Вам также может понравиться

- Caterpillar Game 4 Letter WordsДокумент2 страницыCaterpillar Game 4 Letter Wordsjainmegha01Оценок пока нет

- Number Order Puzzle - My BodyДокумент2 страницыNumber Order Puzzle - My Bodyjainmegha01Оценок пока нет

- Caterpillar Game 4 Letter WordsДокумент2 страницыCaterpillar Game 4 Letter Wordsjainmegha01Оценок пока нет

- 4 Letter Words GameДокумент2 страницы4 Letter Words Gamejainmegha01Оценок пока нет

- 3 Letter Word GameДокумент2 страницы3 Letter Word Gamejainmegha01Оценок пока нет

- 1 Letter Word GameДокумент2 страницы1 Letter Word Gamejainmegha01Оценок пока нет

- 2 Letter Word GameДокумент2 страницы2 Letter Word Gamejainmegha01Оценок пока нет

- Body Part Pattern TemplatesДокумент2 страницыBody Part Pattern TemplatesOana NourОценок пока нет

- Bodydifferent PDFДокумент1 страницаBodydifferent PDFjainmegha01Оценок пока нет

- Number Order Puzzle - My BodyДокумент4 страницыNumber Order Puzzle - My BodyOana NourОценок пока нет

- ©2teachingmommies. All Rights ReservedДокумент4 страницы©2teachingmommies. All Rights ReservedOana NourОценок пока нет

- ©2teachingmommies2010. All Rights ReservedДокумент1 страница©2teachingmommies2010. All Rights ReservedAltuleu TroОценок пока нет

- Bodyprewrite PDFДокумент3 страницыBodyprewrite PDFjainmegha01Оценок пока нет

- LetterB PDFДокумент1 страницаLetterB PDFjainmegha01Оценок пока нет

- Company LawДокумент1 312 страницCompany LawavinashavalaОценок пока нет

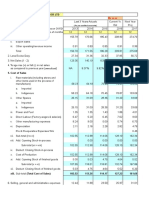

- CMA - Bank Format 15-16Документ77 страницCMA - Bank Format 15-16jainmegha01Оценок пока нет

- Corporate Finance Chapter8Документ4 страницыCorporate Finance Chapter8jainmegha01Оценок пока нет

- BodyPartImages PDFДокумент1 страницаBodyPartImages PDFjainmegha01Оценок пока нет

- All About Dolphins !: A Multilingual Educational ManualДокумент24 страницыAll About Dolphins !: A Multilingual Educational ManualNAAUP AQUAICBASОценок пока нет

- Assessment of Working Capital Requirement: Sheet 1Документ13 страницAssessment of Working Capital Requirement: Sheet 1jainmegha01Оценок пока нет

- MBA List of Colleges ContactsДокумент6 страницMBA List of Colleges Contactsjainmegha01Оценок пока нет

- FM11 CH 22 Tool KitДокумент8 страницFM11 CH 22 Tool Kitjainmegha01Оценок пока нет

- CBSE UGC NET Management Paper 3 December 2014Документ32 страницыCBSE UGC NET Management Paper 3 December 2014jainmegha01Оценок пока нет

- Course Work Syllabus IMSДокумент3 страницыCourse Work Syllabus IMSjainmegha01Оценок пока нет

- Research Paper On EconometricsДокумент17 страницResearch Paper On Econometricsjainmegha01Оценок пока нет

- Researcher ListДокумент22 страницыResearcher Listjainmegha01Оценок пока нет

- IIB Bank Quest April June 12Документ68 страницIIB Bank Quest April June 12Tejaswi KarriОценок пока нет

- Vikalpa-Research PaperДокумент10 страницVikalpa-Research Paperjainmegha01Оценок пока нет

- Management Accounting Chapter 6Документ29 страницManagement Accounting Chapter 6jainmegha01Оценок пока нет

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- New Client QuestionnaireДокумент13 страницNew Client QuestionnairesundharОценок пока нет

- Angeles City National Trade SchoolДокумент7 страницAngeles City National Trade Schooljoyceline sarmientoОценок пока нет

- Detailed Lesson Plan in Mathematics (Pythagorean Theorem)Документ6 страницDetailed Lesson Plan in Mathematics (Pythagorean Theorem)Carlo DascoОценок пока нет

- How Do I Predict Event Timing Saturn Nakshatra PDFДокумент5 страницHow Do I Predict Event Timing Saturn Nakshatra PDFpiyushОценок пока нет

