The infuence of the London Overground network on

economic growth and prosperity

Research for Spatial Planning

1

Contents

Introduction 2

Growth of the Overground 2

The Impact of the Overground 4

Conclusion 6

Glossary 7

Bibliography 8

Appendices 9

2

Introduction

With London Overground network just over four years old it is possible to look back over the

infant years of the network and attempt to assess its impacts on London. The growth of the

network has been rapid, with lines proliferating around north London from Richmond and

Clapham Junction in the west to Crystal Palace and West Croydon in the East, with the full

circle connection around London from Surrey Quays to Clapham Junction south of the Thames

under construction and due for completion in 2012.

The London Overground network that exists today is a combination of existing lines transferred

into TfL operation (with varying degrees of increased service levels) as well as the newly constructed

East London Line extension (henceforth ELLX) from Highbury & Islington to Whitechapel in the

north via the former East London underground line to New Cross Gate, Crystal Palace and

West Croydon in the south.

1

Because of its varied origins there are varying levels to which the

development of the network has changed the landscape of transportation along its route.

At a general scale in recent years the East London property market has been heavily infuenced

by the Olympics development, however a 2010 report by LloydsTSB shows that of the 14 nearest

Olympic postal districts only 4 have exceeded the Greater London average price increase since

the Olympics were announced

2

. These four postal districts were Homerton, Shoreditch, Dalston

and Clapton, with Homerton and Shoreditch signifcantly higher than the other districts. It is

perhaps no surprise that these are the two districts most heavily infuenced by the ELLX, with

Dalston also seeing a large beneft with the new terminus station at Dalston Junction.

Whilst these fgures show the overall trend they may also start to hint at the varying infuence

the different parts of the Overground, whether for example the ELLX as a new line has had more

signifcant impact than the places where the route merely improved and re-branded an existing

service, or whether increased services, the Overground branding and its inclusion on the tube

map have lead to as big a change in areas where a service already existed as where it did not.

This essay will attempt to look at a number of different stations on the Overground network and

look at the change in value of the housing stock directly around them in the period before and

after the opening of the Overground network. By utilising data for the council tax banding of

the housing stock by output area, it should be possible to see not only the growth in volume of

the housing stock as a result of the Overground but also any shift in breakdown towards higher

value properties. A signifcant growth in volume of the housing stock would indicate that the

area has seen signifcant growth in population as a result of the rail links. At the same time the

percentage breakdown of the housing stock may show a trend towards higher value properties

at the expense of more affordable ones, indicating perhaps gentrifcation is on its way and also a

potential for pricing some of the existing population out of the market.

Growth of the Overground

With the different elements of the Overground network it is relevant to give a brief synopsis of

the events leading to its creation in order to see the extent to which services changed before and

after the TfL takeover.

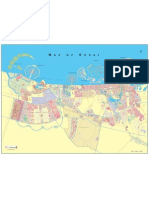

1 Appendix 1: Overground Map showing current lines and southern extension to Clapham Junction

2 Appendix 3: LloydsTSB survey

3

The Overground network we have today was created from the remnants of a number of partial

radial rail routes created in the late 19th and early 20th centuries by independent train companies

in the wake of the successful inner circle underground railway. Unfortunately though the inner

circle line (the Circle Line on the underground today) was successful, the outer routes never

really became proftable, London was much smaller then than now and there simply werent the

passenger numbers to support the routes.

Over the years the radial routes were cut back, though by the time British Rail was privatised a

number of radial routes still existed. The most London centric of the new franchises created as a

result of the privatisation of British Rail was the North London franchise operated by Silverlink

whose services were as follows:

London Euston to Birmingham New Street (stopping services via Northampton)

Bletchley to Bedford

Watford Junction to St Albans

London Euston to Watford Junction

Richmond to North Woolwich (via Stratford)

Clapham Junction to Willesdon Junction

The franchise operated the long distance services as Silverlink County and the London services

as Silverlink Metro.

Though the Silverlink franchise was recorded as having PPM fgures in excess of 83% in Q3 2005

(up from 77.7% the previous year)

3

, which on paper made it one of the most reliable railways

in the south east, it was seen by passengers as Shabby, unreliable, unsafe, overcrowded

4

.

Following changes made in the Railways Act 2005 (as a result a government review in July 2004

5

and proposals by TfL for a London Regional Rail Authority

6

) it became possible for TfL to have an

infuence over the London rail network in a way that was previously handled at a national level.

The result of this was that in February 2006 it was announced that the Silverlink Franchise

would be split, with the longer distance routes transferring to another franchise and the London

routes transferring into to TfL control. In September 2006 the London Overground branding

was unveiled and it was announced that the ELLX (which already had some preparatory work

underway) would also form part of this new transport network.

On 11 November 2007 the WLL, NLL, GOBLIN and Watford-Euston DC lines transferred into

TfL control under the branding of London Overground. Oystercards were immediately accepted

on all routes, service levels were increased and a deep cleaning and renewal programme began,

alongside a re-branding and marketing campaign.

The ELLX itself fnally opened in April 2010 between Dalston Junction and New Cross/New

Cross Gate with the southern extensions to Crystal Palace & West Croydon opened the following

month. Subsequently in February 2011 the western curve north of Dalston Junction opened,

taking the line to its present Northern terminus of Highbury & Islington, running alongside the

NLL route to Stratford via Dalston Kingsland.

2012 should see the opening of the Inner South London Line, creating a southern route to

Clapham Junction and achieving a full orbital rail network

7

.

3 Network Rail (2005), Cross London Route Utilization Strategy, pp.26-27,

4 Greater London Authority (2006), Londons Forgotten Railway, p.2, March.

5 Department for Transport (2004), The Future of Rail, White Paper, Cm 6233, July.

6 TfL (2004). Bob Kiley outlines proposals for London Regional Rail Authority. Press release, issued 23 March 2004.

7 Appendix 1: Overground Map showing current lines and southern extension to Clapham Junction

4

The Impact of The Overground

Methodology

The Overground network has rapidly grown since its creation in 2007 to now serve 78 stations

(this will rise to 83 following the opening of the Inner South London Line), with a view to looking

at the impacts the network has had on East London, and specifcally the A10 corridor a number

of stations were chosen to focus upon. As mentioned above the Overground has grown from a

varied mix of existing infrastructure so it was important to select stations that represent this

varied ancestry. With the focus on the A10 corridor the completely new ELLX stations from

Whitechapel to Dalston Junction were critical, so all have been investigated. The A10 corridor

also cuts through the two other Overground routes in East London (NLL and GOBLIN) providing a

number of stations to focus upon. In addition to the Overground network some rail stations that

are not part of the Overground have been chosen to act as a control to compare the Overground

network stations against. The full list of stations chosen are as follows:

Cannonbury (NLL & ELLX, formerly Silverlink)

Dalston Junction (ELLX, new station)

Dalston Kingsland (NLL, formerly Silverlink)

Hackney Central (NLL, formerly Silverlink)

Haggerston (ELLX, new station)

Highbury & Islington (NLL, ELLX and Victoria Line, formerly Silverlink & Victoria Line)

Hoxton (ELLX, new station)

Rectory Road (East Anglia - non-Overground)

Shoreditch High Street (ELLX, new station)

South Tottenham (GOBLIN, formerly Silverlink)

Stamford Hill (East Anglia - non-Overground)

Stoke Newington (East Anglia - non-Overground)

Whitechapel (ELLX, H&C and District Lines, formerly part of the old East London Line)

The initial source of data for each of the stations above was Council Tax Banding data produced

by the VOA annually since 2001

8

. The council tax banding data is available for every property

in an output area regardless of whether it has been sold or not, this allows it to give more area

specifc information than is possible by using house sale prices which may have only one or two

sales in a small area making conclusions hard to draw. The data isnt without limitations that

will be covered later

9

but act as a reasonable indicator of the state of the property market in the

specifc area of a station.

