Вам также может понравиться

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (894)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (119)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2219)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (265)

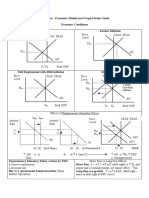

- AP Macroeconomic Models and Graphs Study GuideДокумент23 страницыAP Macroeconomic Models and Graphs Study GuideGabriel Jimenez100% (7)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- Overview of the Economy and Everyday Life in BritainДокумент9 страницOverview of the Economy and Everyday Life in BritainCua NhậtОценок пока нет

- Assignment On Intermediate Macro Economic (ECN 303) - USEDДокумент6 страницAssignment On Intermediate Macro Economic (ECN 303) - USEDBernardokpeОценок пока нет

- Dividend SmoothingДокумент63 страницыDividend SmoothingNawsher210% (1)

- Fair Value Accounting and Pro-CyclicalityДокумент100 страницFair Value Accounting and Pro-CyclicalityNawsher21Оценок пока нет

- Getting Started With StataДокумент11 страницGetting Started With StataNawsher21Оценок пока нет

- Does The Contribution of Corporate Cash HoldingsДокумент27 страницDoes The Contribution of Corporate Cash HoldingsNawsher21Оценок пока нет

- Tax and British Business Making The Case PDFДокумент24 страницыTax and British Business Making The Case PDFNawsher21Оценок пока нет

- Acca Corporate Sector CareerДокумент12 страницAcca Corporate Sector CareerNawsher21Оценок пока нет

- Acca Corporate Sector CareerДокумент12 страницAcca Corporate Sector CareerNawsher21Оценок пока нет

- COSO Framework - September 2012Документ166 страницCOSO Framework - September 2012Nawsher21Оценок пока нет

- COSO Framework - September 2012Документ166 страницCOSO Framework - September 2012Nawsher21Оценок пока нет

- Dividend PuzzleДокумент40 страницDividend PuzzleNawsher21Оценок пока нет

- Questions & Solutions ACCTДокумент246 страницQuestions & Solutions ACCTMel Lissa33% (3)

- The Credit Rating Agencies Role of SECДокумент17 страницThe Credit Rating Agencies Role of SECNawsher21Оценок пока нет

- ER and Currency BoardsДокумент41 страницаER and Currency BoardsNawsher21Оценок пока нет

- Nichols How Do Earnings Numbers PDFДокумент24 страницыNichols How Do Earnings Numbers PDFNawsher21Оценок пока нет

- Process Engineering Economics and ManagementДокумент6 страницProcess Engineering Economics and ManagementkayeОценок пока нет

- Inflation in Pakistan Economics ReportДокумент15 страницInflation in Pakistan Economics ReportQanitaZakir75% (16)

- Monetary Policy Oxford India Short IntroductionsДокумент3 страницыMonetary Policy Oxford India Short IntroductionsPratik RaoОценок пока нет

- Benjamin C. Santos and Estrella, Remitio & Associates For Petitioner. Rodolfo V. Gumban For Private RespondentДокумент5 страницBenjamin C. Santos and Estrella, Remitio & Associates For Petitioner. Rodolfo V. Gumban For Private RespondentLouisa FerrarenОценок пока нет

- Basic Economic ProblemsДокумент146 страницBasic Economic ProblemsRichard DancelОценок пока нет

- Elements of Cost - Material Cost (PPT - 07) (Cut)Документ53 страницыElements of Cost - Material Cost (PPT - 07) (Cut)Jeevan Rajan67% (3)

- ECO 561 Final Exam AssignmentДокумент11 страницECO 561 Final Exam AssignmentRosie LeeОценок пока нет

- InfilationДокумент2 страницыInfilationDion MoonОценок пока нет

- MEBEДокумент12 страницMEBEAnant singhОценок пока нет

- Demand Pull InflationДокумент4 страницыDemand Pull InflationqashiiiОценок пока нет

- Determination of GDP in The Short RunДокумент38 страницDetermination of GDP in The Short Runhhhhhhhuuuuuyyuyyyyy0% (1)

- Alta 2017 AugustbnwДокумент25 страницAlta 2017 Augustbnw上古則言Оценок пока нет

- Eco Revision 22, 23 FebruaryДокумент2 страницыEco Revision 22, 23 FebruarysilОценок пока нет

- ECO202-Practice Test - 22 (CH 22)Документ4 страницыECO202-Practice Test - 22 (CH 22)Aly HoudrojОценок пока нет

- Assignment On Impact of Exchange Rate On Foreign TradeДокумент15 страницAssignment On Impact of Exchange Rate On Foreign TradeSheikh Munirul Hakim67% (3)

- Hacking CiphersДокумент47 страницHacking CiphersJay SagarОценок пока нет

- ReadingДокумент68 страницReadingariniОценок пока нет

- Is Government Spending Too Easy An AnswerДокумент11 страницIs Government Spending Too Easy An Answerfarik007Оценок пока нет

- Aky PDFДокумент38 страницAky PDFcharanОценок пока нет

- Issues in Indian Public Policies: Vinod B. Annigeri R. S. Deshpande Ravindra Dholakia EditorsДокумент239 страницIssues in Indian Public Policies: Vinod B. Annigeri R. S. Deshpande Ravindra Dholakia EditorsAKHILA B S100% (1)

- UK Current Account Deficit Widens to Record HighДокумент31 страницаUK Current Account Deficit Widens to Record Highmks93Оценок пока нет

- 8 Salient Features of Post Keynesian Compared To Neo ClassicalДокумент12 страниц8 Salient Features of Post Keynesian Compared To Neo ClassicalAnonymous hDMqlYpQbОценок пока нет

- Mankiw8e Student PPTs Chapter 1Документ12 страницMankiw8e Student PPTs Chapter 1karina2227Оценок пока нет

- Economyquestion For PCSДокумент12 страницEconomyquestion For PCSAshmit RoyОценок пока нет

- Comparison Between India and ChinaДокумент92 страницыComparison Between India and Chinaapi-3710029100% (3)

- Intermarket AnaДокумент7 страницIntermarket Anamanjunathaug3Оценок пока нет

- Glossary of key economic termsДокумент8 страницGlossary of key economic termsuzairОценок пока нет