Вам также может понравиться

- 1Q17 Financial StatementsДокумент31 страница1Q17 Financial StatementsJBS RIОценок пока нет

- Notice To The MarketДокумент1 страницаNotice To The MarketJBS RIОценок пока нет

- Minutes of The Board of Directors' Meeting Held On May 08, 2017Документ2 страницыMinutes of The Board of Directors' Meeting Held On May 08, 2017JBS RIОценок пока нет

- 1Q17 Conference Call TranscriptДокумент13 страниц1Q17 Conference Call TranscriptJBS RIОценок пока нет

- 1Q17 Earnings PresentationДокумент15 страниц1Q17 Earnings PresentationJBS RIОценок пока нет

- Notice To The MarketДокумент1 страницаNotice To The MarketJBS RIОценок пока нет

- JBS S.A. Announces The Conclusion of Plumrose AcquisitionДокумент1 страницаJBS S.A. Announces The Conclusion of Plumrose AcquisitionJBS RIОценок пока нет

- Minutes of The Board of Directors' Meeting Held On May 05, 2017Документ2 страницыMinutes of The Board of Directors' Meeting Held On May 05, 2017JBS RIОценок пока нет

- Release and FS 1Q17Документ53 страницыRelease and FS 1Q17JBS RIОценок пока нет

- JBS S.A. Releases Its 2016 Annual and Sustainability ReportДокумент1 страницаJBS S.A. Releases Its 2016 Annual and Sustainability ReportJBS RIОценок пока нет

- Minutes of The Fiscal Council's Meeting Held On May 04, 2017Документ2 страницыMinutes of The Fiscal Council's Meeting Held On May 04, 2017JBS RIОценок пока нет

- MgmtReport FSДокумент96 страницMgmtReport FSJBS RIОценок пока нет

- Notice To The MarketДокумент1 страницаNotice To The MarketJBS RIОценок пока нет

- JBS - Annual and Sustainability Report 2016Документ144 страницыJBS - Annual and Sustainability Report 2016JBS RIОценок пока нет

- 4Q16 Conference Call TranscriptДокумент16 страниц4Q16 Conference Call TranscriptJBS RIОценок пока нет

- JBS - ARCA - 2017 04 06 - Aprovao Reapresentao DFs 2015 e 2016 (JUCESP) EngДокумент5 страницJBS - ARCA - 2017 04 06 - Aprovao Reapresentao DFs 2015 e 2016 (JUCESP) EngJBS RIОценок пока нет

- Minutes of The Fiscal Council's Meeting Held On April 05, 2017Документ5 страницMinutes of The Fiscal Council's Meeting Held On April 05, 2017JBS RIОценок пока нет

- Minutes of The Board of Directors' Meeting Held On March 13, 2017Документ4 страницыMinutes of The Board of Directors' Meeting Held On March 13, 2017JBS RIОценок пока нет

- REMOTE VOTING FORM OF OESM To Be Held On April 28, 2017Документ5 страницREMOTE VOTING FORM OF OESM To Be Held On April 28, 2017JBS RIОценок пока нет

- MGMT Report FS 2015 (Reap 2017)Документ95 страницMGMT Report FS 2015 (Reap 2017)JBS RIОценок пока нет

- JBS - ARCF - 2017 03 10 - Aprovao DFs 4T2016 (Livro) MZT EngДокумент4 страницыJBS - ARCF - 2017 03 10 - Aprovao DFs 4T2016 (Livro) MZT EngJBS RIОценок пока нет

- Notice To The Market - Federal Police OperationДокумент1 страницаNotice To The Market - Federal Police OperationJBS RIОценок пока нет

- 4Q16 and 2016 Earnings PresentationДокумент21 страница4Q16 and 2016 Earnings PresentationJBS RIОценок пока нет

- MGMT Report FS 2016 (Reap 2017)Документ97 страницMGMT Report FS 2016 (Reap 2017)JBS RIОценок пока нет

- JBS Institutional Presentation Including 4Q16 and 2016 ResultsДокумент24 страницыJBS Institutional Presentation Including 4Q16 and 2016 ResultsJBS RIОценок пока нет

- MgmtReport FSДокумент96 страницMgmtReport FSJBS RIОценок пока нет

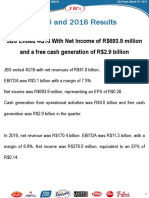

- 4Q16 and 2016 Earnings ReleaseДокумент31 страница4Q16 and 2016 Earnings ReleaseJBS RI100% (1)

- UntitledДокумент4 страницыUntitledJBS RIОценок пока нет

- MATERIAL FACT - JBS Announces The Acquisition of Plumrose USAДокумент2 страницыMATERIAL FACT - JBS Announces The Acquisition of Plumrose USAJBS RIОценок пока нет