The Council Tax Banding data for each station has been combined into summary sheets and

attached as Appendix 4.

Analysis

The data shows quite clearly that the ELLX has had a signifcant impact on the areas around the

new stations, all of the new stations on the route show clear jumps in the number of properties

since the Overground was announced, these increases in general have a particular focus on the

C & D bands. The speed of the increase varies from Dalston Junction which shows an extremely

sharp rise in 2010 to Shoreditch High Street that has the largest growth in 2005 & 2006 but has

8 Appendix 4A: Council Tax Banding data set information

9 Appendix 4, summary sheet

5

continued to grow steadily since. Part of the reason for the two types of growth is likely related to

the type of development that has (and still is) taking place around the stations. Dalston Junction

has been the site of major construction work, the lead time of which would inevitably be quite

long, resulting in apartments only coming to market in 2010. The data also shows that the

southern stations (Shoreditch High Street & Hoxton) have shown a steady continuous growth

since 2006 whilst Dalston Junction and Haggerston further north have had larger more abrupt

rises indicative perhaps of fewer larger developments compared with numerous smaller projects

in the Shoreditch and Hoxton areas.

In looking at the top banding with properties in each of the station areas it is possible to make a

judgement into gentrifcation in the different areas, Dalston for example shows a growth in Band

E dwellings from 0% to 13% in 2010, this would seem to ft well with the new developments in

the area.

For stations elsewhere on the Overground network the change to Overground has had mixed

impacts, Highbury & Islington saw a signifcant jump in Band E properties in 2010 from 26% to

42% of the housing stock, a physical increase of 67 dwellings. Dalston Kingsland has also seen

a steady rise in housing volumes (though the distribution has remained relatively consistent),

the data shows a small jump in 2004 (a 31% increase in dwellings) and again a smaller one

in 2010 (10% increase). Highbury & Islington and Dalston Kingsland however seem to be the

exceptions for existing stations, with areas such as Cannonbury and Hackney Central showing

little signifcant change in the housing stock as a result of the Overground. The non-Overground

stations investigated show a similar steady distribution, though Stoke Newington has seen a

small but steady growth over the 10 year period it would seem this is more indicative of the area

in general being on the rise rather than anything else.

The two jumps that are seen in the Dalston Kingsland data might well be linked to the ELLX as

the station is extremely close to Dalston Junction and its associated development. Some spill

over into the neighbouring areas would seem likely considering the scale of development around

Dalston Junction. At Highbury and Islington the 2010 jump would seem to tie in with the timing

of the ELLX extension that opened early in 2011.

Other Data

Alongside the council tax data it is important to look at the actual usage of the Overground

network both before and after TfL control. Station passenger number data is available for all

national rail stations annually.

10

Whilst TfL publish fgures for London Underground stations,

they do not do so for the Overground, as a result none of the Stations on the ELLX or the former

ELL are available within this data set, just the stations that were previously served by national

rail. There are some also variations in the data collection over the years, particularly with regard

to Oyster PAYG users not being counted until 2009/10 when coverage became universal.

Whilst the data may not be perfect it does show passenger entries and exits increasing sharply

following the Overground takeover followed by a decrease, this decrease is due to the increased

use of Oyster PAYG following its blanket acceptance on the Overground. In comparison the non-

Overground stations show steady growth without the sharp rise seen at the Overground stations.

Stoke Newington again shows a growth pattern slightly more in tune with the Overground

stations than the non-Overground ones, this could as in the case of the council tax data be

attributed to an area becoming increasingly popular. Though there are no individual station

data, the Overground as a whole has far exceeded estimates by TfL

11

with the ELLX particularly

being successful.

10 The data is collated by Delta Rail for the Ofce for Rail Regulation

11 TfL, Rail and Underground Panel. (2011). London Overground Impact Study. 16 November 2011.

6

Conclusions

Whilst the effect of the ELLX can be seen from the Council Tax Banding data it is hard to

discern any consistent change elsewhere. It could be that it was obvious that the new rail line

would increase demand in the areas it served and the areas where a service already existed

the improvement was not so obvious, leading to less property speculation and development. It

would be interesting to go back to the same data set in a couple of years to see if now that the

Overground has settled in and become the runaway success that it has, whether it will act as a

driver for development in areas that were previously served by existing rail lines. Looking at the

station usage fgures

12

and the Overground usage as a whole

13

shows that local residents are

using it in signifcant numbers. The 2011 census data will provide information on travelling to

work, I would expect, given the Overground data, to see many more people using this to travel

to work and quite possibly travelling further afeld for work. Leading on from this I would expect

the Overground to have impacted on worklessness in the areas, though the effects of the 2008

recession have had such a large global effect it is hard to discern at this point the true impacts

of The Overground on employment.

The lower impact of the Overground where existing services have been improved would seem to

attract signifcantly less of the large scale development seen along the ELLX, yet the increased

passenger numbers show there has been signifcant improvement for local residents. Assuming

as mentioned above that development and investment will follow The Overground, albeit at a

slower pace than the ELLX it would seem to suggest that The Overground will provide signifcant

economic gains at a pace that does not displace the existing residents.

Looking to the future and TfLs aspirations for The Overground

14

it wouldnt be surprising to see

more of the Lea Valley Lines (namely the Southbury loop to Enfeld Town and Cheshunt and the

Chingford Line) under Overground control in future years. The Upper Lea Valley Opportunity

Area Planning Framework (ULV OAPF) highlights the A10/A1010 corridor as a key growth areas,

the Southbury loop serves this linear growth area far better than the busy mainline to the east

(which is the focus of proposed infrastructure improvements). If these services under Overground

control saw the same increase in passengers it could help achieve the growth desired in the

ULV OAPF. Additionally minor track works west of South Tottenham could enable trains to run

from Stratford to Enfeld Town linking the Upper Lea Valley quickly and directly with the large

developments in Stratford.

12 Appendix 5

13 TfL, Rail and Underground Panel. (2011). London Overground Impact Study. Figure 3. Growth in LO Demand.

14 TfL, Rail and Underground Panel. (2011). Tfs Recommendations For The High Level Output Specifcation For 2014 2019 (HLOS2), 12 July 2011

7

ELL

East London Line (London Underground Line, extended with the ELLX to become part of the

Overground)

ELLX

East London Line Extension (See ELL)

GOBLIN

Gospel Oak to Barking Line (Former Silverlink line that became part of the London Overground

network)

NLL

North London Line (Former Silverlink line that became part of the London Overground network)

PPM

Public Performance Measure (Operational effciency score determined by the SRA)

SRA

Strategic Rail Authority

WLL

West London Line (Former Silverlink line that became part of the London Overground network)

Glossary

8

Haswell A. (2010). New report shows mixed picture for house prices despite promise of Olympics

boom. Available from: http://www.eastlondonlines.co.uk/2010/08/mixed-picture-for-house-

prices-despite-olympic-promises/. [Accessed: 10/01/2012].

Headicar, P. (2009). Transport policy and planning in Great Britain. London, Routledge.

