Himanshu Journalrakesh19865Оценок пока нет

- FM - 1 - Accounts of Professional PersonsДокумент15 страницFM - 1 - Accounts of Professional Personsyagnesh trivedi100% (1)