- Minutes of The Board of Directors' Meeting Held On February 23, 2017Документ20 страницMinutes of The Board of Directors' Meeting Held On February 23, 2017JBS RIОценок пока нет

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (120)

- Workingcapitalmanagement-Lecture (Student)Документ19 страницWorkingcapitalmanagement-Lecture (Student)Christoper SalvinoОценок пока нет

- 16 - Y S Butola - Performance Improvement of The Distribution Segment A Case Study of NDPLДокумент25 страниц16 - Y S Butola - Performance Improvement of The Distribution Segment A Case Study of NDPLjeemitpsОценок пока нет

- Frieslandcampina Engro Pakistan Limited Financial Results - Quarter 1, 2020Документ3 страницыFrieslandcampina Engro Pakistan Limited Financial Results - Quarter 1, 2020Hassan KhanОценок пока нет

- Assignment On Pakistan EconomyДокумент14 страницAssignment On Pakistan EconomySabeen khalidi88% (8)

- Budget: The Fiscal Policy OverviewДокумент9 страницBudget: The Fiscal Policy OverviewDurga Rao0% (1)

- Barita Weekly Recap January 8 2016Документ3 страницыBarita Weekly Recap January 8 2016DKzОценок пока нет

- BBA 2nd SemesterДокумент14 страницBBA 2nd SemesterKunal SharmaОценок пока нет

- The Role of Sterilization Policy in Addressing The Impact of Public Expenditures in Iraq During The Period (2003-2017) Instructor: Naji Radees Abd Iraqi Parliament MemberДокумент17 страницThe Role of Sterilization Policy in Addressing The Impact of Public Expenditures in Iraq During The Period (2003-2017) Instructor: Naji Radees Abd Iraqi Parliament MemberLawa samanОценок пока нет

- Public Finance and Taxation (ch-1)Документ26 страницPublic Finance and Taxation (ch-1)yebegashet50% (2)

- Book Review The Ascent of MoneyДокумент6 страницBook Review The Ascent of MoneyshubhamОценок пока нет

- Case StudiesДокумент6 страницCase Studiesbhanu.chanduОценок пока нет

- 1984 Inflation: Israel's Stabilisation PlanДокумент6 страниц1984 Inflation: Israel's Stabilisation PlanRachit MurarkaОценок пока нет

- Indian Journal of Research Anvikshiki - EnglishДокумент63 страницыIndian Journal of Research Anvikshiki - EnglishHimani MittalОценок пока нет

- External Analysis: Industry Structure, Competitive Forces, and Strategic GroupsДокумент5 страницExternal Analysis: Industry Structure, Competitive Forces, and Strategic GroupsdoggaОценок пока нет

- An In-Depth Exp-WPS OfficeДокумент12 страницAn In-Depth Exp-WPS OfficePro cyclist AlicandoОценок пока нет

- Introductory MacroeconomicsДокумент2 страницыIntroductory Macroeconomics22ech040Оценок пока нет

- Shubhrakanti Nag: Financial Planning Report ForДокумент60 страницShubhrakanti Nag: Financial Planning Report ForRakesh IndianОценок пока нет

- Futa Post UtmeДокумент133 страницыFuta Post UtmeEAO TECHОценок пока нет

- b3 Economics and FinanceДокумент35 страницb3 Economics and FinanceAnonymous YkMptv9jОценок пока нет

- Etextbook 978 0132992282 MacroeconomicsДокумент61 страницаEtextbook 978 0132992282 Macroeconomicslee.ortiz429100% (49)

- Macroecon Mexam PDFДокумент24 страницыMacroecon Mexam PDFFredОценок пока нет

- Macro Economy and Construction Industry 3Документ7 страницMacro Economy and Construction Industry 3Syeda Aliza shahОценок пока нет

- Print: Unit Test 3Документ3 страницыPrint: Unit Test 3Rhita OuafiqОценок пока нет

- Managerial Economics Quiz 2Документ8 страницManagerial Economics Quiz 2Junayed AzizОценок пока нет

- EconomicGrowthinNepal MacroeconomicDeterminantsДокумент8 страницEconomicGrowthinNepal MacroeconomicDeterminantsratna hari prajapatiОценок пока нет

- MIL CPI IW July 2021 EДокумент1 страницаMIL CPI IW July 2021 EAmit BharambeОценок пока нет

- Long Term Construction Contracts - QuizДокумент10 страницLong Term Construction Contracts - QuizEliza BethОценок пока нет

- Fasanara Capital Investment Outlook - May 3rd 2016Документ17 страницFasanara Capital Investment Outlook - May 3rd 2016Zerohedge100% (1)

- Report TimkenДокумент45 страницReport TimkenVubon Minu50% (4)