Offce for National Statistics. Available from: http://neighbourhood.statistics.gov.uk/

dissemination/LeadHome.do;jessionid=lNSGPMnbsJvTrwTzB9phQHGcB3xKQlBlhKG0HzCn32

RlxJDL1PBZ!-1055568020!1326198491704?m=0&s=1326198491704&enc=1&nsjs=true&nsck

=true&nssvg=false&nswid=1680. [Accessed: 28/12/2011].

Offce for Rail Regulation. (2011). Station usage. Available from: http://www.rail-reg.gov.uk/

server/show/nav.1529. [Accessed: 10/01/2012].

Transport for London. (2004). Bob Kiley outlines proposals for London Regional Rail Authority.

Available from: http://www.tf.gov.uk/static/corporate/media/newscentre/archive/4359.html.

[Accessed: 10/01/2012].

Valuation Offce Agency. How your home is banded. Available from: http://www.voa.gov.uk/

corporate/CouncilTax/howYourHomeIsbanded.html. [Accessed: 10/01/2012].

Bibliography

9

Appendix 1 10

London Overground Geographic Map

Appendix 2 12

TfL Rail & Underground Group Report: The Impacts of the London Overground

Appendix 3 34

LloydsTSB Olympic Housing report

Appendix 4 37

Dwelling Stock by Council Tax Band (2001-2011)

Appendix 5 58

National Rail Passenger Usage Figures

Appendices

A

p

p

e

n

d

i

x

1

10

Appendix 1

Current London Overground Geographic Network Map

And Inner South London Line Opening 2012

HERTFORDSHI RE

HI LLI NGDON

WESTMI NSTER

TOWER

HAMLETS

BARKI NG &

DAGENHAM

BARNET

I SLI NGTON

WALTHAM

FOREST

LAMBETH

GREENWI CH

H

A

M

M

E

R

S

M

I

T

H

&

F

U

L

H

A

M

KENSI NGTON

& CHELSEA

HARROW

RI CHMOND

UPON

THAMES

REDBRI DGE

MERTON

BEXLEY

SOUTHWARK

CI TY OF

LONDON

KI NGSTON

UPON

THAMES

EALI NG

BROMLEY

HOUNSLOW

WANDSWORTH

LEWI SHAM

CROYDON

BRENT

HARI NGEY

CAMDEN

HACKNEY

NEWHAM

ENFI ELD

ESSEX

River Thames

River Thames

Harrow & Wealdstone

Watford Junction

Bushey

Carpenders Park

Hatch End

Headstone Lane

Watford High Street

Kenton

North Wembley

South Kenton

Wembley Central

Shadwell

Whitechapel

Wapping

Rotherhithe

Blackhorse

Road

Gospel

Oak

South

Hampstead

Highbury &

Islington

Stratford

Willesden Junction

Harlesden

Queens Park

Stonebridge Park

Gunnersbury

Shepherds Bush

Kensington (Olympia)

West Brompton

Wandsworth Road

Kew

Gardens

Richmond

New

Cross

Gate

Surrey Quays

New

Cross

Canada Water

West Hampstead

Shoreditch

High Street

Hoxton

Haggerston

Dalston

Junction

Homerton

Hackney

Wick

Hackney

Central

Dalston

Kingsland Canonbury

Imperial Wharf

Kilburn High Road

Leyton Midland Road

South

Tottenham

Harringay Green Lanes

Crouch Hill

Upper Holloway

Hampstead

Heath

Finchley Road & Frognal

Kentish

Town West Camden

Road

Caledonian

Road &

Barnsbury

Euston

Barking

Wanstead Park

Woodgrange

Park

Leytonstone High Road

Kensal Green

Kensal Rise

Brondesbury Park

Brondesbury

South Acton

Acton Central

Clapham Junction

Clapham

High Street

Denmark Hill

Peckham

Rye

Queens Road

Peckham

Brockley

Honor Oak Park

Crystal Palace

West Croydon

Norwood Junction

Penge West

Anerley

Sydenham

Forest Hill

Walthamstow

Queens Road

Key

Tramlink

Interchange stations

Step-free access fromstreet

to train

National Rail

London Underground

London Overground

DLR

Step-free access fromstreet

to platform

MAYOR OF LONDON Transport for London

London Overground Geographic Map August 2011

London Overground geographic map

A

p

p

e

n

d

i

x

1

11

A

p

p

e

n

d

i

x

2

12

Appendix 2

London Overground Impact Study

A

p

p

e

n

d

i

x

2

13

1

AGENDA ITEM 5

TRANSPORT FOR LONDON

RAIL AND UNDERGROUND PANEL

SUBJECT: LONDON OVERGROUND IMPACT STUDY

DATE: 16 NOVEMBER 2011

1 PURPOSE AND DECISION REQUIRED

1.1 The purpose of this paper is to advise the Panel of the results of TfLs analysis

of demand patterns on the London Overground network and to highlight the

fact that rapid demand growth has led to increasing levels of crowding on the

network despite investment in new capacity. This is attached to the paper as

Appendix 1

1.2 The paper is written in two parts. The first part looks at the network that

transferred to TfL in 2007 and explains the growth in demand on that network.

The second part looks at the extended East London Line and its impact on

transport in London.

1.3 The Panel is asked to note the paper and appendix.

2 BACKGROUND

2.1 TfL took over the concession to operate the London Overground in November

2007. Since then it has transformed the network from a neglected railway into

the best performing train operator in Great Britain. This has been achieved

through a major infrastructure upgrade to deliver increased train frequency,

new trains, station enhancements and service quality improvements.

2.2 The extended East London Line was opened in May 2010 with new trains and

new and refurbished stations. It was further extended to Highbury & Islington

in February 2011 and now forms an integrated part of the London Overground

network.

2.3 Passenger demand on London Overground increased from 0.6 million

journeys per week in 2007 to almost two million journeys in September 2011.

In July 2011, the Panel asked for an explanation of recent growth on the North

and West London Lines. The attached report reviews demand trends on the

London Overground network and the impact of the East London Line one year

after opening.

3 LONDON OVERGROUND IMPACTS

3.1 London Overground passenger volumes are now two and a half times the

level when TfL took over management of the concession. The opening of the

extended East London Line has contributed a large part of the growth but the

existing Overground network also experienced an increase in demand of 80

per cent.

A

p

p

e

n

d

i

x

2

14

2

3.2 Economic and demographic factors, fares and service levels are key drivers of

rail demand and demand would normally be flat during an economic downturn.

However, London and South East rail demand has grown strongly over the

last two years despite the lack of growth in the economy and this forms the

background to strong London Overground demand growth. The other main

drivers of growth on the London Overground network are service frequency;

operational performance; service quality including stations and rolling stock,

connectivity and marketing. These factors contributed to extremely strong

growth in demand during 2010/11 even without East London Line opening.

3.3 0.6 million passengers per week use East London Line. Demand on the route

is in line with forecasts despite the poor economic situation and peak services

are already crowded from the south of the route in to Canada Water.

3.4 Operational performance is excellent and customer satisfaction on London

Overground is now rated very good at 82 out of 100.

4 CONCLUSION AND NEXT STEPS

4.1 Enhancements to the London Overground network resulted in a dramatic

increase in passenger demand in 2009/10 and 2010/11. Demand continues to

grow with the full effects of the infrastructure upgrade still to impact fully.

Crowding is already a concern on part of the West London, East London and

Gospel Oak Barking routes and, as no further capacity enhancements are

planned, this is likely to become an increasing problem.

