Вам также может понравиться

- CH 3 - The Problems With Conventional AccountingДокумент52 страницыCH 3 - The Problems With Conventional AccountingCondro TriharyonoОценок пока нет

- CH 3 - The Problems With Conventional AccountingДокумент52 страницыCH 3 - The Problems With Conventional AccountingCondro TriharyonoОценок пока нет

- ACC 6810 Lesson 2Документ20 страницACC 6810 Lesson 2Condro TriharyonoОценок пока нет

- Need For Islamic AccountingДокумент57 страницNeed For Islamic AccountingCondro TriharyonoОценок пока нет

- Jurnal Islam AkuntaniДокумент16 страницJurnal Islam AkuntaniCondro TriharyonoОценок пока нет

- Jurnal Islam Akuntasi Syariah PDFДокумент11 страницJurnal Islam Akuntasi Syariah PDFCondro TriharyonoОценок пока нет

- Jurnal Akuntansi Syariah IndonesiaДокумент4 страницыJurnal Akuntansi Syariah IndonesiaCondro TriharyonoОценок пока нет

- CH 3 - The Problems With Conventional AccountingДокумент52 страницыCH 3 - The Problems With Conventional AccountingCondro TriharyonoОценок пока нет

- Jurnal Akuntansi IslamДокумент19 страницJurnal Akuntansi IslamCondro TriharyonoОценок пока нет

- Jurnal Islam Akuntansi 2Документ23 страницыJurnal Islam Akuntansi 2Condro TriharyonoОценок пока нет

- Jurnal Islam IndnesiaДокумент16 страницJurnal Islam IndnesiaCondro TriharyonoОценок пока нет

- Jurnal Islam AkuntansiДокумент15 страницJurnal Islam AkuntansiCondro TriharyonoОценок пока нет

- Jurnl Islam IndonesiaДокумент6 страницJurnl Islam IndonesiaCondro TriharyonoОценок пока нет

- GiantsДокумент17 страницGiantsCondro TriharyonoОценок пока нет

- UntitledДокумент1 страницаUntitledCondro TriharyonoОценок пока нет

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5782)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (265)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (119)

- Fiscal Theory and Public PolicyДокумент41 страницаFiscal Theory and Public PolicyClint RamosОценок пока нет

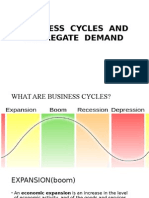

- Understanding Business Cycles and Aggregate DemandДокумент40 страницUnderstanding Business Cycles and Aggregate DemandSnehal Joshi100% (1)

- Impact of Monetary Policy On Economic Growth - A Case Study of South AfricaДокумент9 страницImpact of Monetary Policy On Economic Growth - A Case Study of South AfricaAbdulkabirОценок пока нет

- The 28 Great Ideas That Changed The World ShowДокумент69 страницThe 28 Great Ideas That Changed The World ShowJeff AkinОценок пока нет

- Question and Answer - 5Документ30 страницQuestion and Answer - 5acc-expertОценок пока нет

- An Abridged History of Labour MovementДокумент32 страницыAn Abridged History of Labour Movementximena.torresОценок пока нет

- ECON 3008: History of Economic Thought: SEMESTER 2-2016 Keynesians and MonetaristsДокумент22 страницыECON 3008: History of Economic Thought: SEMESTER 2-2016 Keynesians and MonetaristsKishawn SmithОценок пока нет

- Economic School of ThoughtДокумент199 страницEconomic School of ThoughtMinakshi Barman100% (1)

- Introduction To Economics - Class NotesДокумент33 страницыIntroduction To Economics - Class NotesEliot PrimoОценок пока нет

- Keynesian Economics Explained: How Government Spending Boosts GrowthДокумент14 страницKeynesian Economics Explained: How Government Spending Boosts GrowthMisha KosiakovОценок пока нет

- The Fall of The House of Credit PDFДокумент382 страницыThe Fall of The House of Credit PDFRichard JohnОценок пока нет

- Starting Over Again - The Covid-19 Pandemic Is Forcing A Rethink in Macroeconomics - Briefing - The EconomistДокумент20 страницStarting Over Again - The Covid-19 Pandemic Is Forcing A Rethink in Macroeconomics - Briefing - The EconomistblacksmithMGОценок пока нет

- Fatal Couplings of Power and DifferenceДокумент10 страницFatal Couplings of Power and DifferenceJoohyun KimОценок пока нет

- Monetary Policy Notes PDFДокумент18 страницMonetary Policy Notes PDFOptimistic Khan50% (2)

- Lecture Notes On Inflation: Meaning, Theories, and Costs/EffectsДокумент39 страницLecture Notes On Inflation: Meaning, Theories, and Costs/EffectsAnonymous yy8In96j0rОценок пока нет

- H3 Economics PapersДокумент21 страницаH3 Economics Papersdavidboh100% (1)

- MacroExam2SelfTest AnswersДокумент9 страницMacroExam2SelfTest AnswersIves LeeОценок пока нет

- Principles of Economics Business Banking Finance and Your Everyday Life Peter NavarroДокумент81 страницаPrinciples of Economics Business Banking Finance and Your Everyday Life Peter NavarroWaris Awais100% (2)

- Settling the Accounts of Revolutionary Democracy in EthiopiaДокумент31 страницаSettling the Accounts of Revolutionary Democracy in EthiopiaKaleb Berhanu100% (1)

- Modern Macroeconomics QuizДокумент115 страницModern Macroeconomics Quizimmoenix0% (1)

- 2008-2009 Keynesian Resurgence: Navigation SearchДокумент19 страниц2008-2009 Keynesian Resurgence: Navigation SearchAppan Kandala VasudevacharyОценок пока нет

- Inflation in India: An Analytical Survey: The TheДокумент1 страницаInflation in India: An Analytical Survey: The TheTio KumowalОценок пока нет

- Economic Terms Glossary PDFДокумент12 страницEconomic Terms Glossary PDFannayaОценок пока нет

- Money, Bank Credit, Economic CyclesДокумент906 страницMoney, Bank Credit, Economic CyclesBot Psalmerna100% (3)

- Monetary Reform and The Bellagio GroupДокумент4 страницыMonetary Reform and The Bellagio GroupPickering and ChattoОценок пока нет

- NullДокумент22 страницыNullapi-28191758100% (1)

- Economics: DR P James Daniel Paul Professor VIT BSДокумент29 страницEconomics: DR P James Daniel Paul Professor VIT BSAntony JohnОценок пока нет

- What is the Quantity Theory of Money? (39Документ4 страницыWhat is the Quantity Theory of Money? (39Nazmun BegamОценок пока нет

- Ace Institute of Management: Assignment: Inflation in NepalДокумент7 страницAce Institute of Management: Assignment: Inflation in NepalRupesh ShahОценок пока нет

- Jun18l1-S02pm QaДокумент22 страницыJun18l1-S02pm QajuanОценок пока нет