Вам также может понравиться

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- Statement of FactsДокумент32 страницыStatement of FactsThe Ultra IndiaОценок пока нет

- QuezДокумент15 страницQuezKent Jerome Salem PanubaganОценок пока нет

- CFI 3 Statement Model Complete in ClassДокумент10 страницCFI 3 Statement Model Complete in ClassThiện NhânОценок пока нет

- Module 4 - Government AccountingДокумент14 страницModule 4 - Government AccountingJoanna TiuzenОценок пока нет

- IRCA Application Form 2015Документ7 страницIRCA Application Form 2015shaistaОценок пока нет

- Job SheetДокумент6 страницJob SheetRoy Sumugat100% (1)

- Minutes SampleДокумент2 страницыMinutes SampleKitty MeatiiОценок пока нет

- Technology and AuditДокумент75 страницTechnology and AuditSadaf MahfoozОценок пока нет

- Chapter 7 HW 7-4Документ6 страницChapter 7 HW 7-4GuinevereОценок пока нет

- Audited Financials 2022Документ159 страницAudited Financials 2022Anjelika ViescaОценок пока нет

- CH 4 Acc106Документ36 страницCH 4 Acc106Mas Ayu0% (1)

- Purchase OrdersДокумент9 страницPurchase OrderslulughoshОценок пока нет

- Ctolibas Ac550 Assignment1 Unit1Документ4 страницыCtolibas Ac550 Assignment1 Unit1May-AnnJoyRedoñaОценок пока нет

- Final UCB Report HRM340 PDFДокумент30 страницFinal UCB Report HRM340 PDFSazzad66Оценок пока нет

- The Companies (General Provisions and Forms) Rules, 1985 (As Amended Upto 30.5.16)Документ28 страницThe Companies (General Provisions and Forms) Rules, 1985 (As Amended Upto 30.5.16)Syed HunainОценок пока нет

- FEDO ProfileДокумент20 страницFEDO ProfileBinodh DanielОценок пока нет

- Requirements in Renewing Business PermitДокумент1 страницаRequirements in Renewing Business PermitCharina Marie CaduaОценок пока нет

- Engro-Polymer-Chemicals 2021 ReportДокумент197 страницEngro-Polymer-Chemicals 2021 ReportUmer FarooqОценок пока нет

- Annexure A Physical Verification Report 2020Документ11 страницAnnexure A Physical Verification Report 2020Md SobujОценок пока нет

- PrE 4 - AUDIT OF THE GAS, PETROLEUM, AND OIL SECTORS (Outline)Документ12 страницPrE 4 - AUDIT OF THE GAS, PETROLEUM, AND OIL SECTORS (Outline)nefael lanciolaОценок пока нет

- Ias 8 PDFДокумент21 страницаIas 8 PDFJoedy Mae MangampoОценок пока нет

- Long Form Audit ReportДокумент34 страницыLong Form Audit ReportAshish SaxenaОценок пока нет

- Auditing Problems Test Banks - SHE Part 1Документ5 страницAuditing Problems Test Banks - SHE Part 1Alliah Mae ArbastoОценок пока нет

- LP - Acctg - 19 - 1stsem - 2019-2020Документ16 страницLP - Acctg - 19 - 1stsem - 2019-2020Rolly BaniquedОценок пока нет

- Auditing: T I C A PДокумент3 страницыAuditing: T I C A Psecret studentОценок пока нет

- PDF Resa Ap Quiz 5b43 - Compress PDFДокумент42 страницыPDF Resa Ap Quiz 5b43 - Compress PDFVianney Claire RabeОценок пока нет

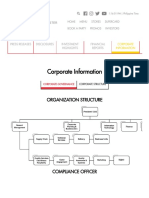

- Corporate Information: Organization StructureДокумент11 страницCorporate Information: Organization StructureKang ChulОценок пока нет

- Control Risk Self Assessment ToolДокумент36 страницControl Risk Self Assessment ToolMbuthiac Mbuthiac33% (3)

- Final Report WAPDAДокумент39 страницFinal Report WAPDArizi4me9197100% (1)

- Course Description - Institute of Business ManagementДокумент40 страницCourse Description - Institute of Business ManagementHaseeb Nasir SheikhОценок пока нет