4.2 TfLs report Delivering the Mayors Transport Strategy: National Rail in London

sets out the case for enhancement in capacity on the routes including train

lengthening on North and West London Lines, East London Line and Gospel

Oak Barking route and additional peak services where feasible. The

recommendations are reflected in Network Rails London and South East

Route Utilisation Strategy and the Initial Industry Plan.

5 RECOMMENDATION

5.1 The Panel is asked to NOTE the paper and appendix.

6 CONTACT

6.1 Contact: Howard Smith, Chief Operating Officer, London Rail

Number: 020 7918 3453

Email: HowardSmith@tfl.gov.uk

A

p

p

e

n

d

i

x

2

15

APPENDIX 1

London Overground Impact Study

Part 1 Existing London Overground network

1 Introduction

1.1 TfL took over the management of the London Overground (LO) concession

(formerly Silverlink Metro services) in November 2007. Services at the time

were of low quality with old rolling stock, neglected stations and low levels of

customer service. Since taking over the network, TfL has made significant

enhancements to the level and quality of services through a programme of

introducing new rolling stock, upgrading infrastructure to deliver more frequent

services, refurbishing stations and delivering higher standards of customer

service. The extended East London Line was opened in May 2010 and a

further phase to run services from Dalston Junction to Clapham Junction will

be completed in 2012 completing the orbital network.

1.2 This paper describes the changes that have taken place and the impact of

those changes on demand and customer satisfaction.

2 Background

2.1 TfL manages the operation of services on the LO under a seven year

concession. Unlike a standard franchise, TfL takes revenue risk on LO

services and works closely with the concessionaire, LOROL to manage

service quality and performance.

2.2 At the time of takeover, LO operated up to six peak trains per hour between

Stratford and Richmond and three peak trains per hour between Willesden

and Clapham. In the off peak, frequencies were lower at four trains per hour

between Stratford and Richmond and two trains per hour between Clapham

and Willesden. The timetable was improved in 2010 to provide three Stratford-

Clapham trains per peak hour serving the increasingly popular Willesden

Clapham section of route, and three trains per hour from Stratford to

Richmond. This improved performance and helped generate additional

demand.

2.3 A major infrastructure upgrade project led to the introduction of the May 2011

timetable which enables provision of four trains per hour from Stratford to

Richmond and four trains per hour from Stratford to Willesden. This timetable

has resulted in a further increase in demand as all parts of the route have a

turn up and go service and the central section benefits from eight peak trains

per hour.

2.4 Gospel Oak Barking services had a service frequency of two trains per hour

when TfL took over the concession. Frequency has now increased to four

trains per hour on the route with extra early morning services and an

additional peak train has recently been introduced.

A

p

p

e

n

d

i

x

2

16

Figure 1: Frequency of peak LO services

2.5 LO provides both radial routes into central London on the Watford Euston

route and orbital services around London allowing passengers to make local

journeys or to travel without interchanges in central London. It serves locations

which have historically been poorly served by public transport.

2.6 In 2007, Silverlink Metro carried 0.6 million passengers per week. That figure

has now increased to 1.2 million, excluding East London Line services which

add a further 0.6 million journeys. In 2011/12, a total of 100m journeys are

expected to be made on LO services.

3 Capacity

3.1 LO services are increasingly becoming crowded despite increased capacity

from new and longer trains and higher frequency as more passengers are

attracted to the improved services. The busiest parts of the network in the

morning peak are between Clapham Junction and Shepherds Bush, Barking

and Blackhorse Road and Sydenham and Canada Water.

3.2 Figure 2 shows forecast crowding on the Overground network in 2016 where

black and purple lines show demand exceeding TfLs planning standard of

three passengers per square metre standing in the morning peak. TfL is

looking at options for relieving crowding.

2

A

p

p

e

n

d

i

x

2

17

Figure 2: Forecast crowding in 2016

3.3 Most LO routes are served by new four-car Class 378 trains with longitudinal

seating and high capacity layout. Trains have capacity of 700 and are

designed to carry large numbers of passengers comfortably over relatively

short distances. Walk-through carriages and wide doors ease passenger flow

onto and through the train. The new trains are popular with passengers as

reflected in high customer satisfaction scores for train attributes. Trains were

introduced in three-car formation first on North and West London Lines and

extended to four cars in 2010. They represent a 33 per cent increase in

capacity compared with the old rolling stock. On Watford Euston services,

class 378s were introduced as four car trains.

3

A

p

p

e

n

d

i

x

2

18

3.4 On the Gospel Oak Barking line, new two-car class 172 trains were introduced

in 2010 with capacity of up to 400 people per train, a third higher than the

original rolling stock. Demand for Gospel Oak Barking services has

increased rapidly and services are crowded.

4 Stations

4.1 TfL has undertaken a major programme of refurbishment at stations along the

Overground network. It manages most of the stations it serves and has a

policy of staffing stations to ensure that staff are visible and available to help

passengers, improving personal security.

4.2 Passenger facilities at stations have been improved with the installation of

ticket machines, help points, cycle parking and passenger information. Eleven

stations were gated shortly after the concession started to reduce fraudulent

travel and to improve security and over 95 per cent journeys pass through a

gated station at one or both ends. The volume of passenger journeys made

without valid tickets fell from 10 per cent to three per cent within a year of the

network being under TfL management. The volume of passenger journeys

made without a valid ticket is currently two per cent.

4.3 Two new stations were opened on the Clapham to Willesden route.

Shepherds Bush station was opened in 2008 to serve the new Westfield

shopping centre and to provide interchange with the Central Line; and Imperial

Wharf was opened in 2009. This section of line has been the fastest growing

part of the network with increasing peak loads despite an increase in capacity.

5 Operational Performance

5.1 LO performance across all routes has increased dramatically from PPM

(Public Performance Measure) of 91 per cent at the time TfL took over the

concession to the current level of 95 per cent. PPM measures the percentage

of trains arriving within five minutes of scheduled time. This is the highest

performance level of all train operators and represents a turnaround from

below average to excellent performance which is exceptional on a mixed use

railway.

6 Fares

6.1 Oyster Pay as You Go was introduced on LO in 2007 making travel easier and

cheaper. The product gained popularity and now accounts for almost 40 per

cent of journeys on LO. PAYG was rolled out to National Rail services in

London in January 2010, allowing passengers to make through journeys on

LO and other National Rail operators services such as South West Trains

services with an interchange at Clapham Junction. Through ticketing for

Overground and London Underground (LU) means that a fully integrated

journey can be made for no extra cost.

6.2 Euston and Shoreditch High Street are the only LO stations in Zone 1.

Passengers are able to reach a range of destinations without travelling into

Zone 1 and pay lower fares than people travelling via central London.

4

A

p

p

e

n

d

i

x

2

19

Use of the route

7 Passenger numbers

7.1 160 million passengers have used LO since its opening. Figure 2 shows

growth in demand since 2007/08 compared with growth on other TfL services

and London and South East National Rail services.

Figure 3: Growth in LO demand

7.2 LO growth has been consistently higher than that on other services but a step

change took place in 2010/11. Passenger volumes are two and a half times

the level when TfL took over services. Excluding the East London Line,

demand has increased by over 80 per cent.

7.3 Since 2009, demand on the existing Overground network (North and West

London Lines, Gospel Oak Barking and Watford Euston) has increased by 1.5

million journeys per four week period. The main drivers of rail demand are

economic factors, service quality and performance and fares. The impact of

these drivers on demand has been calculated using industry elasticities where

possible to generate a waterfall chart of demand drivers (figure 4).

