Вам также может понравиться

- Introduction To Healthcare Quality Management (PDFDrive - Com) - 1 PDFДокумент50 страницIntroduction To Healthcare Quality Management (PDFDrive - Com) - 1 PDFAffandi Akbar100% (2)

- Geotech LecДокумент364 страницыGeotech LecBeatriz Devera TongolОценок пока нет

- Livestock Fattening Business Plan 100Документ38 страницLivestock Fattening Business Plan 100Kayode Adebayo100% (1)

- E & y Sap S4hanaДокумент8 страницE & y Sap S4hanaShreeОценок пока нет

- Engineering Economy: Interest and Money-Time RelationshipsДокумент21 страницаEngineering Economy: Interest and Money-Time RelationshipsanonОценок пока нет

- Activity 1 Engineering Economy: I PRTДокумент5 страницActivity 1 Engineering Economy: I PRTtaliya cocoОценок пока нет

- Module 00 Engineering Economics PDFДокумент330 страницModule 00 Engineering Economics PDFJON EDWARD ABAYAОценок пока нет

- Mastering CPRE v2.0 SampleДокумент40 страницMastering CPRE v2.0 SampleMitchell J. Sharoff100% (1)

- EECOДокумент6 страницEECOJohnОценок пока нет

- Chapter No. 1: ContentДокумент101 страницаChapter No. 1: ContentVipul AdateОценок пока нет

- Other Annuity TypesДокумент7 страницOther Annuity TypesLevi John Corpin AmadorОценок пока нет

- Seatwork7 Withanswer Final PDFДокумент3 страницыSeatwork7 Withanswer Final PDFLester John PrecillasОценок пока нет

- Engineering EconomyДокумент5 страницEngineering EconomyDayLe Ferrer AbapoОценок пока нет

- Wisdom Diary On Divine PresenceДокумент11 страницWisdom Diary On Divine PresenceChikwason Sarcozy MwanzaОценок пока нет

- Nqesh Reviewer For Deped PampangaДокумент3 страницыNqesh Reviewer For Deped PampangaRonald Esquillo100% (1)

- NUt 6 SA9 SSN 65Документ38 страницNUt 6 SA9 SSN 65Don RomantikoОценок пока нет

- Engineering Economy AccountingДокумент198 страницEngineering Economy AccountingJericho Dizon TorresОценок пока нет

- Simple Interest Compound InterestДокумент6 страницSimple Interest Compound InterestKaye OleaОценок пока нет

- Unit 2 Time and Money D PDFДокумент2 страницыUnit 2 Time and Money D PDFCarmelo Janiza LavareyОценок пока нет

- EE40 Homework 1Документ2 страницыEE40 Homework 1delacruzrae12Оценок пока нет

- Depreciation Matheson Formula & The Sum of The Years - Digits (Syd)Документ15 страницDepreciation Matheson Formula & The Sum of The Years - Digits (Syd)Naidy De HittaОценок пока нет

- II. Compound InterestДокумент21 страницаII. Compound InterestFrancis De GuzmanОценок пока нет

- Sample of Feasibility StudyДокумент25 страницSample of Feasibility StudyShiela PerdidoОценок пока нет

- Hue HueДокумент26 страницHue HueWex Senin Alcantara100% (1)

- 8 - DepreciationДокумент3 страницы8 - Depreciationjoyce san joseОценок пока нет

- ES 33 - Plate No. 1Документ10 страницES 33 - Plate No. 1Maybelline DipasupilОценок пока нет

- Practice ProblemsДокумент1 страницаPractice ProblemsYss CastañedaОценок пока нет

- Part Ii-Works of RizalДокумент10 страницPart Ii-Works of RizalLourdes ArguellesОценок пока нет

- Continuous & Discrete CompoundingДокумент3 страницыContinuous & Discrete CompoundingJohnlloyd BarretoОценок пока нет

- CH.3 Annuity PDFДокумент29 страницCH.3 Annuity PDFJenalyn MacarilayОценок пока нет

- Regine Mae Yaniza - 2 Year BsceДокумент11 страницRegine Mae Yaniza - 2 Year BsceRegine Mae Lustica YanizaОценок пока нет

- Activity in Double Declining Balance DepreciationДокумент2 страницыActivity in Double Declining Balance DepreciationTet GomezОценок пока нет

- Cee 109 - First ExamДокумент43 страницыCee 109 - First ExamRonald Renon QuiranteОценок пока нет

- Engineering Economics: Rate of Return AnalysisДокумент29 страницEngineering Economics: Rate of Return AnalysisEkoОценок пока нет