- Feature Glance - How To Differentiate HoVPN and H-VPNДокумент1 страницаFeature Glance - How To Differentiate HoVPN and H-VPNKroco gameОценок пока нет

- A List of 142 Adjectives To Learn For Success in The TOEFLДокумент4 страницыA List of 142 Adjectives To Learn For Success in The TOEFLchintyaОценок пока нет

- Ethics FinalsДокумент22 страницыEthics FinalsEll VОценок пока нет

- Jurnal KORELASI ANTARA STATUS GIZI IBU MENYUSUI DENGAN KECUKUPAN ASIДокумент9 страницJurnal KORELASI ANTARA STATUS GIZI IBU MENYUSUI DENGAN KECUKUPAN ASIMarsaidОценок пока нет

- EIL 6-51-0051-Rev 06 - 1.1kv-Xlpe - Dimension Cat - B Armour-BbpДокумент2 страницыEIL 6-51-0051-Rev 06 - 1.1kv-Xlpe - Dimension Cat - B Armour-BbpShubham BaderiyaОценок пока нет

- Excel Lesson 5 QuizДокумент5 страницExcel Lesson 5 Quizdeep72Оценок пока нет

- Astm C119-16Документ8 страницAstm C119-16Manuel Antonio Santos Vargas100% (2)

- Jurnal Direct and Indirect Pulp CappingДокумент9 страницJurnal Direct and Indirect Pulp Cappingninis anisaОценок пока нет

- Mythology GreekДокумент8 страницMythology GreekJeff RamosОценок пока нет

- JLPT Application Form Method-December 2023Документ3 страницыJLPT Application Form Method-December 2023Sajiri KamatОценок пока нет

- 3-CHAPTER-1 - Edited v1Документ32 страницы3-CHAPTER-1 - Edited v1Michael Jaye RiblezaОценок пока нет

- CMS156Документ64 страницыCMS156Andres RaymondОценок пока нет

- Venere Jeanne Kaufman: July 6 1947 November 5 2011Документ7 страницVenere Jeanne Kaufman: July 6 1947 November 5 2011eastendedgeОценок пока нет

- Know Your TcsДокумент8 страницKnow Your TcsRocky SinghОценок пока нет

- Libel Arraignment Pre Trial TranscriptДокумент13 страницLibel Arraignment Pre Trial TranscriptAnne Laraga LuansingОценок пока нет

- Module 17 Building and Enhancing New Literacies Across The Curriculum BADARANДокумент10 страницModule 17 Building and Enhancing New Literacies Across The Curriculum BADARANLance AustriaОценок пока нет

- Xbox One S Retimer - TI SN65DP159 March 2020 RevisionДокумент67 страницXbox One S Retimer - TI SN65DP159 March 2020 RevisionJun Reymon ReyОценок пока нет

- ARHAM FINTRADE LLP - Company, Directors and Contact Details Zauba CorpДокумент1 страницаARHAM FINTRADE LLP - Company, Directors and Contact Details Zauba CorpArun SonejiОценок пока нет

- English 6, Quarter 1, Week 7, Day 1Документ32 страницыEnglish 6, Quarter 1, Week 7, Day 1Rodel AgcaoiliОценок пока нет

- A Mini-Review On New Developments in Nanocarriers and Polymers For Ophthalmic Drug Delivery StrategiesДокумент21 страницаA Mini-Review On New Developments in Nanocarriers and Polymers For Ophthalmic Drug Delivery StrategiestrongndОценок пока нет

- Risk Management: Questions and AnswersДокумент5 страницRisk Management: Questions and AnswersCentauri Business Group Inc.Оценок пока нет

- Language EducationДокумент33 страницыLanguage EducationLaarni Airalyn CabreraОценок пока нет

- Brochure - Actiwhite PWLS 9860.02012013Документ12 страницBrochure - Actiwhite PWLS 9860.02012013J C Torres FormalabОценок пока нет

- Passive Income System 2Документ2 страницыPassive Income System 2Antonio SyamsuriОценок пока нет

- Paper:Introduction To Economics and Finance: Functions of Economic SystemДокумент10 страницPaper:Introduction To Economics and Finance: Functions of Economic SystemQadirОценок пока нет

- Study of Subsonic Wind Tunnel and Its Calibration: Pratik V. DedhiaДокумент8 страницStudy of Subsonic Wind Tunnel and Its Calibration: Pratik V. DedhiaPratikDedhia99Оценок пока нет