7.4 Despite the recent downturn in the economy, rail demand in London and the

South East has remained buoyant and LO has benefitted from that growth.

However, background growth only accounts for a quarter of the growth

experienced. Between 2009 and 2011, service frequency was the largest

contributor to demand. Service quality was another significant driver. New

trains, higher capacity, station upgrades and performance improvements all

contributed to better service quality. Connectivity was another important factor

5

A

p

p

e

n

d

i

x

2

20

with the ending of a long programme of engineering works which had

disrupted travel, especially at weekends, and the opening of the East London

Line enabling orbital journeys to be made between north, east and south

London.

7.5 Other factors such as marketing also contributed to demand and this was

most apparent around the time of the East London Line opening when

demand on the rest of the LO network increased by more than the growth in

interchanging passengers.

Figure 4: Drivers of Overground Growth

8 Journey purpose

8.1 LO has a high proportion of regular passengers. 61 per cent of passengers on

the route are using it to travel to or from work and the breakdown of journey

purposes is shown in Figure 5. The Watford Euston Line serves employment

centres in central London with interchange at Queens Park or Euston. The

orbital routes serve central London via interchanges at key locations such as

Blackhorse Road, Highbury & Islington and Shepherds Bush as well as

serving Docklands via an interchange at Stratford. In addition, Stratford and

other locations along the routes are employment centres in their own right.

8.2 LO has a higher proportion of educational travel than most rail operators with

schoolchildren using the routes and five per cent of passengers travelling to or

from education. This means the evening peak period is extended with high

volumes of travel in the late afternoon.

8.3 Average journey length is relatively short at 7kms, reflecting the metro style

nature of the service.

6

A

p

p

e

n

d

i

x

2

21

Figure 5: LO journey purpose

9 Integration

9.1 20 per cent of LO passengers interchange with Underground or Docklands

Light Railway (DLR) and a further 20 per cent use bus and Overground. This

compares with 50 per cent of National Rail passengers arriving in London in

the morning peak who use Underground or DLR for their onward journey.

9.2 TfL has estimated that, of the increase in passengers using LO since 2007,

the largest share have switched from bus or LU helping to reduce congestion

on radial routes into Central London. Around 12 per cent have switched from

car or are making new journeys.

Figure 6: Modes previously used by additional LO passengers

7

A

p

p

e

n

d

i

x

2

22

10 Customer satisfaction

10.1 Current performance following TfLs investment has delivered an overall

customer satisfaction rating on LO of 82 out of 100, with particularly high

scores for train and service level attributes. This compares with a rating of 71

out of 100 in 2007 and reflects the step change in quality that has taken place.

A satisfaction rating of over 80 means the perception of service quality is very

good.

Figure 7: LO Customer Satisfaction

10.2 The National Passenger Survey undertaken by Passenger Focus compares

satisfaction with train operators performance on a consistent basis. During its

last year of operation, Silverlink Metro scored 71 per cent for overall

satisfaction under this survey. In contrast LO scored 89 per cent for overall

satisfaction under the most recent National Passenger Survey conducted

during Spring 2011, demonstrating the impact of the improvements delivered

by TfL.

11 Equality and inclusion

11.1 LO has improved accessibility to public transport through works to implement

step free access. Step free access from street to platform is available at 44

per cent of stations, and trains are designed to be accessible. This compares

with 22 per cent of LU stations and 31 per cent of National Rail stations in

London which are step free from street to platform. The new LO trains have

accessibility features such as on board audio and visual train running

information, wider doors for improved accessibility and more grab rails and

handles Staff are trained to assist people using wheelchairs. Eight per cent of

passengers surveyed have a long term mental or physical disability and one

per cent passengers are wheelchair users.

8

A

p

p

e

n

d

i

x

2

23

12 Conclusions on the existing LO network

12.1 Enhancements to the existing Overground network including better

management and service quality resulted in a dramatic increase in passenger

demand in 2009/10 and 2010/11. Demand continues to grow with the full

effects of the 2011 North London Railway Infrastructure Project (NLRIP)

timetable still to be reflected in demand. Peak crowding is a concern on part

of the West London and North London Lines and Gospel Oak Barking routes

and, as no further capacity enhancements are planned, this is likely to become

an increasing problem.

12.2 TfLs report Delivering the Mayors Transport Strategy: National Rail in London

sets out the case for enhancement in capacity on the routes including train

lengthening on Gospel Oak Barking and North and West London Lines and

additional peak services where feasible. The recommendations are reflected

in Network Rails London and South East Route Utilisation Strategy.

12.3 TfL continues to monitor demand patterns on LO for management reporting

and results are published in Travel in London.

9

A

p

p

e

n

d

i

x

2

24

Part 2 East London line one year after opening

1 Background

1.1 The extended East London Line carries 0.6 million passengers per week, 3.5

times as many as the old East London Line that it replaced and more than

double the volume of usage in June 2010. Passenger revenue has also

doubled and is forecast to be 32m in 2011/12. This report describes the key

impacts of the extended line on passengers and on London.

1.2 The East London Line operated as a London Underground (LU) service

between Shoreditch and New Cross/New Cross Gate until it was closed in

2007. The route has been enhanced through a combination of conversion to

National Rail standards, extension and use of existing tracks to create a new

rail route. TfL upgraded the route at a total cost of approximately 1 billion

and provided new electric trains and new and refurbished stations. This was

followed by the second phase which extended the route to Highbury &

Islington in February 2011 and will be followed by a third phase in late 2012.

The first two phases of the project were completed several months ahead of

schedule

1.3 The East London Line runs from Highbury & Islington in the north to New

Cross, West Croydon and Crystal Palace in the south. Five per cent of

Londons population live within a kilometre of an East London Line station and

this figure will increase to over seven per cent with the extension to Clapham

Junction. The route passes through some of the most deprived areas of

London, serves a station at Shoreditch with direct access to the City, and

provides interchanges with LU at Highbury & Islington, Whitechapel and

Canada Water and with DLR at Shadwell.

1.4 The extended route reopened as far as Dalston Junction in May 2010 and was

further extended to Highbury & Islington in February 2011. LUs East London

Line operated 10 trains per hour between New Cross/New Cross Gate and

Shoreditch until 2006 when Shoreditch station was closed. In 2007 the route

operated as far as Whitechapel and carried nine million passengers per year

before its closure. The new route carried around approximately 16 million

passengers in its first year to May 2011, a figure that will increase to 38 million

passengers in the financial year 2011/12.

10

A

p

p

e

n

d

i

x

2

25

2 Improved accessibility

2.1 The East London Line serves parts of northeast London that were previously

poorly served by public transport and links them to key employment centres in

the City, Docklands and West End as well as leisure and social facilities.

Services are fast and frequent and integrated with the TfL network.

2.2 On the central section of the route, passengers have a greater choice of public

transport routes and interchanges to reach their destinations. The route also

provides an important river crossing linking north east and south east London.

2.3 The new route forms part of an orbital network allowing passengers to travel

around London without having to travel through the centre. From stations in

the Boroughs of Bromley, Croydon and Lewisham, passengers can travel

without needing to interchange at London Bridge or Victoria, helping to relieve

crowding on radial rail routes into central London and at congested London

termini.

2.4 Passengers from the north, including those travelling on National Rail services

from Hertfordshire and Essex, can travel to the City and Docklands without

travelling through central London. Use of orbital routes also relieves crowding

on LU services and at stations. The final link in the orbital network, from

Clapham Junction to Surrey Quays will be completed in late 2012 enabling

passengers to travel between east and west London to the south of the city.