- Eeco 111716Документ20 страницEeco 111716Rom HoboiiОценок пока нет

- CE155P Module Exam 1Документ4 страницыCE155P Module Exam 1Kelly Mae Viray100% (1)

- Engineering Economy ReviewerДокумент5 страницEngineering Economy ReviewerBea Abesamis100% (1)

- 7 Seatwork Annuity Second SetДокумент1 страница7 Seatwork Annuity Second SetNobel Engzen Du Bermoy100% (1)

- Task #2 Practice Problems PDFДокумент1 страницаTask #2 Practice Problems PDFkate asiaticoОценок пока нет

- RCD 2Документ4 страницыRCD 2John Joshua DavantesОценок пока нет

- Problem 267 Resultant Non Concurrent Force System PDFДокумент5 страницProblem 267 Resultant Non Concurrent Force System PDFCrstn-26Оценок пока нет

- Eecon 1-Engineering Economy: (Depreciation, Capitalized Cost, Depletion Cost, Annual Cost and Bond)Документ41 страницаEecon 1-Engineering Economy: (Depreciation, Capitalized Cost, Depletion Cost, Annual Cost and Bond)Mark Anthony GarciaОценок пока нет

- ENGINEERING ECONOMY With ANSWER KEYДокумент14 страницENGINEERING ECONOMY With ANSWER KEYKAMIKAZIОценок пока нет

- Spiral Curve Earthworks and Hydrographic SurveyДокумент7 страницSpiral Curve Earthworks and Hydrographic Surveykevin_ramos007100% (1)

- Soil Classification: and Materials) Is Used For Virtually All Geotechnical Engineering Works Except Highway and RoadДокумент3 страницыSoil Classification: and Materials) Is Used For Virtually All Geotechnical Engineering Works Except Highway and RoadPeter D.Оценок пока нет

- Additional ExercisesДокумент4 страницыAdditional Exerciseschinoi C100% (1)

- Engineering Econ. - ANNUITYДокумент35 страницEngineering Econ. - ANNUITYNikolai VillegasОценок пока нет

- Sharing Is CaringДокумент4 страницыSharing Is CaringChris bongalosaОценок пока нет

- De La Pena, Mary Princess C. BSME-3C-Engineering EconomyДокумент6 страницDe La Pena, Mary Princess C. BSME-3C-Engineering EconomyJohn A. CenizaОценок пока нет

- Hypothesis Testing For One PopulationДокумент57 страницHypothesis Testing For One PopulationFarah CakeyОценок пока нет

- Evaluating Single Project: PROBLEM SET: Money-Time RelationshipsДокумент4 страницыEvaluating Single Project: PROBLEM SET: Money-Time RelationshipsAnjo Vasquez100% (1)

- Chapter 4 Additional Sample Problems For Comparison of AlternativesДокумент5 страницChapter 4 Additional Sample Problems For Comparison of AlternativesIyahОценок пока нет

- Assignment #5 (Sep2019) - GDB3023-SolutionДокумент4 страницыAssignment #5 (Sep2019) - GDB3023-SolutionDanish Zabidi100% (1)

- AllptДокумент26 страницAllptKidlat0% (1)

- Sum of The Years MethodДокумент2 страницыSum of The Years MethodKristin ByrdОценок пока нет

- Methods of Comparing Alternative ProposalsДокумент34 страницыMethods of Comparing Alternative Proposalsrobel popОценок пока нет

- Engineering Economics, Chapter 8Документ23 страницыEngineering Economics, Chapter 8Bach Le NguyenОценок пока нет

- FInalДокумент7 страницFInalRyan Martinez0% (1)

- Depreciation ConceptДокумент22 страницыDepreciation ConceptJulie Ann ZafraОценок пока нет

- Chu P2C2 - Rick RigsbyДокумент1 страницаChu P2C2 - Rick RigsbyChu carloОценок пока нет

- Statics of Rigid Bodies 1: Email AddressДокумент15 страницStatics of Rigid Bodies 1: Email AddressKc Kirsten Kimberly MalbunОценок пока нет

- Design of Flexible and Rigid PavementДокумент29 страницDesign of Flexible and Rigid Pavementrodge macaraegОценок пока нет

- Manegerial EconomicsДокумент17 страницManegerial EconomicsPrincess EscovidalОценок пока нет

- The Water Sprinkler A Is Placed On Sloping Ground and Oscillates in The XyДокумент14 страницThe Water Sprinkler A Is Placed On Sloping Ground and Oscillates in The XyChristine Joyce BunyiОценок пока нет