11

A

p

p

e

n

d

i

x

2

26

3 Capacity provision

3.1 Rail services on the Sydenham corridor were crowded before the East London

Line opening with over five per cent passengers in excess of capacity in the

morning peak. Southern services on the route now experience lower levels of

crowding. The route provides much needed rail capacity for commuters from

south London to help them access jobs in central London and Docklands and

has increased capacity of services to London by 70 per cent.

3.2 The East London Line is served by new four car Class 378 trains with

longitudinal seating and high capacity layout. Trains have capacity of up to

700 and are designed to carry large numbers of passengers comfortably over

relatively short distances. Walk-through carriages and wide doors ease

passenger flow onto and through the train. The new trains are popular with

passengers as reflected in high customer satisfaction scores for train

attributes.

4 Stations

4.1 TfL managed stations along the route are either refurbished or new. Four new

stations were built as part of the project: Dalston Junction, Haggerston,

Hoxton and Shoreditch High Street which will contribute to regeneration of a

deprived part of east London.

4.2 Stations between West Croydon, Crystal Palace and Surrey Quays transferred

to LO management in September 2009. These stations already served

Southern Trains passengers on services into London Bridge but now offer a

choice of operators and destinations with Overground providing 75 per cent of

services and Southern 25 per cent. The former LU stations on the central

section were refurbished during a two year closure period and four new

stations opened north of the river. Stations meet TfLs standards of customer

services, information and security. Most stations on the route are gated to

ensure revenue is collected in full and to improve passenger security.

5 Service patterns

5.1 LO operates a minimum of four trains per hour on any East London Line route

for most of the day and 12 trains per hour run on the central section from

Surrey Quays to Dalston Junction. On weekdays and Saturdays, first trains

start before 06.00 and last trains are around 23.30.

5.2 The new route has improved accessibility from areas such as Hackney which

were previously relatively poorly served by public transport, providing access

to a high quality, high frequency rail service. Passengers have benefited from

greatly reduced journey times on many journeys since the opening of the

route.

5.3 Shoreditch High Street is within walking distance of the City and Bishopsgate

and the station enables some commuters from north and south London to

reach the City without travelling through Central London.

5.4 The route provides a convenient Thames river crossing. Half of passengers

cross the river on the East London Line, significantly increasing accessibility

12

A

p

p

e

n

d

i

x

2

27

between north and south London and allowing more direct journeys to be

made.

6 Fares

6.1 A range of TfL and National Rail tickets are accepted on the East London

Line. Oyster Pay as You Go is retailed and accepted along the route. PAYG

usage is particularly high on the northern and central sections and accounts

for 40 per cent journeys overall on the East London Line. Travelcards account

for the majority of other journeys.

6.2 Although Shoreditch High Street is in Zone 1, the rest of the line is in Zones 2-

5. This means that many journeys between south London and Docklands or

east London can be made without passing through Zone 1, reducing the cost

of travel. Journeys on Overground, Underground and DLR are charged at TfL

fares which are lower than equivalent rail plus Underground fares.

Table 1 Oyster peak fares from Sydenham

Destination Zone LO LO/LU Rail Rail/LU Season

fare per

journey

London

Bridge

123 2.80 2.10

Shoreditch

High Street

123 2.90 2.90 3.22

Green Park 123 2.90 4.10 3.22

Canary

Wharf

23 1.40 4.10 2.08

Season fare assumes 10 journeys per week

Use of the route

7 Passenger numbers

7.1 23 million passengers have used the extension since its opening. Volumes

are expected to continue to grow as people become aware of new journey

opportunities and as regeneration takes place. For an infrastructure project,

TfL usually assumes 35 per cent of steady state demand is achieved in the

first year and 75 per cent in the second year. Initial growth on the East

London Line was much faster than the standard growth profile with 50 per cent

of forecast demand achieved in the first year of operation. The annual forecast

is 38 million passengers and the project is in line to achieve its forecast benefit

cost ratio.

7.2 Demand has doubled since the first week of operation. 17,000 passengers

per day use the newest section of the route between Dalston Junction and

Highbury & Islington.

13

A

p

p

e

n

d

i

x

2

28

7.3 The busiest station is Canada Water with 30,000 Overground passengers per

day, many of them interchanging with the Jubilee Line. This is followed by

Whitechapel with 15,000, and Highbury & Islington and New Cross Gate with

12,000.

Figure 8: Passenger Loads

Figure 9: Comparison of East London Line demand

14

A

p

p

e

n

d

i

x

2

29

7.4 Figure 9 compares demand by station on the core section of the route which

was served by LU until 2007. Demand at the key interchanges (Canada

Water, Whitechapel and Shadwell) has increased significantly with

passengers from the north and south of the route interchanging at these

stations. This chart shows that, following a closure of over two years, demand

has returned to above pre-closure levels.

8 Time of travel

8.1 Average loads on the route are highest during the weekday peaks with the

largest flows being into Canada Water from the south in the morning for

interchange to the Jubilee Line service to Docklands and the West End and

the reverse flow in the evening. Other key commuting flows are into

Shoreditch High Street and from both directions to Whitechapel. The profile of

demand is similar to that of radial rail routes into London.

8.2 The busiest section of line is between New Cross Gate and Canada Water

where 50,000 people per day travel by LO in both directions. The route has

already become crowded in peak periods with loads over three passengers

per square meeting standing in the peak hour. The extension to Clapham

Junction will provide more capacity on the central section of the route but not

on the crowded section south of New Cross Gate.

Figure 10: Loads by time of day

9 Journey purpose

9.1 The route has a relatively high proportion of regular passengers. 60 per cent

of passengers on the route are using it to travel to or from work, a similar

proportion to that of the rest of LO. The East London Line serves employment

centres both in central London and in Croydon although commuting accounts

for a slightly lower share of demand than for other LO routes.

15

A

p

p

e

n

d

i

x

2

30

9.2 The route also serves a range of leisure destinations including Surrey Quays

shopping centre, Geffrye Museum, Crystal Palace Park and Shoreditch. At

weekends, shopping, leisure and visiting friends and relatives account for a

large proportion of journeys on the line. Both the Geffrye Museum at Hoxton

and the Brunel museum at Rotherhithe have reported increases in visitor

numbers since the extended East London Line opened.

9.3 Average journey length is relatively short at 6kms, reflecting the metro style

nature of the service and the large number of interchanging passengers.

10 Integration

10.1 Integration between modes is key to the design of the East London Line.

More than half of passengers on the route interchange with LU or DLR

services. Canada Water is the largest interchange followed by Whitechapel,

Highbury & Islington and Shadwell. National Rail passengers interchange at

stations such as New Cross and Highbury & Islington and West Croydon

provides an interchange with Tramlink. Research has also shown that

passengers from south London interchange between Southern and

Overground services at intermediate stations along the route. A survey of

passengers using the Highbury & Islington extension and interchanging to

DLR showed that seven per cent had started their journey on other National

Rail services. Some 15 per cent of passengers access LO services by bus.

10.2 Research has shown that simplification of the customer proposition makes

services more convenient to use. Turn up and go services make interchange

easier than with many traditional rail routes and through ticketing for

Overground and LU means that a fully integrated journey can be made for no

extra cost.