- AnnuitiesДокумент4 страницыAnnuitiesJohn Nicole Villas CapulongОценок пока нет

- Year Book Value at The Beginning of The Year (P) Depreciation (P) Book Value at The End of The Year (P) 1 2 3 4 5Документ9 страницYear Book Value at The Beginning of The Year (P) Depreciation (P) Book Value at The End of The Year (P) 1 2 3 4 5Kevin SimonsОценок пока нет

- DepreciationДокумент6 страницDepreciationSYOUSUF45Оценок пока нет

- Kpi SkapsДокумент2 страницыKpi SkapsChikwason Sarcozy MwanzaОценок пока нет

- Unification Germany ItalyДокумент8 страницUnification Germany ItalyChikwason Sarcozy Mwanza100% (1)

- Housing Assignment 510 Group 2Документ3 страницыHousing Assignment 510 Group 2Chikwason Sarcozy MwanzaОценок пока нет

- Using Building Information Modeling (Bim) ToДокумент10 страницUsing Building Information Modeling (Bim) ToChikwason Sarcozy MwanzaОценок пока нет

- Proposed Programme of Works For 1X 2 CRBДокумент1 страницаProposed Programme of Works For 1X 2 CRBChikwason Sarcozy MwanzaОценок пока нет

- ElisДокумент5 страницElisChikwason Sarcozy MwanzaОценок пока нет

- Materials at New MasalaДокумент18 страницMaterials at New MasalaChikwason Sarcozy MwanzaОценок пока нет

- Building Information Modelling (Bim) : A New Approach To Improving Design and Construction in The Z.C.IДокумент3 страницыBuilding Information Modelling (Bim) : A New Approach To Improving Design and Construction in The Z.C.IChikwason Sarcozy MwanzaОценок пока нет

- Table of ContentsДокумент1 страницаTable of ContentsChikwason Sarcozy MwanzaОценок пока нет

- In The High Court For Zambia 2013Документ3 страницыIn The High Court For Zambia 2013Chikwason Sarcozy MwanzaОценок пока нет

- A Report On Works Done With Jumucha Enterprises Limitedccording Me An Opportunity To WooДокумент8 страницA Report On Works Done With Jumucha Enterprises Limitedccording Me An Opportunity To WooChikwason Sarcozy MwanzaОценок пока нет

- Ubumi Bwa Bantu Non Governmental Organisation.: Project Title: Community MobilisationДокумент1 страницаUbumi Bwa Bantu Non Governmental Organisation.: Project Title: Community MobilisationChikwason Sarcozy MwanzaОценок пока нет

- Building Economics Assignment OneДокумент10 страницBuilding Economics Assignment OneChikwason Sarcozy MwanzaОценок пока нет

- The Copperbelt University: Building Science DepartmentДокумент1 страницаThe Copperbelt University: Building Science DepartmentChikwason Sarcozy MwanzaОценок пока нет

- Old Columbia Pike, Silver Spring, MD 20904 Zdravko Stefanovicć Clifford R. Goldstein Soraya Homayouni Lea Alexander GreveДокумент5 страницOld Columbia Pike, Silver Spring, MD 20904 Zdravko Stefanovicć Clifford R. Goldstein Soraya Homayouni Lea Alexander GreveChikwason Sarcozy MwanzaОценок пока нет

- The Copperbelt University: Building Science DepartmentДокумент1 страницаThe Copperbelt University: Building Science DepartmentChikwason Sarcozy MwanzaОценок пока нет

- Specific Performance: Sally KaneДокумент1 страницаSpecific Performance: Sally KaneChikwason Sarcozy MwanzaОценок пока нет

- Eaq213 03Документ8 страницEaq213 03Chikwason Sarcozy MwanzaОценок пока нет

- Re: Application For The Position of Assistant AccountantДокумент2 страницыRe: Application For The Position of Assistant AccountantChikwason Sarcozy MwanzaОценок пока нет

- Agency Content PageДокумент1 страницаAgency Content PageChikwason Sarcozy MwanzaОценок пока нет

- (Hosea) : Love and Judgment: God's DilemmaДокумент8 страниц(Hosea) : Love and Judgment: God's DilemmaChikwason Sarcozy MwanzaОценок пока нет

- Cover PageДокумент1 страницаCover PageChikwason Sarcozy MwanzaОценок пока нет

- Eaq213 01Документ8 страницEaq213 01Chikwason Sarcozy MwanzaОценок пока нет

- Name: Masumba Stalline. Computer Number: 06054216. Proposed Supervisors: Mr. J HansonДокумент2 страницыName: Masumba Stalline. Computer Number: 06054216. Proposed Supervisors: Mr. J HansonChikwason Sarcozy MwanzaОценок пока нет