Figure 11: Modes used by passengers before the East London Line opening

10.3 Figure 11 shows the modes used by passengers before the East London Line

opened following a survey of public transport users along the route. The

largest switch was from rail use at the southern end of the route, followed by

16

A

p

p

e

n

d

i

x

2

31

significant switches from LU/DLR and bus services. Almost 10 per cent of

people have switched from car use.

10.4 There have been changes in demand on a number of bus routes in the

Dalston and Shoreditch areas that suggest that changes in frequency and/or

structure may be warranted. These are being reviewed by London Buses and

appropriate schemes may be brought forward in due course.

11 Customer satisfaction

11.1 Customer satisfaction with the route averages 85 out of 100, higher than the

results for other Overground routes and with particularly high scores for train

and service level attributes. Figure 12 shows the overall customer satisfaction

scores for the current and old East London Line. Customer satisfaction has

increased from an average of 77 before closure.

Figure 12: Customer satisfaction

12 Operational Performance

12.1 Operational performance on the whole of is a key driver of satisfaction and

has increased since opening to reach 97.5 per cent by the end of 2010/11.

The routes performance has contributed to LO being the best performing train

operator in summer 2011.

13 Equality and inclusion

13.1 The route has increased accessibility of the public transport network in east

London. Step free access is available at 52 per cent of stations served by the

route and the trains have been designed to be accessible. This compares

with 22 per cent of LU stations and 31 per cent of National Rail stations in

London which are step free from street to platform. The new LO trains have

accessibility features such as on board audio and visual train running

information, wider doors for improved accessibility and more grab rails and

handles Staff are trained to assist people using wheelchairs. Research

17

A

p

p

e

n

d

i

x

2

32

shows that eight per cent of users of the route have a long term mental or

physical disability.

13.2 The route serves many of the most deprived boroughs in London, improving

access to jobs and facilities, as shown in the map. Crystal Palace, Norwood

and Croydon have areas of high deprivation as do New Cross and the area

from Whitechapel to Dalston. This is reflected in passengers incomes along

the route with the most affluent passengers living in the area around Wapping

and those with the lowest incomes just north of that area. The extension to

Clapham Junction will also run through areas of high deprivation.

Figure 13: Opportunity areas and most deprived areas

14 House prices

14.1 Data from the Land Registry shows that house prices have increased by more

than the average for east and south east London over the last two years as a

result of the impact of the East London Line on accessibility of the surrounding

areas. A number of newspapers have featured articles on the growth in house

prices. Particular property hotspots are at the northern end of the route where

the line provides completely new journey opportunities, Wapping and the area

around New Cross and New Cross Gate.

18

A

p

p

e

n

d

i

x

2

33

15 Progress against Mayors objectives

Support economic development

and population growth

High frequency services provide access to

employment in central London and

Docklands.

Enhance the quality of life for all

Londoners

High quality trains, customer satisfaction of

85/100 and reduced journey times improve

quality of life.

Improve the safety and security

of all Londoners

New trains with CCTV and refurbished

stations with CCTV and help points

combined with staffing throughout hours of

operation make services safer for

customers.

Improve transport opportunities

for all Londoners

Step free access at half of the stations on

the route and accessible trains improve

access for passengers with disabilities. The

route also serves some severely deprived

areas as shown in Figure 13.

Reduce transports contribution

to climate change and improve

its resilience

Mode switch from car to rail has helped to

reduce CO

2

emissions.

Support the delivery of the

London 2012 Olympic and

Paralympic Games

The link to Highbury & Islington enables

passengers on the route to access services

to the Olympic Park at Stratford and forms

part of the Olympic Transport Plan.

16 East London Line Conclusions

16.1 The East London Line has succeeded in meeting its objectives. Demand has

grown faster than anticipated, despite the downturn in the economy and peak

services are already crowded. Demand will continue to grow and further

capacity will be needed in the next few years. TfLs report Delivering the

Mayors Transport Strategy: National Rail in London sets out TfLs

recommendations for rail capacity in 2014-19. This includes a

recommendation to increase the East London Line trains to five cars in length

as well as lengthening Southern trains on the Sydenham corridor to provide

sufficient capacity to meet demand. Recent trends show that this capacity

increase is essential.

19

A

p

p

e

n

d

i

x

3

34

Appendix 3

LloydsTSB East London House Price Report

A

p

p

e

n

d

i

x

3

35

NOT FOR BROADCAST OR PUBLICATION BEFORE 00.01 HRS TUES 27

th

JULY 2010

East London house prices up 26% since London 2012 victory

announcement

As 27

th

July marks two years until the opening ceremony for the London 2012

Olympic Games, Lloyds TSB research has measured house price performance in the

fourteen postal districts located close to the Olympic Park. .

Some parts of London close to the main site for the London 2012 Olympic and

Paralympic Games have seen a sharp rise in house prices since the capital was

awarded the Games in July 2005. Homerton and Shoreditch both in the borough of

Hackney - have seen average property prices rise by 69% and 53% respectively,

significantly above the Greater London average of 36%.

There has, however, been a mixed performance in property prices with Stratford, the

home of the Olympic Stadium, seeing only a 3% increase in average prices, slower

than any of the other postal districts.

1

Suren Thiru, housing economist, Lloyds TSB, said:

"Some areas close to the Olympic Park have experienced a sharp rise in property

prices since London's successful bid to host the 2012 Olympic and Paralympic

Games. Part of this rise is likely to have been due to an increased interest in property

in these locations from both buyers and investors as a result of the associated

regeneration taking place. The picture, however, is mixed.

Looking forward, property prices across East London are likely to receive a boost

from the legacy of improved infrastructure and transport links left by the London

2012."

KEY FINDINGS:

Average prices in the fourteen postal districts located close to the Olympic

Park have risen by over a quarter (26%) since July 2005. This exceeded the

average rise of 20% across England, but was below the London average of

36%.

Four out of the 14 postal districts near Olympic Park saw house prices rise by

more than the average for London (36%).

House prices in the Olympic Park areas have bounced back strongly from the

downturn in the housing market, rising by 13% between April 2009 and April

2010. This was almost three times the average rise across England (5%), but

slightly lower than the London average (16%).

The average house price among the postal districts near Olympic Park is

262,953.

The least expensive postal district is Plaistow with an average house price of

196,426, followed by East Ham (203,500) and Leyton (209,769).

1

'Postal districts' used to define the following fourteen postal districts that are located close to the site of the 2012

Olympic Park: Bethnal Green, Bow, Clapton, East Ham, Forest Gate, Dalston, Homerton, Leyton, Leytonstone,

Manor Park, Plaistow, Shoreditch, Stratford and Walthamstow.

A

p

p

e

n

d

i

x

3

36

% change in house prices in postal districts near Olympic Park since London

was awarded the 2012 Olympic and Paralympic Games.

Jul-05 Apr-10

Postal District

Average Price

%

Change

Homerton 210,119 355,522 69%

Shoreditch 225,441 345,827 53%

Dalston 218,190 303,243 39%

Clapton 207,805 288,720 39%

Bethnal Green 234,960 317,888 35%

Bow 222,269 292,805 32%

Leytonstone 237,187 297,002 25%

Walthamstow 193,314 224,327 16%

Leyton 186,369 209,769 13%

Forest Gate 203,717 219,241 8%

East Ham 189,368 203,500 7%

Plaistow 187,222 196,426 5%

Manor Park 206,207 214,850 4%

Stratford 206,211 212,217 3%

East London Average 209,170 262,953 26%

Source: Land Registry

Contact for press enquiries:

Emma Partridge, tel 01902 325180 or 07824 471951

Editors' Notes

1. The London house prices quoted in this release are taken from the Land Registry database

and refer to 3 month averages. Prices are arithmetic average prices of houses - otherwise

known as crude averages and are based on Land Registry completions. These prices are

not standardised and therefore can be affected by changes in the sample from year to year

therefore, care should be taken when comparing prices.