- The Copperbelt University: School of Built EnvironmentДокумент1 страницаThe Copperbelt University: School of Built EnvironmentChikwason Sarcozy MwanzaОценок пока нет

- Bible Sense For Getting Into MarriageДокумент9 страницBible Sense For Getting Into MarriageChikwason Sarcozy MwanzaОценок пока нет

- Esb 420Документ11 страницEsb 420Chikwason Sarcozy MwanzaОценок пока нет

- Table of ContentsДокумент1 страницаTable of ContentsChikwason Sarcozy MwanzaОценок пока нет

- The Power Pact Names of GodДокумент1 страницаThe Power Pact Names of GodChikwason Sarcozy MwanzaОценок пока нет

- KRU Affiliation Fee ChallanДокумент1 страницаKRU Affiliation Fee ChallansuryanetsОценок пока нет

- Chap 001Документ14 страницChap 001Adi Susilo100% (1)

- AFL 1 Marketing Strategy Matthew Clement 0106021910041Документ4 страницыAFL 1 Marketing Strategy Matthew Clement 0106021910041Matthew ClementОценок пока нет

- Oriental Engineering Works PVTДокумент20 страницOriental Engineering Works PVTDarshan DhimanОценок пока нет

- Earlier This Month, Your Company, A Running Equipment Designer and ManufacturerДокумент2 страницыEarlier This Month, Your Company, A Running Equipment Designer and Manufacturermayank goyalОценок пока нет

- ADM 016 ACRS Certification Agreement (Version 3.1) WebДокумент23 страницыADM 016 ACRS Certification Agreement (Version 3.1) WebMonica SinghОценок пока нет

- Slide Isb 540Документ14 страницSlide Isb 540Syamil Hakim Abdul GhaniОценок пока нет

- WHSmith Indonesia Shortened Presentation Mar 2014Документ28 страницWHSmith Indonesia Shortened Presentation Mar 2014Benjamin James SmithОценок пока нет

- FARAP 4404 Property Plant EquipmentДокумент11 страницFARAP 4404 Property Plant EquipmentJohn Ray RonaОценок пока нет

- Materials Management I. Chapter SummaryДокумент2 страницыMaterials Management I. Chapter SummaryLucille TevesОценок пока нет

- Anurag ShuklaДокумент23 страницыAnurag Shukladeepkamal_jaiswalОценок пока нет

- Eiasm Paper Spanhove&VerhoestДокумент40 страницEiasm Paper Spanhove&Verhoestion dogeanuОценок пока нет

- SAP Profit Center AccountingДокумент5 страницSAP Profit Center AccountingVinoth Kumar PeethambaramОценок пока нет

- Project Report ON "A Customer Behaviour and Satisfaction Level For Hero Motocorp LTD."Документ57 страницProject Report ON "A Customer Behaviour and Satisfaction Level For Hero Motocorp LTD."abhaybittuОценок пока нет

- The Issues On Corporate GovernanceДокумент15 страницThe Issues On Corporate Governanceanitama_aminОценок пока нет

- Building & Restructuring The CorporationДокумент17 страницBuilding & Restructuring The CorporationziaeceОценок пока нет

- Worldcom - The Story of A WhistleblowerДокумент5 страницWorldcom - The Story of A WhistleblowerYeni Hanisah PiliangОценок пока нет

- Value of A Bond: Arbitrage-Free Valuation Approach For BondsДокумент5 страницValue of A Bond: Arbitrage-Free Valuation Approach For BondsXyza Faye RegaladoОценок пока нет

- Group Assignment TaxationДокумент20 страницGroup Assignment TaxationEnat Endawoke100% (1)

- Cafe Coffee Day Coalition Marketing ProgrammeДокумент3 страницыCafe Coffee Day Coalition Marketing ProgrammeKhalid Abdul LatifОценок пока нет

- McKinsey Matrix - GE Business ScreenДокумент2 страницыMcKinsey Matrix - GE Business Screenpallav86Оценок пока нет

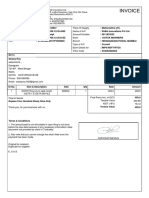

- Invoice 32Документ1 страницаInvoice 32Sanjoy RoyОценок пока нет

- Maintenance Spare Parts Logistics: Special Characteristics and Strategic ChoicesДокумент10 страницMaintenance Spare Parts Logistics: Special Characteristics and Strategic ChoicesLheoОценок пока нет

- Individual Assignment: Software Quality Engineering Hi-Tech Crop. Case Study'Документ23 страницыIndividual Assignment: Software Quality Engineering Hi-Tech Crop. Case Study'Md Sakhiruj Jaman SalimОценок пока нет