2. London house price performance has been measured over the period July 2005 to April 2010

(the latest available Land Registry data).

3. On July 6th 2005 the International Olympic Committee announced London as the winning city

to host the 2012 Olympic and Paralympic Games.

4. East London will see a massive upgrade in facilities from hosting the Olympic and Paralympic

Games. The area will benefit from a 500 acre Olympic Park reaching from the Hackney

Marshes to the Thames, which will include an Olympic stadium, aquatic centre, along with

several other sporting complexes and a 17,800 person Olympic village. Significant transport

improvements are also taking place. Investment is trebling the capacity of Stratford Regional

Station - the main transport hub for London 2012 - and which is expected accommodate

120,000 passengers and enable 200 trains every hour to call there during the Games. A range

of other transport improvements serving the Park are already underway, including an extension

to the Docklands Light Railway (DLR) and increasing capacity on the Jubilee Line.

http://www.london2012.com/index.php

This report is prepared from information that we believe is collated with care, however, it is only

intended to highlight issues and it is not intended to be comprehensive. We reserve the right to

vary our methodology and to edit or discontinue/withdraw this, or any other report. Any use of

this report for an individual's own or third party commercial purposes is done entirely at the risk

of the person making such use and solely the responsibility of the person or persons making

such reliance.

A

p

p

e

n

d

i

x

4

37

Appendix 4:

Dwelling Stock by Council Tax Band (2001-2011)

About the data:

The following pages are sheets that collate the data available from the VOA with a key plan of the

Output Area as well as a brief summary of the station information and its confguration both

before and after TfL takeover.

Council Tax banding data is a useful way to get signifcant data for an area as small as an OA,

the more reliable method of house sale prices is hard to apply to small individual station areas

due to the small number of house sales over the time period.

The methodology of council tax banding is a based on the value of the property in 1991, for new

developments their banding is determined by an estimate of the value of the property in 1991

and it is banded based on this price.

Whilst the data is available for all properties it does have limitations, notably the use of a prices in

1991 for the basis of the data is limiting despite the extrapolation of the equivalent values today.

There are also some anomalies with regard to improvements to properties that may change the

band within which they fall, the banding for these properties is only adjusted following the sale

of the property - if for example a landlord signifcantly changes a property yet doesnt sell it or

divide it, it will remain under the existing band.

Further data on the limitations of Council Tax banding and how it is calculated can be found

online here: http://bit.ly/Ab6N4i

Subsections:

Appendix 4a 38

Information about the data set

Appendix 4b 45

Collated data summary sheets

A

p

p

e

n

d

i

x

4

A

38

General Details

Dataset Title: Dwelling Stock by Council Tax Band, 2006

Domain(s): Housing, Indicators: Housing

Time Period of

Dataset(s):

31 March 2006

Geographic Coverage: England, Wales

Lowest Area Output: Output Area (OA)

Supplier: Department for Communities and Local Government (CLG)

Department: Housing Data and Statistics

National Statistics Data? Not National Statistics - this information based on administrative data

does not comply fully with the National Statistics Code of Practice

No. of Variables

(excluding area names

and codes):

21

Scope and Purpose

NB: Ownership of this dataset remains with the Department for Communities and Local

Government (CLG). Information can only be reproduced if the source is fully acknowledged.

This dataset, drawn from Council Tax valuation lists, has been provided by the Value Office Agency

(VOA) and the Department for Communities and Local Government (CLG) to facilitate assessment

of the overall number of domestic properties and their distribution across specific Council Tax

bands.

The number of dwellings in a given area is the most fundamental statistic in this domain, providing

the context for all other statistical information on the dwelling stock. It is the denominator for

calculating proportions such as tenure, or as in this case Council Tax band, for the purpose of

meaningful comparison between areas that vary in the number of dwellings they contain. The time

series provides basis for monitoring change, in the dwelling stock.

The information provides a breakdown of the number of dwellings in specific Council Tax bands for

individual Output Areas (OAs) across England and Wales at 31 March 2006. Details are given of the

number of properties allocated to each of the standard Council Tax bands. An additional Council

Tax band (Band I) is included with this data year when compared with the previous years available

on the Neighbourhood Statistics (NeSS) website. The additional band only applies to dwellings

located in Wales.

The dataset covers a total number of 23,407,896 dwellings in England and Wales where postcodes

could be matched to a specific OA.

Please note, the figures exclude business premises but include composite dwellings i.e. properties

used for both domestic and business purposes.

Administrative Procedures - Background Information

The source for this data is the Valuation List for Council Tax, which is a register of domestic

properties administered by the VOA and used by Local Authorities (LAs) for local taxation

purposes. These lists have been maintained and updated in their present form since the introduction

of the Council Tax on 1 April 1993.

Although Council Tax came into effect on 1 April 1993 the process of valuing every domestic

property in England and Wales started some time before this. In order to ensure that all dwellings

A

p

p

e

n

d

i

x

4

A

39

are valued on a common basis as they existed on 1 April 1993, the open market value is based on a

fixed valuation date of 1 April 1991. Detailed decisions about value are based on a number of

standard assumptions including:

the sale was with vacant possession;

the interest sold was freehold, except for flats where a lease for 99 years at a nominal rent has

been assumed;

the dwelling had no potential for any building work or other development requiring planning

permission;

the dwelling is in a state of reasonable repair; and

the use of the dwelling would be permanently restricted to private residential purposes.

The original 1993 Valuation Lists were prepared using existing survey data held by the VOA,

supplemented by external inspection of dwellings by surveyors and the matching of property size,

type and age to transactions evidence, indexed to 1991. 50% of bandings were done in-house by the

VOA. The valuations carried out by other private agencies were quality controlled and supervised

by each Listing Officer. Taxpayers had a right of appeal within eight months of 1 April 1993 and

appeals not resolved by agreement were determined by an independent tribunal. An appeals

procedure has remained in place for all subsequent new bandings or rebandings.

While the size, layout or character of a dwelling may be altered by conversion, demolition,

extension or general improvement, the banding cannot be amended until there is a change of

ownership. For example, if a property has been improved since 1 April 1993 there is the possibility

that it will be moved to a higher Council Tax band when it changes hands.

LAs report all changes to the dwelling stock of which they are aware, through new building,

demolition or conversion to the VOA. A new or changed banding is subsequently produced by the

VOA based on the valuation assumptions stated previously. This new banding however will not

become operational until the property changes ownership. A valuation band will not normally be

altered on appeal without a full inspection of the property, but other changes may be made on the

basis of information provided by the Billing Authority and external inspection only.

Concepts and Definitions

Dwelling

Accommodation normally lived in by one or more households and includes houses, flats, bungalows

and maisonettes. Temporary structures such as caravans and houseboats are counted as dwellings if

they are the sole or main residence of a household. The precise definition that applies to this dataset

is set out in Section 3 of The 1992 Local Government Finance Act. It is based on the definition of a

'hereditament' contained in the legislation for rates. This definition differs from the 2001 Census in

the way that it treats shared accommodation. While the Census defines a dwelling as

accommodation that is physically self-contained, the definition used for Council Tax purposes is